A Complete Homeowner Guide for Nassau & Suffolk County

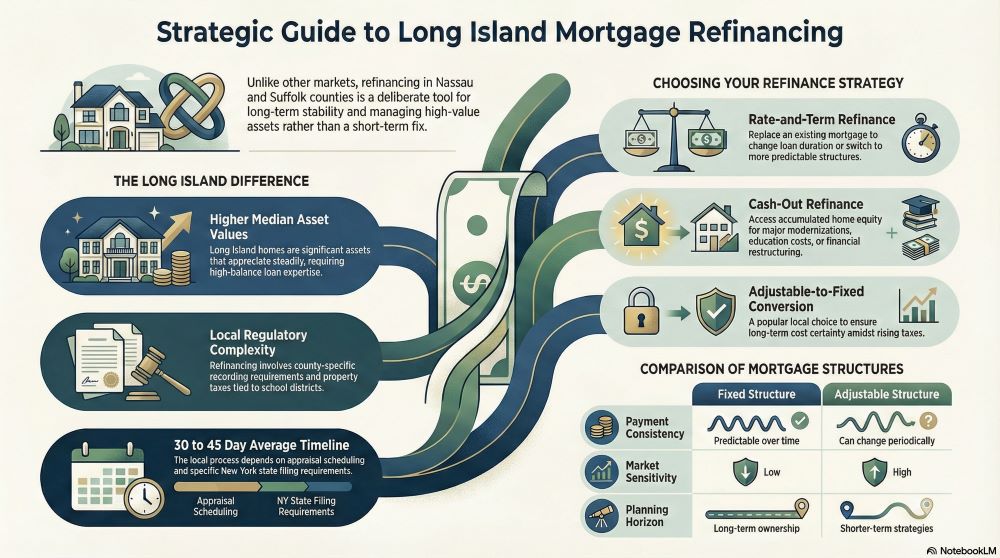

Mortgage refinancing on Long Island is a strategic financial decision shaped by local property values, tax structures, and long-term ownership patterns that are distinct from many other housing markets. Homeowners across Nassau and Suffolk County often approach refinancing not as a short-term adjustment, but as a deliberate step toward stability, flexibility, and long-range financial planning.

Long Island homes frequently represent a household’s most significant asset. Refinancing that asset can influence monthly budgeting, future liquidity, and overall financial resilience for years to come. Because many residents remain in their homes longer than the national average, the impact of a refinance decision tends to extend well beyond immediate outcomes. That reality makes it essential to understand how refinancing works within a local context, how different refinance structures support different goals, and what practical considerations apply specifically to Long Island properties.

What Mortgage Refinancing Means for Long Island Homeowners

Mortgage refinancing replaces an existing home loan with a new mortgage that may have different terms, structure, or repayment timeline. On Long Island, refinancing is often used as a financial planning tool rather than a reaction to short-term changes.

Homeowners may refinance to better align their mortgage with evolving priorities, such as career progression, family needs, education planning, or preparing for retirement. Because Long Island properties tend to retain value and appreciate steadily over time, refinancing decisions are frequently evaluated in the context of long-term homeownership rather than quick turnover.

Refinancing may help homeowners:

- Restructure their mortgage to better match household income patterns

- Improve long-term predictability and budgeting clarity

- Access flexibility for major life events

- Simplify financial obligations into a single housing payment

Why Refinancing on Long Island Is Structurally Different

Long Island refinancing differs from refinancing in many other parts of the country due to a combination of market, regulatory, and geographic factors. These elements influence how loans are structured, how properties are evaluated, and how refinancing timelines unfold.

Key factors include:

