What’s the Difference?

Choosing between a conventional loan vs. FHA loan is one of the most important financial decisions a homebuyer will make. The mortgage you select shapes your approval path, your upfront financial commitment, your monthly obligation, and your long-term equity strategy.

For buyers in Bohemia, Long Island, New York City, or anywhere across the country, understanding the difference between conventional and Federal Housing Administration financing is essential before submitting an offer on a home.

Both programs help people purchase homes. Both are widely used. But they operate very differently behind the scenes — from approval standards to insurance structure to long-term cost considerations.

If you’re comparing FHA vs conventional mortgage options, here’s a deep, practical breakdown designed to help you move forward confidently.

Understanding the Core Difference Between Conventional and FHA Loans

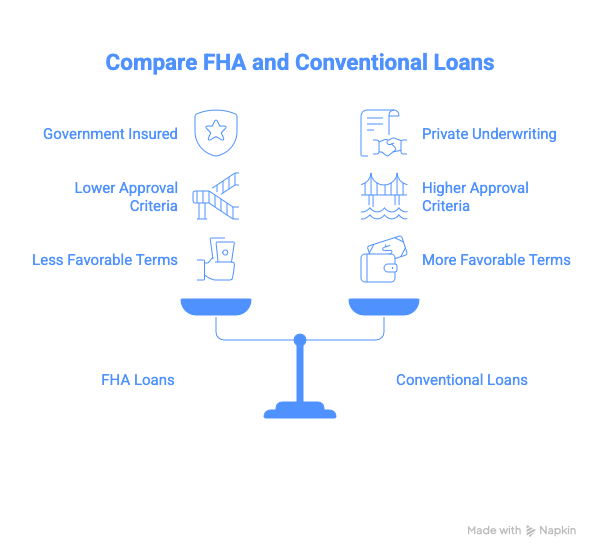

At its simplest level, the difference comes down to government insurance versus private underwriting standards.

- FHA loans are insured by the Federal Housing Administration, which operates under the U.S. Department of Housing and Urban Development (HUD).

- Conventional loans are not government-insured and follow guidelines established by federally chartered entities such as Fannie Mae and Freddie Mac.

Because FHA loans carry government insurance, lenders may approve borrowers who might not meet conventional approval criteria. Conventional loans, on the other hand, often reward stronger financial profiles with more favorable long-term structures.

Official program details can be found through:

- U.S. Department of Housing and Urban Development (HUD)

- Federal Housing Administration (FHA)

- Federal Housing Finance Agency (FHFA)

What Is a Conventional Loan?

A conventional mortgage is a home loan that is not insured by a federal agency. Instead, it follows underwriting standards set by Fannie Mae and Freddie Mac, which are regulated by the Federal Housing Finance Agency.

These loans are extremely common across the United States and are available with fixed or adjustable terms.

Core Features of Conventional Loans

- No federal insurance backing

- Available for primary residences, second homes, and investment properties

- Mortgage insurance required if equity is below 20 percent

- Mortgage insurance can typically be removed once sufficient equity is reached

- Often requires stronger credit history

Conventional financing is frequently chosen by borrowers who:

- Have established credit

- Maintain manageable debt levels

- Want long-term flexibility

Because mortgage insurance can be eliminated without refinancing once equity builds, conventional loans are often structured with long-term cost control in mind.

What Is an FHA Loan?

An FHA loan is insured by the Federal Housing Administration. That insurance protects the lender if the borrower defaults, which allows lenders to offer more flexible approval standards.

FHA financing was originally designed to expand access to homeownership and remains one of the most widely used programs for buyers entering the market.

Official FHA program guidance is available from HUD:

https://www.hud.gov/buying/loans

Core Features of FHA Loans

- Government-insured mortgage

- More flexible credit guidelines

- Lower upfront cash contribution requirements

- Requires mortgage insurance premium (MIP)

- Intended for owner-occupied properties

FHA loans are commonly used by:

- First-time homebuyers

- Borrowers rebuilding credit

- Buyers with higher debt ratios

- Individuals with limited savings

While FHA loans increase accessibility, they also include unique insurance rules that affect long-term cost.

Side-by-Side Comparison: Conventional Vs. FHA Loan

| Feature | Conventional Loan | FHA Loan |

|---|---|---|

| Government Insurance | No | Yes |

| Credit Flexibility | Moderate to Strict | More Flexible |

| Mortgage Insurance | Required below 20% equity | Required upfront and monthly |

| Insurance Removal | Yes, with equity | Limited removal options |

| Property Standards | Standard appraisal | Stricter safety standards |

| Intended Use | Primary, second, investment | Primary residence only |

Credit Standards: Which Loan Is Easier to Qualify For?

