Jumbo vs Conventional Loans?

Buying a home on Long Island often comes with higher price tags compared to many parts of the country. With median prices in Nassau and Suffolk Counties consistently above national averages, many buyers face the question: Should I use a Jumbo loan or a Conventional loan?

Both loan programs can help you purchase a home, but they serve different purposes:

- Conventional loans fit within federal loan limits and are often used for standard home purchases.

- Jumbo loans are designed for high-value homes that exceed those loan limits.

This guide explains how each loan type works, outlines key differences, and helps Long Island buyers decide which is right for their purchase—with expert support from Jet Direct Mortgage.

Long Island Housing & Mortgage Landscape

- Median Home Price (2025): Over $600,000 in Nassau and Suffolk counties, with higher averages in coastal and luxury markets like the Hamptons or North Shore.

- Buyer Profiles: First-time buyers often lean toward Conventional financing, while professionals, executives, and luxury buyers frequently require Jumbo loans.

- Loan Usage: Conventional loans dominate typical purchases under conforming limits, while Jumbo loans are essential for many Long Island neighborhoods where prices exceed those limits.

Understanding which loan fits depends largely on home price, your credit profile, and financial goals.

What Is a Conventional Loan?

Conventional loans are mortgages not backed by a government agency. They are originated by private lenders and often sold to Fannie Mae or Freddie Mac. Because they must fall within set conforming loan limits, they’re the most common choice for standard home purchases across Long Island.

In 2025, the conforming loan limit for single-family homes in high-cost areas like Long Island is $1,149,825. Any loan amount above this becomes a Jumbo loan.

Conventional financing is well-suited for:

- Buyers with strong credit and stable incomes.

- Families purchasing homes within conforming limits.

- Investors financing second homes or smaller properties.

Key Features

- Credit score requirement typically 620 or higher.

- Private Mortgage Insurance (PMI) required if equity is below 20%, but removable once sufficient equity is reached.

- Contact Jet Direct Mortgage for specific down payment requirements.

Eligibility Criteria

- Must demonstrate stable employment and verifiable income.

- Credit history showing consistent repayment.

- Loan amount within conforming loan limits.

Benefits of Conventional Loans

- Competitive interest rates for qualified borrowers.

- PMI can be removed, lowering long-term costs.

- Flexibility to finance second homes or investment properties.

What Is a Jumbo Loan?

A Jumbo loan is a mortgage for amounts above conforming loan limits set by the Federal Housing Finance Agency (FHFA). Because they’re larger loans, they are not eligible to be sold to Fannie Mae or Freddie Mac. This makes them riskier for lenders, which means stricter qualification standards for borrowers.

On Long Island, where homes in areas like the Hamptons, North Shore, or luxury Nassau County neighborhoods often exceed $1 million, Jumbo loans are critical. They enable buyers to finance high-value homes that Conventional loans cannot cover.

Key Features

- Loan amounts above $1,149,825 in 2025 for single-family homes in Long Island.

- Stricter underwriting: higher credit score, lower debt-to-income ratios, and larger reserves often required.

- Contact Jet Direct Mortgage for specific down payment requirements on Jumbo loans.

Eligibility Criteria

- Strong credit history (often 700+).

- Verifiable, stable income at higher levels.

- Significant cash reserves or assets.

Benefits of Jumbo Loans

- Allows financing of high-value properties beyond Conventional limits.

- Competitive rates for well-qualified borrowers.

- Flexibility in structuring loan amounts to fit luxury or coastal properties.

Jumbo vs Conventional: Side-by-Side Comparison

| Feature | Conventional Loan | Jumbo Loan |

| Loan Limit (2025) | Up to $1,149,825 | Above $1,149,825 |

| Credit Score Requirement | 620+ | Typically 700+ |

| Property Types | Primary, secondary, investment | Primarily primary & luxury secondary |

| Best For | Buyers within conforming limits | Buyers purchasing luxury or high-value homes |

Factors Long Island Buyers Should Consider

- Home Price

- If your purchase is under $1,149,825, a Conventional loan likely fits.

- Above that threshold, you’ll need a Jumbo loan.

- Credit & Financial Profile

- Conventional: available with fair-to-excellent credit (620+).

- Jumbo: best for strong credit (700+), lower debt-to-income ratios.

- Property Goals

- Conventional loans: primary homes, second homes, or investment properties.

- Jumbo loans: typically focused on luxury or primary residences.

- Future Plans

- If you may want to refinance or pay down quickly, Conventional loans provide more flexible exit strategies.

- Jumbo loans suit those ready for long-term investment in high-value real estate.

