Refinancing a mortgage is not a one-time financial decision. Many homeowners revisit their loan structure multiple times over the life of their home as priorities shift, household needs evolve, and financial conditions change. One of the most common—and most misunderstood—questions is how often you can refinance a mortgage.

There is no universal limit on refinancing frequency, but timing, loan type, and strategic intent all play a major role. Refinancing too often without a plan can dilute long-term benefits, while well-timed refinances can improve flexibility, stability, and overall financial efficiency.

Is There a Legal Limit on How Often You Can Refinance?

There is no federal law that limits how many times a homeowner may refinance a mortgage. As long as a borrower qualifies and lender guidelines are met, refinancing can be done repeatedly.

- Mandatory waiting or seasoning periods

- Loan program–specific rules

- Property equity requirements

- Lender qualification standards

Refinancing is permitted multiple times, but each transaction must stand on its own merit.

How Soon Can You Refinance Again?

Seasoning Periods Explained

A seasoning period refers to the minimum amount of time that must pass after closing before another refinance is allowed. These requirements vary by loan type and refinance purpose.

Typical Waiting Periods by Refinance Type

| Refinance Type | Typical Waiting Period | Key Requirements |

|---|---|---|

| Conventional Rate-and-Term | Often none to 6 months | Equity and qualification required |

| FHA Rate-and-Term | 210 days from closing | On-time payment history |

| VA Refinance | 210 days & 6 payments made | Net tangible benefit test |

| Cash-Out Refinance | 6–12 months typical | Equity thresholds apply |

These timelines exist to prevent excessive loan churn and ensure borrower benefit.

How Loan Type Influences Refinance Frequency

Conventional Mortgages

Conventional loans typically provide the most flexibility. Many lenders allow consecutive refinances with little to no mandatory waiting period, provided the borrower qualifies again and sufficient equity exists.

Government-Backed Loans

Programs backed by federal agencies include more structured requirements to protect borrowers.

- FHA loans require specific waiting periods and payment histories

- VA loans impose recoupment and seasoning rules

- USDA loans include rural eligibility and timing conditions

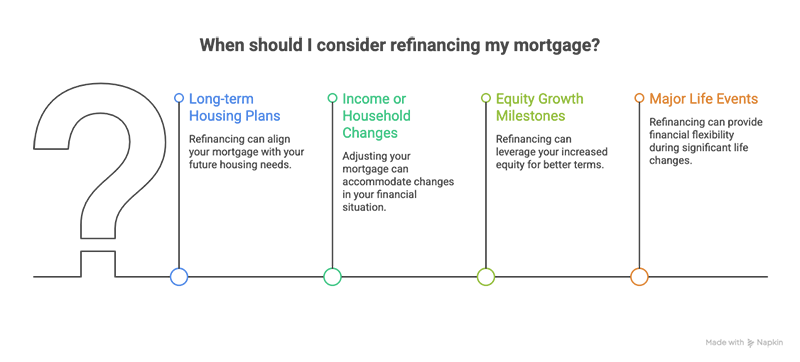

How Often Should You Refinance?

The key question is not how often refinancing is allowed—but how often it is strategically beneficial.

- Long-term housing plans

- Income or household changes

- Equity growth milestones

- Major life events

The True Cost of Refinancing Multiple Times

Costs to Consider Each Time You Refinance

| Cost Category | Description |

|---|---|

| Lender Fees | Origination and underwriting charges |

| Third-Party Services | Appraisal, title, and settlement services |

| Government Fees | Recording and state-specific charges |

| Prepaid Items | Escrow and interest adjustments |

A refinance is most effective when the benefits outweigh costs within a reasonable timeframe.

Cash-Out Refinancing: Special Frequency Rules

- Minimum ownership or seasoning period

- Maximum loan-to-value thresholds

- Demonstrated ability to manage revised payments

Refinancing vs. Loan Modification

| Refinancing | Loan Modification |

|---|---|

| Replaces existing mortgage with new loan | Adjusts terms of existing loan |

| Requires full qualification | Often used during hardship |

| Market-based restructuring | Relief-focused solution |

Frequently Asked Questions

How often can you refinance your mortgage?

There is no federally imposed limit. Refinancing can be done multiple times as long as lender requirements are met.

Is there a waiting period between refinances?

Yes, seasoning requirements vary by loan program and refinance purpose.

Does refinancing reset the loan timeline?

Yes. Refinancing replaces the existing mortgage with a new loan term.

Key Takeaways

- There is no legal limit on how often you can refinance

- Waiting periods depend on loan type

- Refinancing should support a defined financial objective

- Costs and long-term impact matter more than frequency

Contact Jet Direct Mortgage

Website: https://jetdirectmortgage.com

Phone: +1.800.700.4JET

Email: express@jetdirectmortgage.com

Address: 4875 Sunrise Hwy, Suite 300, Bohemia, New York 11716

Jet Direct Mortgage © 2026. All Rights Reserved.

NMLS: 3542

Alabama Consumer Credit License – License/Registration #22632; Arizona Mortgage Banker License – Lic/Reg#:1040763; Licensed by the Department of Financial Protection and Innovation under the California Residential Mortgage Lending Act – #41DBO-81230; Colorado Mortgage Company Registration #LMB100014791; Connecticut Mortgage Lender License #20333; Delaware Lender License – License/Registration #032943; Florida Mortgage Lender Servicer License #MLD357; Licensed by the Georgia Department of Banking and Finance Company License Company – License #64345; Illinois Residential Mortgage License – Lic/Reg#:MB.6850070; Indiana DFI Mortgage Lending License No. 59981; Maine Supervised Lender License No. SLM9525; Maryland Mortgage Lender License #17365; MA Mortgage Lender License #ML3542; Michigan 1st Mortgage Broker/Lender/Servicer Registrant #FL10015703; Licensed Residential Mortgage Lender NJ Dept of Banking & Insurance #3542; New Mexico Mortgage Loan Company License 3542; Licensed Mortgage Banker NYS Department of Financial Services #B500903 – NMLS#3542; North Carolina Mortgage Lender License L-180193; Ohio Mortgage Broker Act Mortgage Banker Exemption # MBMB.850088.000; Oregon: State of Oregon ML-3542; Pennsylvania Mortgage Lender License No. 47421; South Carolina-BFI Mortgage Lender / Servicer License MLS–3542; Tennessee Mortgage License – License/Registration #17365; Texas – SML Mortgage Banker Registration; Virginia License/Registration # MC-4985; Washington Department of Financial Institutions, Consumer Loan Company License CL-3542; Wisconsin – Mortgage Banker License, #ML3542.

All loan programs are subject to credit approval, underwriting guidelines, and property eligibility.

Experienced Chief Operating Officer with a 26 + year demonstrated history of working in the banking industry. Skilled in all aspects of the residential mortgage market . Strong business development professional with a Bachelor of Science (BS) focused in Business Administration and Management, from St. Joseph College. A direct endorsement underwriter and a licensed Mortgage Loan Originator.