Reverse vs. Refinance: Which Fits Seniors Best?

For many New York homeowners entering retirement, their home is more than just a place to live — it’s one of their most valuable financial assets. As expenses shift, fixed incomes become the norm, and financial priorities change, many seniors look to unlock or restructure their home equity for greater stability. Two of the most common strategies are:

- Reverse mortgage, which allows eligible homeowners to access their equity without making monthly payments.

- Conventional refinance, which replaces an existing mortgage with a new one—often with better terms.

Both options can provide meaningful financial relief, but they serve very different purposes. The right choice depends on your personal goals, income structure, and long-term plans for your property.

Understanding Your Options as a Senior Homeowner

Why Many Seniors in New York Consider Reverse Mortgages or Refinancing

The cost of living in New York is among the highest in the country, and housing expenses are often a major factor for retirees. For many seniors:

- Monthly mortgage payments may take up a large portion of fixed income.

- Rising property taxes and insurance costs can create financial strain.

- They may want to age in place rather than sell and downsize.

- Equity built over decades can be converted into financial flexibility.

That’s why reverse mortgages and conventional refinancing have become attractive solutions for seniors seeking stability and control over their retirement finances.

How Rising Home Values Impact Senior Lending Options

According to the Federal Housing Finance Agency, New York home values have grown steadily over the past decade. For seniors, that means:

- Higher available equity.

- Potential to qualify for larger reverse mortgage payouts.

- More refinancing options with competitive rates.

In high-value markets like Long Island, Westchester County, and New York City, the home itself often becomes a cornerstone of retirement planning.

What Is a Reverse Mortgage?

A reverse mortgage allows homeowners aged 62 and older to convert part of their home equity into cash or a line of credit without selling the home or making monthly mortgage payments. Instead of paying the lender each month, the lender pays the homeowner.

The loan balance grows over time and is typically repaid when:

- The homeowner sells the property,

- Moves out permanently, or

- Passes away.

How Reverse Mortgages Work

- The borrower must continue to pay property taxes, insurance, and maintain the home.

- Borrowers can receive funds as a lump sum, monthly payments, or a line of credit.

- Interest accrues on the outstanding balance, reducing the home’s available equity over time.

Eligibility Requirements for Reverse Mortgages in New York

- Borrower must be at least 62 years old.

- The property must be the primary residence.

- The home must meet HUD property standards.

- The homeowner must have sufficient equity in the property.

- Must complete HUD-approved reverse mortgage counseling.

Pros of Reverse Mortgages for Seniors

- 💰 No monthly mortgage payments required.

- 🏡 Remain in the home while accessing equity.

- 🔐 Can improve cash flow during retirement.

- 📊 Flexible payout options (lump sum, monthly, or line of credit).

- 🪙 Non-recourse loan: borrowers or heirs never owe more than the home’s value.

Cons of Reverse Mortgages for Seniors

- 📉 Equity decreases over time as interest accrues.

- 🧾 Property taxes, insurance, and maintenance remain required.

- 💵 Fees and closing costs can be higher than a traditional loan.

- 🧓 Can affect estate planning and inheritance.

- 🏦 Must be repaid when the borrower leaves the home.

What Is a Conventional Refinance?

A conventional refinance involves taking out a new mortgage to replace an existing one, often with better terms. Unlike a reverse mortgage, you’ll continue to make monthly payments, but you may benefit from a lower interest rate or a shorter loan term.

How Refinancing Works for Seniors

- Homeowners apply for a new mortgage, which pays off the original loan.

- The new loan may have a lower interest rate, lower monthly payment, or different term length.

- Some seniors use cash-out refinancing to access part of their home equity for expenses like medical bills, renovations, or supplemental income.

Eligibility Requirements for Conventional Refinance in New York

- Adequate credit score (usually 620 or higher).

- Stable income or retirement benefits.

- Sufficient home equity (often 20%+ to avoid PMI).

- Property must meet lender appraisal standards.