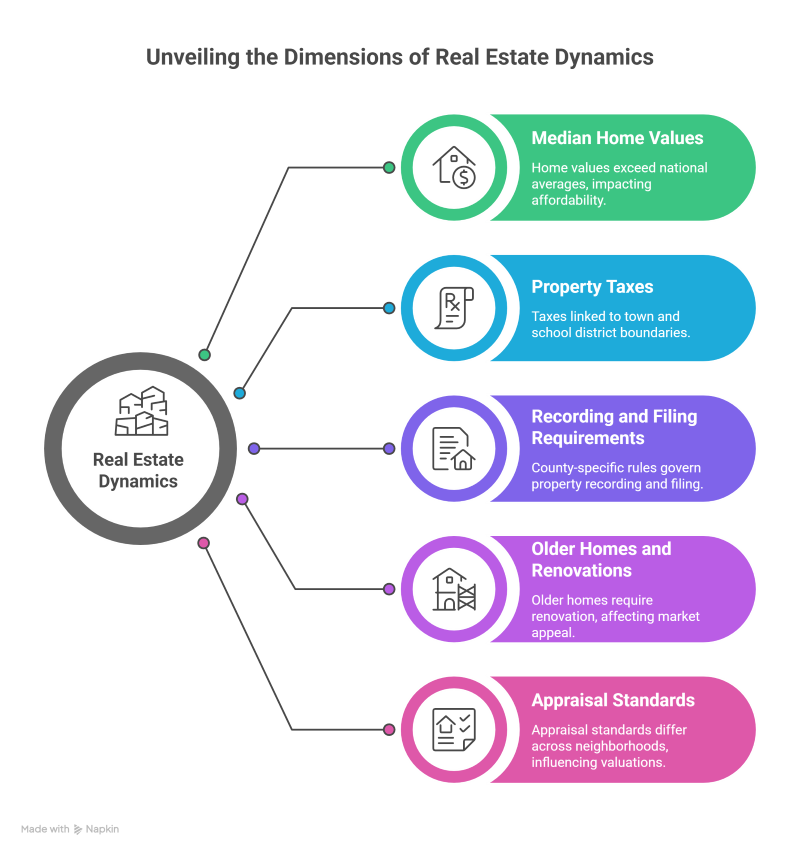

- Higher median home values than national averages

- Property taxes tied closely to town and school district boundaries

- County-specific recording and filing requirements

- A large inventory of older homes with renovation considerations

- Appraisal standards that vary by neighborhood

Because of these differences, refinancing strategies that work elsewhere may not translate directly to Long Island. Local knowledge often plays a significant role in determining whether a refinance proceeds smoothly or encounters delays.

Common Reasons Homeowners Refinance in Nassau and Suffolk County

Homeowners refinance for a variety of reasons, but on Long Island, motivations are often tied to long-term planning rather than short-term financial shifts.

Common refinance motivations include:

- Stabilizing housing costs for extended homeownership

- Adjusting mortgage structure after career or income changes

- Preparing for retirement or fixed-income years

- Consolidating financial obligations into one payment

- Funding significant home improvements or accessibility upgrades

Each of these goals requires a different approach to refinancing, which is why careful evaluation is essential before selecting a refinance structure.

Types of Long Island Mortgage Refinance Options

Refinancing is not a single product. It includes several loan strategies designed to meet different homeowner objectives.

Rate-and-Term Refinance

A rate-and-term refinance replaces an existing mortgage with a new loan that changes the repayment structure, loan duration, or loan type without accessing additional funds.

This approach is commonly used to:

- Adjust the length of the mortgage

- Switch between loan structures

- Improve long-term predictability

Cash-Out Refinance

A cash-out refinance allows homeowners to access a portion of their available home equity while refinancing their existing mortgage.

On Long Island, this option is often explored for:

- Renovations or home modernization projects

- Education-related expenses

- Planned major expenditures

- Financial restructuring or consolidation

Because Long Island homes often accumulate equity over time, cash-out refinancing is frequently considered, though it should be approached with a clear long-term plan.

Adjustable-to-Fixed Refinance

Homeowners with adjustable loan structures may refinance into fixed structures to reduce variability and gain greater long-term certainty.

Fixed vs. Adjustable Refinance Structures on Long Island

| Feature | Fixed Structure | Adjustable Structure | Considerations |

| Payment Consistency | Predictable over time | Can change periodically | Long-term vs. short-term planning |

| Market Sensitivity | Low | Higher | Risk tolerance |

| Planning Horizon | Long-term ownership | Shorter-term strategies | Exit planning |

| Common Use | Stability-focused homeowners | Flexible timelines | Market awareness |

On Long Island, fixed structures are often favored by homeowners who plan to remain in their homes for many years and want consistent housing obligations alongside rising taxes and insurance costs.

