New York FHA Loans

Updated 12/27/2025

FHA loans offer New York homebuyers an opportunity to purchase a house with minimal savings. With these offerings, prospective buyers need not worry about stressing over the often-challenging large down payments typically required for mortgage approval.

How Do I Apply for an FHA Mortgage in New York?

When considering an FHA loan, working with Jet Direct Mortgage to gain pre-approval will allow you to explore the amount of financing available for which you can be approved.

Call Jet Direct Today!

1-800-700-4JET

FHA Loan Application

Ready to Start the FHA Loan Process?

FHA Loans Explained — 2026 Guide for New York Homebuyers

An FHA loan is a government‑backed mortgage insured by the Federal Housing Administration. Because the government absorbs much of the lender’s risk, borrowers can qualify with flexible credit guidelines and a low down payment—making homeownership possible even if you’re still building savings or credit history.

Need exact figures? Contact Jet Direct Mortgage to learn how little you may need to bring to closing and explore local down‑payment assistance programs.

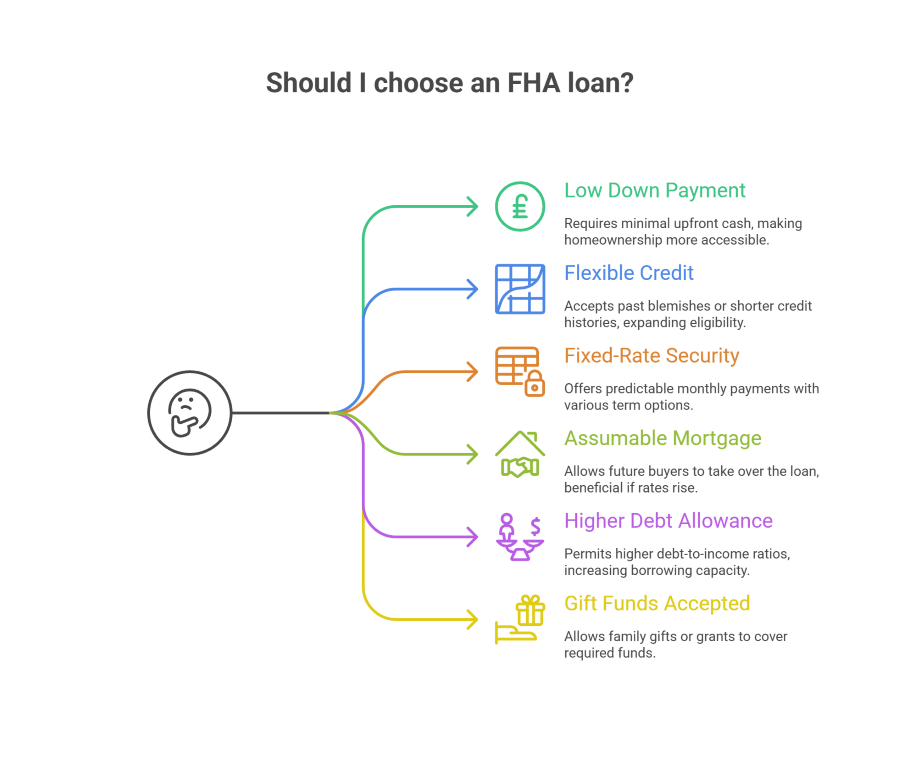

Key Features of FHA Loans in 2026

- Low Down Payment: Minimal cash required upfront—ask Jet Direct for specifics.

- Flexible Credit Requirements: Past blemishes or shorter credit histories are often acceptable.

- Fixed‑Rate Security: Choose 30‑, 25‑, 20‑, or 15‑year terms and lock in predictable monthly payments.

- Assumable Mortgage: A future buyer can take over your FHA loan—an advantage if rates rise.

- Higher Debt Allowance: FHA typically permits higher debt‑to‑income ratios than most conventional programs.

- Gift Funds Accepted: Family gifts, employer assistance, or government grants can cover some or all of your required funds.

Remember: FHA loan limits vary by county. Jet Direct Mortgage can confirm the 2025 limit for your New York borough and property type.

FHA vs. Conventional Financing: Quick Comparison

| Feature | FHA Loan | Conventional Loan |

|---|---|---|

| Down Payment | Low down payment (details from Jet Direct) | Typically higher; varies by lender and program |

| Credit Flexibility | More forgiving | Requires stronger scores for best terms |

| Mortgage Insurance | Up‑front + monthly; can drop later with enough equity | PMI required above 80 % loan‑to‑value; removable |

| Debt‑to‑Income (DTI) | Allows higher DTI in many cases | Stricter limits (varies by lender) |

| Assumable? | Yes | Generally no |

| Best Fit For | First‑time buyers, limited savings, credit challenges | Buyers with solid credit and larger cash reserves |

Disclaimer: Loan rates, terms, and down payment requirements mentioned are for informational and educational purposes only. For personalized guidance and the most current FHA loan options, please contact Jet Direct Mortgage directly.