Real-World Scenarios for Long Island Buyers

- Family in Nassau County: Purchasing a $750,000 colonial in Garden City → Conventional loan.

- Professional in Huntington: Upgrading to a $1.2 million waterfront property → Jumbo loan.

- Investor in Smithtown: Buying a $600,000 rental duplex → Conventional loan (investment allowed).

Steps to Apply

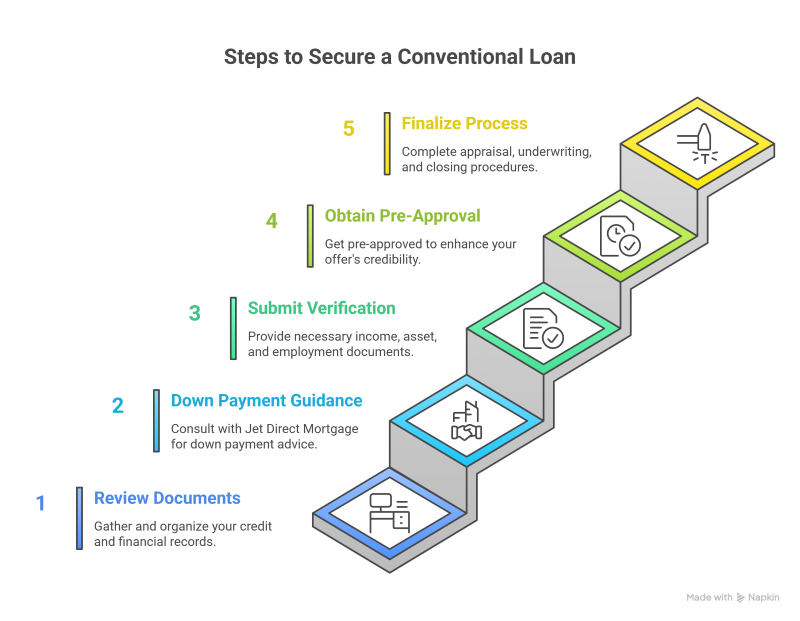

Conventional Loan

- Review your credit and financial documents.

- Contact Jet Direct Mortgage for down payment guidance.

- Submit income, asset, and employment verification.

- Obtain pre-approval to strengthen your offer.

- Finalize appraisal, underwriting, and closing.

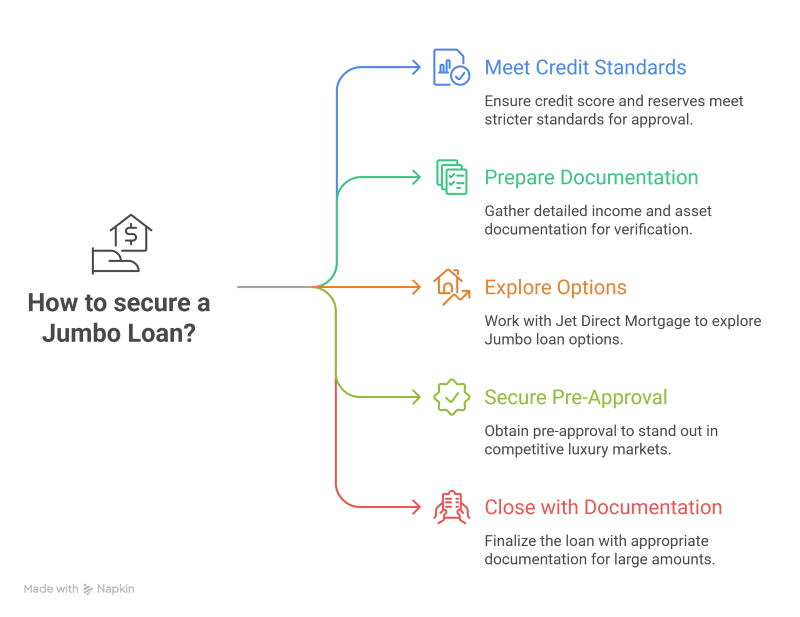

Jumbo Loan

- Ensure credit score and reserves meet stricter standards.

- Prepare detailed income and asset documentation.

- Work with Jet Direct Mortgage to explore Jumbo options.

- Secure pre-approval, especially in competitive luxury markets.

- Close with appropriate documentation for large loan amounts.

How Jet Direct Mortgage Helps Long Island Buyers

Jet Direct Mortgage provides:

- Local expertise in Nassau and Suffolk housing markets.

- Loan program guidance for Conventional and Jumbo financing.

- Fast, competitive processing tailored to Long Island’s competitive market.

- One-on-one support to align financing with your financial goals.

Frequently Asked Questions (FAQs)

What is the current conforming loan limit on Long Island?