When comparing FHA vs conventional mortgage approval standards, credit history often becomes the deciding factor.

Conventional Loan Credit Expectations

- Established credit history

- Consistent payment behavior

- Lower debt-to-income ratios

FHA Credit Flexibility

FHA loans were created to help borrowers who may not meet conventional approval criteria.

FHA guidelines allow lenders to consider:

- Limited credit history

- Past financial hardship

- Higher debt ratios in certain circumstances

This flexibility is why FHA loans are frequently used by first-time buyers or individuals re-entering the housing market after financial setbacks.

Upfront Cash Requirement Differences

One of the most common borrower concerns is the initial cash required to secure a home loan.

FHA Structure

FHA loans allow a smaller initial financial contribution compared to many conventional programs. In addition, eligible gift funds may be used toward upfront costs, making it accessible for buyers with limited savings.

Conventional Structure

Conventional loans typically require a larger upfront contribution, especially for borrowers who want to avoid private mortgage insurance.

However, some conventional programs allow reduced upfront options for qualified buyers depending on income, property location, and other factors.

Loan limits for both programs are published annually:

In higher-cost areas like parts of New York, these limits significantly influence which program may be more suitable.

Mortgage Insurance: A Critical Long-Term Difference

FHA Mortgage Insurance Premium (MIP)

- An upfront mortgage insurance premium

- Ongoing monthly mortgage insurance

Conventional Private Mortgage Insurance (PMI)

Conventional loans require private mortgage insurance when equity is below 20 percent. However, once equity increases to required levels, PMI can typically be removed.

This difference means conventional loans may provide long-term cost advantages for borrowers who expect steady equity growth.

Property Requirements: Appraisal and Condition Standards

FHA and conventional loans also differ in property evaluation standards.

FHA Property Guidelines

FHA appraisals must confirm:

- The home meets minimum safety standards

- Structural components are sound

- Essential systems are functional

If deficiencies are found, repairs may be required before closing.

Conventional Property Guidelines

Conventional appraisals focus primarily on market value and overall condition but are generally less strict regarding minor cosmetic issues.

In competitive markets like Long Island or Westchester County, property conditions can influence which loan is more practical for a specific home.

Debt-to-Income Ratio Differences

Debt-to-income ratio measures how much of your gross monthly income goes toward debt obligations.

FHA Flexibility

FHA loans often allow higher debt ratios, especially when compensating factors are present.

Conventional Guidelines

Conventional loans generally prefer lower debt ratios, though automated underwriting systems may approve higher ratios for strong borrowers.

For buyers carrying student loans or auto loans, this distinction can impact eligibility.

Loan Limits and Geographic Considerations

Loan limits vary by county and are updated annually.

- FHA loan limits are established by HUD

- Conventional loan limits are set by FHFA

In counties with higher property values — including Nassau County and Suffolk County in New York — higher loan limits may allow borrowers to stay within conforming ranges.

Review current limits through the sources below:

- HUD: https://www.hud.gov

- FHFA: https://www.fhfa.gov

Understanding county-specific caps is essential when evaluating FHA vs conventional mortgage options.

Long-Term Cost Strategy

When evaluating conventional vs FHA loan options, borrowers should think beyond approval and focus on long-term financial positioning.

FHA loans may be beneficial at the beginning of a homeownership journey. However, the long-term mortgage insurance structure often leads borrowers to refinance into conventional financing once equity and credit improve.

Conventional loans, while sometimes more challenging to qualify for initially, may provide stronger long-term cost control due to removable mortgage insurance.

The better option depends on:

- Your credit profile

- Your expected time in the home

- Your equity growth strategy

- Your refinancing plans

Which Loan Is Better for First-Time Buyers?

Both programs serve first-time buyers effectively.

FHA May Be Ideal If:

- Credit history is limited

- Debt ratio is higher

- Savings are modest

- Rebuilding financial stability

Conventional May Be Ideal If:

- Credit is strong

- Long-term cost reduction is a priority

- You want mortgage insurance removed without refinancing

In competitive housing markets, some sellers may view conventional financing as stronger due to fewer property repair requirements.

Refinancing From FHA to Conventional

Many homeowners begin with FHA financing and later transition to conventional.

Common reasons include:

- Building sufficient equity

- Improving credit profile

- Eliminating mortgage insurance

- Restructuring loan terms

Refinancing decisions should consider total savings over time and break-even timelines.