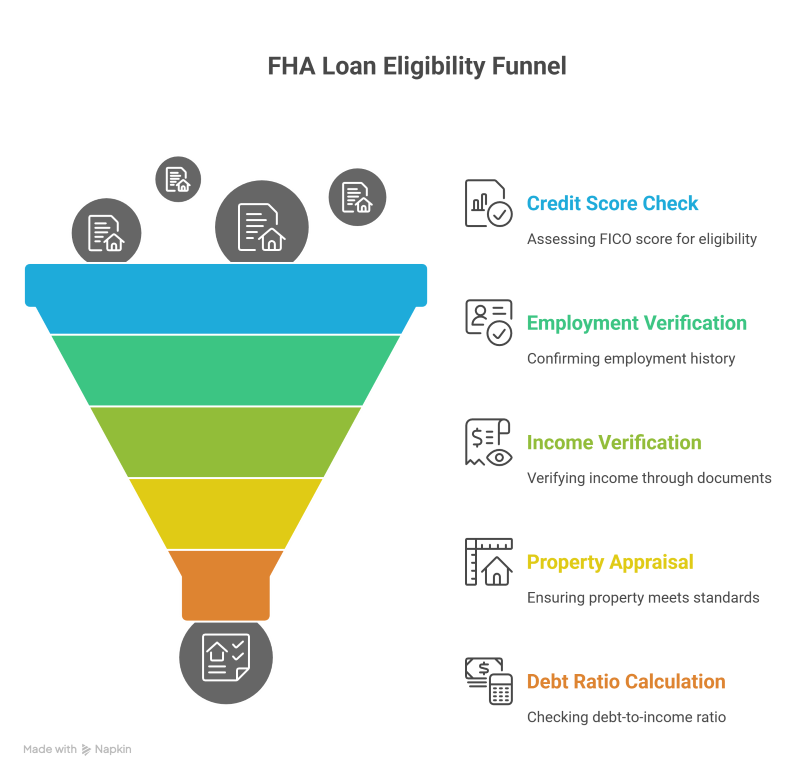

If you are considering an FHA loan, it’s important to understand the eligibility criteria.

- FICO score of 500 to 579 with 10% down, or a FICO score of 580 or higher with 3.5% down

- Verifiable employment history for the last 24 months

- Verifiable income, federal tax returns & bank statements

- Use the loan to finance a primary residence

- Ensure the property is appraised by an FHA-approved appraiser and follow HUD guidelines

- Have a front-end debt ratio of no more than 31% of gross monthly income

FHA mortgages provide immense opportunities for home ownership and financial freedom, though certain criteria must be met prior to applying. You not only need a valid Social Security Number but also you should have attained legal age in the state where you are living. Additionally, your credit score should fall between 500-580 on the 300-850 scale unless there has been bankruptcy within two years of application – then it’s essential that an appropriate reestablished rating is possessed when submitting paperwork.

To qualify for an FHA loan in New York, you’ll need to prove your employment stability: Your current employer must be the same one from at least two years ago. Additionally, all other monthly debt payments should not exceed 50% of total income for approval consideration.

Finally, prerequisites include verifying your residence meets construction standards through a standard appraisal assessment process before approval can be granted.

Unlock the Potential of Home Ownership with an FHA Loan. Before taking this important step, here are some things to be aware of in order to ensure a successful experience!

Securing a loan can be a difficult process, and sometimes additional security is needed to ensure smooth payment processing. FHA loans are protected by Mortgage Insurance Premiums (MIP) that help protect lenders in case of any defaults on repayment schedules. The amount of MIP typically varies based on the size of the loan, its duration as well as downpayment percentage provided at time closing off the mortgage agreement.

Once you have financed the purchase of a home, you are not allowed to apply for a second FHA loan to finance the purchase of a new home. In addition, the buyer should move into the house within 60 days of closing the purchase and should occupy the property for a minimum of one year.