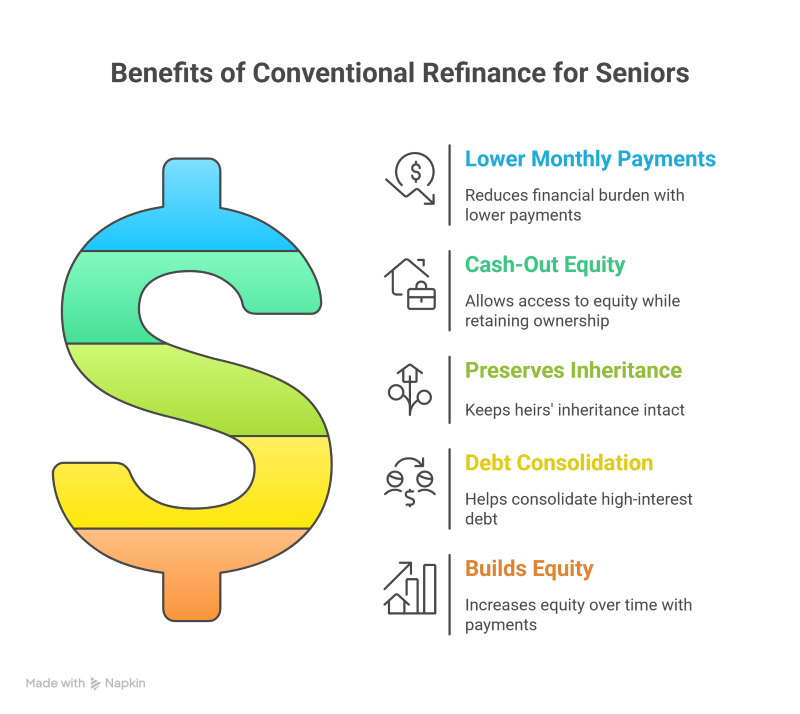

Pros of Conventional Refinance for Seniors

- 📉 Potential for lower monthly payments or interest rates.

- 💵 Option to cash out some equity while retaining ownership.

- 🏡 Keeps heirs’ inheritance intact.

- 💳 May help consolidate high-interest debt.

- 📈 Builds equity over time with continued payments.

Cons of Conventional Refinance for Seniors

- 💰 Monthly payments continue, which may strain fixed income.

- 📝 Requires credit and income verification.

- 💵 Closing costs can be significant.

- 🏦 Risk of foreclosure if payments cannot be maintained.

Reverse Mortgage vs. Conventional Refinance: Key Differences

| Feature | Reverse Mortgage | Conventional Refinance |

| Monthly Payments | No monthly payments required | Monthly mortgage payments required |

| Eligibility Age | 62+ | No age requirement |

| Equity Impact | Reduces equity over time | Builds equity through payments |

| Ownership | Borrower retains ownership | Borrower retains ownership |

| Repayment | When borrower moves, sells, or passes | Monthly over loan term |

| Credit Requirements | Limited (financial assessment) | Strong credit typically required |

| Effect on Heirs | May reduce inheritance | Home remains part of estate |

| Funds Access | Lump sum, line of credit, or monthly payments | Lump sum at closing if cash-out |

Key Takeaway

- Reverse mortgage: Often better for those who want to improve cash flow and remain in their home without monthly payments.

- Refinance: Often better for those who want to lower their interest rate or preserve equity for heirs.

Financial Considerations for Seniors in New York

Property Taxes, Insurance, and Home Maintenance

Even if monthly mortgage payments are eliminated through a reverse mortgage, homeowners are still responsible for:

- 🧾 Property taxes

- 🏡 Homeowners insurance

- 🧰 Regular home maintenance

Failing to meet these obligations can lead to foreclosure under both reverse and conventional loans.

Impact on Retirement Income

- Reverse mortgages can supplement fixed incomes, helping pay for everyday living expenses, medical costs, or home modifications.

- Refinancing can lower monthly mortgage payments and reduce interest costs, freeing up more income each month.

Estate Planning & Inheritance

- Reverse mortgages may reduce or eliminate equity passed down.

- Refinancing allows the home to remain a tangible asset for family inheritance.

When Each Option Might Make Sense

When a Reverse Mortgage May Be Better for Seniors

- You need more monthly income to maintain your lifestyle.

- You plan to stay in your home long-term.

- You don’t mind your equity decreasing over time.

- You have no dependents relying on inheriting the property.

When a Conventional Refinance May Be Better

- You want to lower your mortgage rate or monthly payments.

- You want to preserve equity for family or future financial needs.

- You have strong credit and stable income.

- You’re comfortable with continuing monthly payments.

How Loan Choice Affects Monthly Cash Flow

- Reverse mortgage: Eliminates monthly mortgage payments, increasing available income for living expenses.

- Conventional refinance: May lower monthly payments but maintains an obligation to pay each month.

Property Taxes and Insurance Still Apply

- Regardless of which option you choose, you must continue paying property taxes, homeowners insurance, and maintenance costs.

- Failing to pay these expenses can result in default under either loan.

Estimated Cost Impact for NY Homeowners

| Factor | Reverse Mortgage | Conventional Refinance |

| Monthly Mortgage Payment | $0 (taxes/insurance still required) | Varies by loan size and interest rate |

| Upfront Costs | Higher (MIP, origination, closing) | Moderate (standard closing costs) |

| Access to Equity | Lump sum, line of credit, or monthly payout | Cash-out option if desired |

| Long-Term Equity | Decreases over time | Preserved or increased with payments |

| Impact on Heirs | Reduces inheritance | Property remains in estate |

| Risk of Foreclosure | For failure to pay taxes/insurance | For missed monthly payments |

| Ideal For | Seniors who want cash flow flexibility | Seniors who want lower payments but keep equity |

Key Insight: Reverse mortgages offer flexibility but can erode equity over time. Refinancing may provide lower monthly payments while preserving more wealth for future use or heirs.