How Home Equity Shapes Refinancing Decisions on Long Island

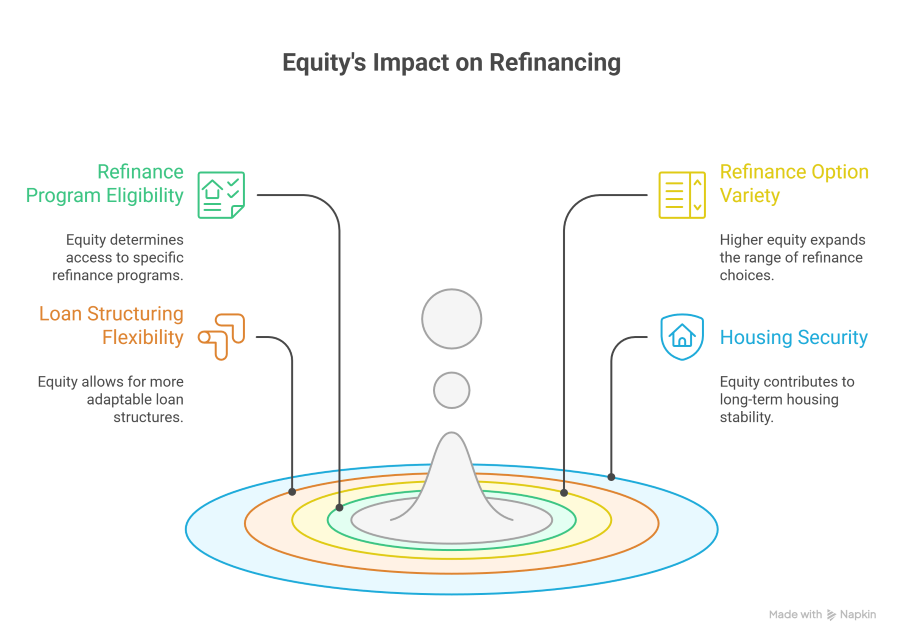

Home equity is the difference between a home’s market value and the remaining mortgage balance. Long Island homeowners often build substantial equity due to long ownership periods and consistent demand across many neighborhoods.

Equity influences:

- Eligibility for certain refinance programs

- The range of refinance options available

- Overall flexibility in loan structuring

- Long-term housing security

While equity can provide financial flexibility, accessing it without a clear strategy may limit future options. Responsible refinancing balances current needs with long-term stability.

Refinance Goals and Matching Loan Strategies

| Homeowner Goal | Refinance Strategy | Typical Outcome | Long Island Consideration |

| Long-term stability | Fixed refinance structure | Predictable housing costs | High property taxes favor consistency |

| Accessing equity | Cash-out refinance | Funds for major expenses | Strong appreciation supports equity |

| Short-term flexibility | Adjustable refinance | Lower initial obligation | Requires clear future plan |

| Debt restructuring | Cash-out or rate-term | Simplified finances | Closing costs must be evaluated |

This table helps homeowners connect refinancing strategies to realistic outcomes based on common Long Island homeowner goals.

Costs Associated With Refinancing on Long Island

Refinancing costs in New York are often higher than national averages due to state and local requirements. Understanding these costs upfront is critical to evaluating the overall value of refinancing.

Common refinancing costs may include:

- Loan origination fees

- Appraisal expenses

- Title insurance

- Recording and filing fees

- Applicable state or county charges

Because costs can vary by county and municipality, Long Island homeowners benefit from reviewing a detailed cost breakdown early in the process.

For additional consumer guidance, homeowners may consult the Consumer Financial Protection Bureau at https://www.consumerfinance.gov and the New York State Department of Financial Services at https://www.dfs.ny.gov.

Why Local Expertise Matters for Long Island Mortgage Refinancing

Refinancing on Long Island requires familiarity with neighborhood-specific property values, school district influences, and county-level administrative processes. Appraisal expectations and closing timelines can differ significantly between Nassau and Suffolk County.

Local expertise supports:

- Accurate valuation expectations

- Fewer underwriting delays

- Better alignment with neighborhood market trends

- Clear communication throughout the refinance process

This regional understanding often leads to smoother transactions and fewer unexpected issues.

How the Long Island Housing Market Influences Refinance Timing

Local market conditions can affect how refinancing unfolds. Factors such as seasonal demand, inventory levels, and neighborhood-specific appreciation trends may influence property valuations and processing timelines.

Market considerations include:

- Property condition and age

- Recent comparable sales

- Local buyer demand

- Timing relative to tax assessments

Refinancing strategies that account for these variables tend to be more resilient and predictable.

The Long Island Mortgage Refinance Process

- Define refinancing goals

- Review home equity and financial profile

- Compare refinance structures

- Submit application and documentation

- Complete appraisal and underwriting

- Review final disclosures and close

Each step benefits from working with professionals familiar with Long Island’s regulatory environment and housing market nuances.

Common Refinance Pitfalls to Avoid

- Refinancing without a clearly defined long-term goal

- Focusing on short-term outcomes instead of total loan impact

- Underestimating closing costs and timelines

- Assuming national averages apply locally

- Proceeding without local professional guidance

Avoiding these pitfalls helps protect both financial stability and home equity.