Conventional vs. FHA Loan: Questions Homebuyers Ask Most

What is the primary difference between conventional and FHA loans?

The primary difference is that FHA loans are insured by the federal government, while conventional loans are not government-backed and follow private underwriting guidelines.

Which loan type is more flexible with credit?

FHA loans generally allow more flexible credit standards, making them suitable for borrowers with limited or recovering credit histories.

Can mortgage insurance be removed?

Conventional loan mortgage insurance can typically be removed once sufficient equity is achieved. FHA mortgage insurance often requires refinancing for removal.

Are FHA loans only for first-time buyers?

No. FHA loans are available to repeat buyers, provided they meet eligibility requirements and the home will be owner-occupied.

Key Takeaways

- FHA loans are government-insured and designed for accessibility.

- Conventional loans follow investor guidelines and may reward stronger financial profiles.

- Mortgage insurance structure is a major cost differentiator.

- Property standards differ between programs.

- Long-term financial goals should guide the decision.

Selecting the right mortgage program is not about which loan is “better.” It is about which loan aligns with your current financial position and future plans.

Work With Jet Direct Mortgage

Choosing between a conventional loan vs FHA loan requires personalized evaluation.

Jet Direct Mortgage helps homebuyers and homeowners across New York and beyond evaluate their options with clarity and precision.

Contact us today:

JetDirectMortgage.com

Call: +1.800.700.4JET

Email: express@jetdirectmortgage.com

4875 Sunrise Hwy, Suite 300

Bohemia, New York 11716

Explore Additional Mortgage Programs

Learn more about available home loan solutions:

https://jetdirectmortgage.com/home-loan-programs/

FAQ’s

Is it harder to qualify for a conventional loan compared to an FHA loan?

Conventional loans often require stronger credit history and lower debt ratios compared to FHA financing. FHA loans are generally more flexible, which can make them easier to qualify for if your credit profile is still developing.

Why does FHA mortgage insurance last longer?

FHA mortgage insurance protects the lender and remains in place for an extended period under many loan scenarios. In most cases, it remains until the loan is refinanced into a conventional product.

Do conventional loans always require a large upfront payment?

Not always. While conventional loans may require more upfront funds than FHA loans in some cases, certain programs allow reduced upfront options depending on borrower qualifications.

Which loan is more cost-effective long term?

For borrowers with strong credit and steady equity growth, conventional loans may provide better long-term cost efficiency due to the ability to remove mortgage insurance without refinancing.

Can I switch loan types after purchasing a home?

Yes. Many borrowers refinance from FHA to conventional financing once their financial profile improves, allowing them to eliminate mortgage insurance and potentially adjust loan terms.

Jet Direct Mortgage © 2025. All Rights Reserved.

NMLS: 3542

Alabama Consumer Credit License – License/Registration #22632; Arizona Mortgage Banker License – Lic/Reg#:1040763; Licensed by the Department of Financial Protection and Innovation under the California Residential Mortgage Lending Act – #41DBO-81230; Colorado Mortgage Company Registration #LMB100014791; Connecticut Mortgage Lender License #20333; Delaware Lender License – License/Registration #032943; Florida Mortgage Lender Servicer License #MLD357; Licensed by the Georgia Department of Banking and Finance Company License Company – License #64345; Illinois Residential Mortgage License – Lic/Reg#:MB.6850070; Indiana DFI Mortgage Lending License No. 59981; Maine Supervised Lender License No. SLM9525; Maryland Mortgage Lender License #17365; MA Mortgage Lender License #ML3542; Michigan 1st Mortgage Broker/Lender/Servicer Registrant #FL10015703; Licensed Residential Mortgage Lender NJ Dept of Banking & Insurance #3542; New Mexico Mortgage Loan Company License 3542; Licensed Mortgage Banker NYS Department of Financial Services #B500903 – NMLS#3542; North Carolina Mortgage Lender License L-180193; Ohio Mortgage Broker Act Mortgage Banker Exemption # MBMB.850088.000; Oregon: State of Oregon ML-3542; Pennsylvania Mortgage Lender License No. 47421; South Carolina-BFI Mortgage Lender / Servicer License MLS–3542; Tennessee Mortgage License – License/Registration #17365; Texas – SML Mortgage Banker Registration; Virginia License/Registration # MC-4985; Washington Department of Financial Institutions, Consumer Loan Company License CL-3542; Wisconsin – Mortgage Banker License, #ML3542;