How to Choose the Best Option in New York

Step-by-Step Decision Framework

- 🧾 Evaluate your financial goals — income flexibility vs equity preservation.

- 🏡 Consider your long-term living plans — aging in place or selling eventually.

- 📊 Assess your credit score, income, and existing mortgage terms.

- 🪙 Compare loan costs, benefits, and impacts on inheritance.

- 🧠 Consult trusted mortgage professionals who understand senior lending in New York.

Pro Tip: Reverse mortgages may sound appealing due to the absence of monthly payments, but they can reduce your estate significantly. Refinancing can protect equity but requires ongoing financial commitment.

Application & Qualification Considerations

Reverse Mortgage Eligibility Checklist

- Age 62 or older.

- Home is primary residence.

- Sufficient equity in the home.

- HUD counseling completion.

- Up-to-date on property taxes and insurance.

Conventional Refinance Eligibility Checklist

- Adequate credit score (620+ is typical).

- Stable income or retirement benefits.

- Sufficient home equity (often 20%+ to avoid PMI).

- Property meets lender’s appraisal and condition standards.

- Willingness and ability to continue monthly payments.

Step-by-Step: Applying for a Loan

Reverse Mortgage Application Steps

- Complete HUD-approved counseling session.

- Gather financial and property documentation.

- Apply with a reverse mortgage lender.

- Property appraisal and financial assessment.

- Loan closing and disbursement of funds.

Conventional Refinance Application Steps

- Review current mortgage and credit profile.

- Shop for competitive refinance rates.

- Submit income, asset, and property documents.

- Appraisal and underwriting review.

- Close on the new mortgage.

Special Considerations for Seniors in New York

- Co-ops and Condos: Reverse mortgages may have restrictions; conventional refinancing is often easier, though co-op board approval may be required.

- High Property Values: Some homes may require jumbo refinance loans or proprietary reverse mortgages.

- Legal and Financial Protections: New York includes consumer protections for reverse mortgages (counseling and disclosures). Heirs have options to settle or sell the property.

(FAQs)

- What is the minimum age for a reverse mortgage in New York?

62 years old (younger spouses may have limited protections). - Will I still own my home with a reverse mortgage?

Yes, ownership remains as long as taxes, insurance, and maintenance are kept current. - Can I refinance after taking a reverse mortgage?

Yes, if you qualify and have adequate equity. - Which option is more cost-effective in the long run?

For equity preservation and inheritance, refinancing is often better. For cash-flow relief, a reverse mortgage can be practical. - Can a reverse mortgage affect my heirs?

Yes. It reduces equity; heirs can repay the balance or sell the property. - What credit score is required for refinancing?

Many lenders look for 620+, with better terms at higher scores. - Can I use a reverse mortgage on a condo or co-op in NYC?

Condos may be eligible if approved; co-ops are usually not eligible for federally insured reverse mortgages. Refinancing is typically more straightforward for both. - Does a reverse mortgage have to be repaid?

Yes — when you sell, move out permanently, or pass away.

Final Thoughts:

For many New York seniors, deciding between a reverse mortgage and a conventional refinance comes down to one critical question:

👉 Do you want to prioritize monthly cash flow or equity preservation?

- Reverse mortgages can offer immediate financial relief by eliminating monthly payments, supporting those who want to age in place.

- Refinancing may be the smarter move for those with steady income who want to keep the property in the family and manage long-term costs.

The right choice depends on your age, financial situation, property type, and long-term goals.

🏡 Contact Jet Direct Mortgage for Expert Guidance

Choosing between a reverse mortgage and a refinance can feel overwhelming — but you don’t have to decide alone. Jet Direct Mortgage can help you evaluate your options and find the best loan structure for your retirement goals.

Contact Information:

- 🌐 jetdirectmortgage.com

- 📞 +1.800.700.4JET

- 📧 express@jetdirectmortgage.com

- 🏢 4875 Sunrise Hwy, Suite 300, Bohemia, New York 11716

Disclosure

All figures in this article are for informational purposes only. For a real mortgage application, contact Jet Direct Mortgage using the information above.

Experienced Chief Operating Officer with a 26 + year demonstrated history of working in the banking industry. Skilled in all aspects of the residential mortgage market . Strong business development professional with a Bachelor of Science (BS) focused in Business Administration and Management, from St. Joseph College. A direct endorsement underwriter and a licensed Mortgage Loan Originator.