New York FHA Loan Limits by County

| County | 1-Family | 2-Family | 3-Family | 4-Family |

|---|---|---|---|---|

| Albany County | $832,750 | $1,066,250 | $1,288,800 | $1,601,750 |

| Allegany County | $832,750 | $1,066,250 | $1,288,800 | $1,601,750 |

| Bronx County | $1,209,750 | $1,548,975 | $1,872,225 | $2,326,875 |

| Broome County | $832,750 | $1,066,250 | $1,288,800 | $1,601,750 |

| Cattaraugus County | $832,750 | $1,066,250 | $1,288,800 | $1,601,750 |

| Cayuga County | $832,750 | $1,066,250 | $1,288,800 | $1,601,750 |

| Chautauqua County | $832,750 | $1,066,250 | $1,288,800 | $1,601,750 |

| Chemung County | $832,750 | $1,066,250 | $1,288,800 | $1,601,750 |

| Chenango County | $832,750 | $1,066,250 | $1,288,800 | $1,601,750 |

| Clinton County | $832,750 | $1,066,250 | $1,288,800 | $1,601,750 |

| Columbia County | $832,750 | $1,066,250 | $1,288,800 | $1,601,750 |

| Cortland County | $832,750 | $1,066,250 | $1,288,800 | $1,601,750 |

| Delaware County | $832,750 | $1,066,250 | $1,288,800 | $1,601,750 |

| Dutchess County | $832,750 | $1,066,250 | $1,288,800 | $1,601,750 |

| Erie County | $832,750 | $1,066,250 | $1,288,800 | $1,601,750 |

| Essex County | $832,750 | $1,066,250 | $1,288,800 | $1,601,750 |

| Franklin County | $832,750 | $1,066,250 | $1,288,800 | $1,601,750 |

| Fulton County | $832,750 | $1,066,250 | $1,288,800 | $1,601,750 |

| Kings County | $1,209,750 | $1,548,975 | $1,872,225 | $2,326,875 |

| Nassau County | $1,209,750 | $1,548,975 | $1,872,225 | $2,326,875 |

| New York County | $1,209,750 | $1,548,975 | $1,872,225 | $2,326,875 |

| Queens County | $1,209,750 | $1,548,975 | $1,872,225 | $2,326,875 |

| Richmond County | $1,209,750 | $1,548,975 | $1,872,225 | $2,326,875 |

| Suffolk County | $1,209,750 | $1,548,975 | $1,872,225 | $2,326,875 |

| Westchester County | $1,209,750 | $1,548,975 | $1,872,225 | $2,326,875 |

How are FHA mortgage limits determined in New York State?

The Federal Housing Administration (FHA) has announced updated loan limits for 2026, reflecting continued increases in home prices across New York State. These new limits impact both standard (low-cost) counties and high-cost counties, including NYC and surrounding metro areas.

Below is a clear breakdown of the 2026 FHA loan limits applicable in New York, based on the official county-level data.

Standard (Low-Cost Area) FHA Loan Limits – 2026

These limits apply to the majority of New York counties outside designated high-cost areas.

- One-Unit Property: $832,750

- Two-Unit Property: $1,066,250

- Three-Unit Property: $1,288,800

- Four-Unit Property: $1,601,750

These limits represent a significant increase over prior years and expand purchasing power for borrowers in standard-cost markets throughout upstate and central New York.

High-Cost Area FHA Loan Limits – 2026 (NYC, Long Island, Westchester, etc.)

High-cost limits apply to counties such as Bronx, Kings (Brooklyn), Queens, New York (Manhattan), Richmond (Staten Island), Nassau, Suffolk, Rockland, and Westchester.

- One-Unit Property: $1,209,750

- Two-Unit Property: $1,548,975

- Three-Unit Property: $1,872,225

- Four-Unit Property: $2,326,875

These elevated limits are designed to better align FHA financing with real-world property values in New York’s most competitive housing markets.

Why the 2026 FHA Loan Limits Matter

FHA remains a strong option for buyers with lower down payments and flexible credit requirements

Higher borrowing caps increase home affordability

Multi-family limits support house hacking and rental income strategies

Can I Get an FHA Loan in New York?

Yes. New York homebuyers can qualify for an FHA loan in New York by meeting the Federal Housing Administration’s core requirements, including a credit score of 500 or higher (scores ≥ 580 receive broader program benefits). In addition, you’ll need:

- Verifiable income and employment history

- A manageable debt‑to‑income (DTI) ratio

- A primary‑residence property that falls within 2026 county loan limits

Because FHA guidelines are more flexible than conventional standards, many first‑time buyers and moderate‑income families find this the easiest path to homeownership.

How Do I Apply for an FHA Loan in NY?

- Get Pre‑Approved with Jet Direct Mortgage

- A quick pre‑approval reveals how much you can borrow and strengthens your purchase offers.

- Gather Required Documents

- Recent pay stubs, W‑2s or tax returns, bank statements, and photo ID.

- Shop for Homes Within Your Budget

- Jet Direct’s pre‑approval letter shows sellers you’re a serious, qualified buyer.

- Complete the Full Loan Application

- Your Jet Direct loan officer will guide you through appraisal, underwriting, and final approval—keeping the process clear and on schedule.