For 2025, the conforming loan limit for single-family homes in Nassau and Suffolk is $1,149,825.

If your home loan is at or below this limit, it can qualify as Conventional.

If your loan amount is above this limit, you’ll need a Jumbo loan.

This threshold is especially relevant in markets like the Hamptons, North Shore, and parts of Nassau County, where prices frequently exceed $1 million.

Which loan type usually offers lower interest rates?

Conventional loans: For qualified borrowers, rates are highly competitive and often slightly lower than Jumbo.

Jumbo loans: Rates can be just as competitive for strong borrowers, but historically, Jumbo loans carried higher rates due to lender risk.

Important Note: Rate differences can change with market conditions. On Long Island, qualified Jumbo borrowers often secure similar or only slightly higher rates than Conventional borrowers.

Can I use a Conventional loan for an investment property?

Yes. This is one of the biggest advantages of Conventional financing.

You can use it for:

Primary residences

Second homes (like a weekend retreat in Montauk)

Investment properties (rental units, condos, or multifamily homes)

Jumbo loans, by contrast, usually focus on primary residences and luxury second homes but not investment properties.

What credit score do I need for a Jumbo loan?

Most lenders require 700 or higher for a Jumbo loan. Some may set the bar at 720 or even 740 depending on loan size.

By comparison:

Conventional loans: Minimum 620.

Jumbo loans: Typically 700+.

Best practice: The stronger your score, the more competitive your interest rate and terms.

Are closing costs higher for Jumbo loans?

Yes. Jumbo loans often involve:

Higher origination fees.

More detailed appraisals (sometimes two appraisals required).

Larger required reserves (cash savings set aside after closing).

Conventional loans usually have more predictable and lower closing costs.

Can I refinance a Jumbo loan into a Conventional loan later?

Yes. Many Long Island buyers refinance when:

They’ve paid down their loan balance below the conforming limit.

They want to access lower interest rates or eliminate stricter Jumbo requirements.

Example: A homeowner with a $1.25M Jumbo mortgage could refinance into a Conventional loan once their balance drops below $1,149,825, unlocking different options.

How do I know if a Jumbo or Conventional loan is right for me?

Ask yourself these questions:

What’s the price of the home I want to buy?

Below $1,149,825 → Conventional likely.

Above $1,149,825 → Jumbo required.

What’s my credit profile?

620–680 → Conventional may be more realistic.

700+ with strong reserves → Jumbo is an option.

What are my goals?

Buying an investment property → Conventional only.

Purchasing a luxury primary or vacation home → Jumbo may be required.

The best way to decide is by contacting Jet Direct Mortgage for a side-by-side analysis of costs, eligibility, and long-term benefits.

When to Choose Jumbo vs Conventional Loans

| Situation | Best Loan Type | Why It Fits |

| Home price below $1,149,825 (2025 limit for Long Island) | Conventional | Stays within conforming loan limits; easier to qualify with fair-to-good credit. |

| Home price above $1,149,825 | Jumbo | Required for high-value homes in areas like the Hamptons, North Shore, or luxury Nassau County. |

| Credit score between 620–680 | Conventional | More forgiving credit requirements compared to Jumbo loans. |

| Credit score 700+ with strong reserves | Jumbo | Meets stricter underwriting standards; competitive rates for luxury buyers. |

| Buying an investment property or rental | Conventional | Eligible for investment financing, which Jumbo loans generally don’t allow. |

| Buying a primary luxury residence | Jumbo | Allows financing of high-value or luxury properties beyond conforming limits. |

| Wanting to remove PMI once equity reaches 20% | Conventional | PMI can be canceled, reducing long-term monthly costs. |

| Planning to stay long-term in a high-value home | Jumbo | Provides financing flexibility for larger mortgages with competitive terms. |

Conclusion

For Long Island buyers, the choice between Jumbo and Conventional loans depends on your home price, financial profile, and long-term goals. Conventional loans are ideal for homes within conforming limits, while Jumbo loans are essential for luxury or high-value purchases.

Contact Jet Direct Mortgage today:

- 🌐 Visit JetDirectMortgage.com

- 📞 Call: +1.800.700.4JET

- 📧 Email: express@jetdirectmortgage.com

- 📍 4875 Sunrise Hwy, Suite 300, Bohemia, New York 11716

Additional Resources

Experienced Chief Operating Officer with a 26 + year demonstrated history of working in the banking industry. Skilled in all aspects of the residential mortgage market . Strong business development professional with a Bachelor of Science (BS) focused in Business Administration and Management, from St. Joseph College. A direct endorsement underwriter and a licensed Mortgage Loan Originator.