Choosing a Trusted Long Island Refinance Partner

Selecting the right lender is as important as selecting the right refinance strategy.

Jet Direct Mortgage works with Long Island homeowners to provide transparent guidance, localized expertise, and refinance solutions aligned with long-term housing and financial goals.

Key Takeaways for Long Island Mortgage Refinancing

- Refinancing is a long-term planning decision, not a one-time transaction

- Local market conditions significantly affect outcomes

- Equity should be accessed intentionally and responsibly

- Closing costs and timelines must be evaluated carefully

- Local expertise improves clarity, efficiency, and confidence

Contact Jet Direct Mortgage

Website: https://jetdirectmortgage.com

Phone: +1.800.700.4JET

Email: express@jetdirectmortgage.com

Address: 4875 Sunrise Hwy, Suite 300, Bohemia, New York 11716

Related Mortgage Programs

Homeowners considering refinancing may also benefit from reviewing additional mortgage programs that support different property types and long-term planning strategies. Exploring available loan options can help clarify how refinancing fits into broader housing and financial goals.

View available mortgage programs here:

https://jetdirectmortgage.com/home-loan-programs/

FAQ’s

What is mortgage refinancing and how does it work on Long Island?

Mortgage refinancing replaces an existing home loan with a new mortgage that may have different terms or structures. On Long Island, refinancing is shaped by higher property values, local tax considerations, and appraisal standards, making region-specific evaluation especially important.

How long does the refinancing process usually take?

The refinancing process on Long Island typically takes between 30 and 45 days. Timelines vary based on appraisal scheduling, underwriting review, documentation accuracy, and county recording requirements in Nassau or Suffolk County.

Is refinancing only useful for short-term financial changes?

Refinancing is often used for long-term planning rather than short-term adjustments. Many Long Island homeowners refinance to improve stability, align housing costs with future income expectations, or prepare for major life transitions.

Does refinancing affect long-term homeownership flexibility?

Refinancing can influence long-term flexibility by changing how equity is structured and how housing obligations fit into broader financial plans. Careful planning helps ensure refinancing supports future options rather than limiting them.

When should a homeowner consider professional guidance for refinancing?

Professional guidance is especially valuable when local property values, tax considerations, or long-term planning goals are involved. Working with a lender familiar with Long Island conditions can help homeowners evaluate options more clearly and avoid costly missteps.

Licensing and Legal Disclosure

Jet Direct Mortgage © 2025. All Rights Reserved.

Alabama Consumer Credit License – License/Registration #22632; Arizona Mortgage Banker License – Lic/Reg#:1040763; Licensed by the Department of Financial Protection and Innovation under the California Residential Mortgage Lending Act – #41DBO-81230; Colorado Mortgage Company Registration #LMB100014791; Connecticut Mortgage Lender License #20333; Delaware Lender License – License/Registration #032943; Florida Mortgage Lender Servicer License #MLD357; Licensed by the Georgia Department of Banking and Finance Company License Company – License #64345; Illinois Residential Mortgage License – Lic/Reg#:MB.6850070; Indiana DFI Mortgage Lending License No. 59981; Maine Supervised Lender License No. SLM9525; Maryland Mortgage Lender License #17365; MA Mortgage Lender License #ML3542; Michigan 1st Mortgage Broker/Lender/Servicer Registrant #FL10015703; Licensed Residential Mortgage Lender NJ Dept of Banking & Insurance #3542; New Mexico Mortgage Loan Company License 3542; Licensed Mortgage Banker NYS Department of Financial Services #B500903 – NMLS#3542; North Carolina Mortgage Lender License L-180193; Ohio Mortgage Broker Act Mortgage Banker Exemption # MBMB.850088.000; Oregon: State of Oregon ML-3542; Pennsylvania Mortgage Lender License No. 47421; South Carolina-BFI Mortgage Lender / Servicer License MLS–3542; Tennessee Mortgage License – License/Registration #17365; Texas – SML Mortgage Banker Registration; Virginia License/Registration # MC-4985; Washington Department of Financial Institutions, Consumer Loan Company License CL-3542; Wisconsin – Mortgage Banker License, #ML3542.

Experienced Chief Operating Officer with a 26 + year demonstrated history of working in the banking industry. Skilled in all aspects of the residential mortgage market . Strong business development professional with a Bachelor of Science (BS) focused in Business Administration and Management, from St. Joseph College. A direct endorsement underwriter and a licensed Mortgage Loan Originator.