Ready to take the next step? Contact Jet Direct Mortgage today for an FHA pre‑approval tailored to New York’s 2025 market conditions.

Call Jet Direct Today!

Quick Contact Form

Steps to Secure an FHA Loan in New York

At Jet Direct Mortgage, we strive to provide the highest quality of customer service and make your dream of home ownership a reality. Our experienced team are on hand to guide you through the mortgage process from start to finish – helping you select the best option for your individual needs, so that owning a home is both achievable and enjoyable!

Are you looking for a loan that won’t put too much pressure on your credit score? A low down payment option and lenient income requirements could be just what the doctor ordered. Jet Direct Mortgage gives you an easy way to check out FHA loans online, so explore today!

TIP: If your credit score is not ideal, you may need to focus on rebuilding it before beginning the home shopping process. To make sure you are set up for success, speak to one of our FHA loans specialists today.

Is it hard to get an FHA loan in New York?

An FHA loan may be easier than a conventional mortgage to obtain; however, lenders have tightened their criteria for successful applicants – such as higher credit scores minimums – in light of current economic challenges.

Helpful Mortgage Videos

Top Lender for FHA Loans in New York

FHA Loan Benefits

- Acceptable credit scores are lower for FHA loans.

- FHA loans require a smaller down payment.

- FHA interest rates are typically lower than conventional rates.

- Gift funds can be used towards the down payment or closing costs.

- Sellers are allowed to contribute towards the buyer’s closing costs.

- FHA loans are assumable, meaning they can be transferred to another borrower.

- Co-signers are permitted for FHA loans.

- Higher debt-to-income ratios are allowed for FHA loan applicants.

FHA Loan Pre-Approval Process

- Ensure that you have the minimum required down payment to qualify for the loan.

- Review your credit report and address any issues that may negatively impact your credit score.

- Obtain copies of your tax returns for the last two years.

- Collect your pay stubs from the last month.

- Obtain copies of your bank statements from the last two months.

- Consult with an FHA lender to discuss your loan options and determine the best course of action.

Related FHA Loan articles

- FHA 203(k) Loans: A Complete Guide

- Streamline Your FHA Refinance: The Ultimate Guide

- How FHA Loan Limits Affect You

- FHA vs VA Loans: Which One Should You Choose?

- FHA vs Conventional Loan: Which One is Right for You?

- FHA Loans Credit Requirements | The Complete Guide

- FHA Loan Requirements: A Comprehensive Guide for Home Buyers

- Applying for an FHA Loan: A Step-by-Step Guide

FHA Loans by State

Nearly one out of every two first‑time buyers nationwide — about 46 % — finances with an FHA‑backed mortgage. That share is even higher in expensive metros like New York City and Long Island, where sky‑high home prices can put conventional 20 %‑down loans out of reach.

FHA 203(k) Loans — At a Glance

FHA 203(k) loans let you bundle the purchase (or refinance) of a fixer‑upper with the cost of renovations into one mortgage. Instead of juggling a short‑term construction loan plus a permanent loan, you make a single monthly payment backed by the Federal Housing Administration.

Two Versions to Match Your Project

| 203(k) Option | Best For | Key Features |

|---|---|---|

| Limited 203(k) | Cosmetic or non‑structural updates (e.g., kitchens, flooring, energy‑efficiency upgrades) | • Finance up to $35k in repairs • Mortgage payments can be rolled in while work is completed • More flexible credit requirements (scores as low as ~580) • Streamlined contractor paperwork |

| Standard 203(k) | Major or structural renovations (additions, foundation, accessibility retrofits) | • Covers larger budgets—subject only to FHA county loan limits • Allows structural changes or room additions • Mortgage payments may be included during rehab • Adds long‑term value to an existing or newly purchased home |

How a New York FHA Mortgage Works

New York FHA loans follow national HUD guidelines, but loan caps adjust to local home values. In 2026 a single‑family limit can range from $524,225 in most upstate counties to $1,209,750 in the ten high‑cost counties surrounding NYC and Long Island.

First‑Time Homebuyer Definition

Haven’t owned a primary residence in the past three years? You’re considered a first‑time buyer under FHA rules— even if you’ve owned investment property or a vacation home elsewhere.

New York‑Specific First‑Time Buyer Assistance

The state and many municipalities offer grants or below‑market‑rate second mortgages, such as:

- SONYMA Achieving the Dream (down‑payment assistance)

- NYC HomeFirst DPAP (up to $100k forgivable loan)

- Local HPD and county programs targeting teachers, first responders, or low‑to‑moderate income households

Each program has its own income limits, home‑buyer education requirements, and property price caps—check eligibility early so you can layer assistance with your FHA loan.