The Complete 2026 Homeowner’s Guide

Refinancing a mortgage in Nassau County is not just a financial transaction — it is a strategic decision shaped by property values, local regulations, loan structure, and long-term homeownership goals. From Garden City and Mineola to Massapequa, Great Neck, and Long Beach, Nassau homeowners operate in one of the most competitive real estate markets in New York.

Understanding how to refinance a mortgage in Nassau County means understanding equity, loan structure, costs, documentation, and local closing procedures. Whether your goal is to adjust your loan term, restructure monthly payments, access equity, or move into a different mortgage product, the process requires clarity and precision.

What Does It Mean to Refinance a Mortgage in Nassau County?

Refinancing replaces your existing mortgage with a new loan. The new mortgage pays off your current balance and establishes updated loan terms.

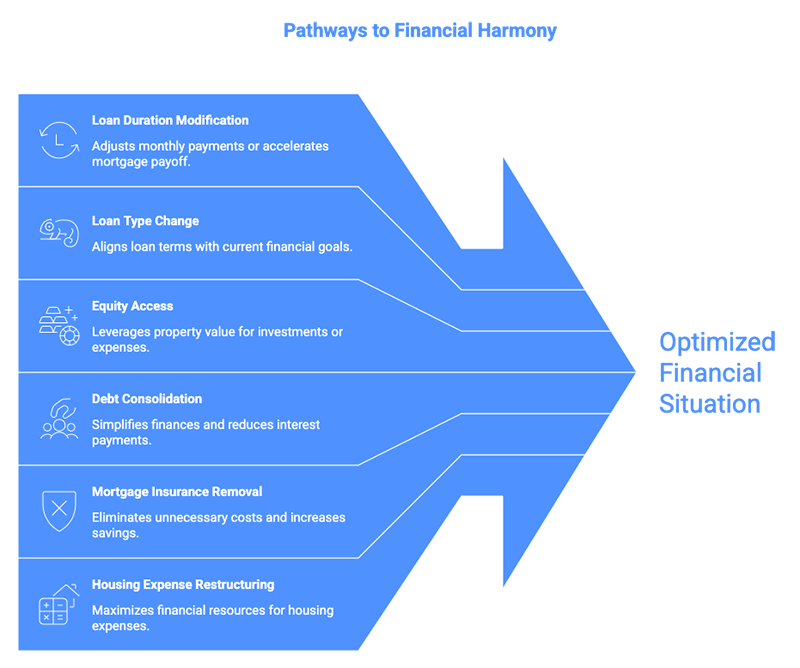

When homeowners refinance in Nassau County, they typically aim to:

- Modify loan duration

- Change loan type

- Access built-up equity

- Consolidate other debts

- Remove mortgage insurance

- Restructure overall housing expenses

Because Nassau County property values are generally higher than many parts of the country, homeowners often build equity faster — making refinancing a practical financial tool when executed properly.

Why Nassau County Homeowners Consider Refinancing

Equity Growth in Long Island’s Housing Market

Nassau County has historically maintained strong home values, particularly in North Shore and central Nassau communities. Over time, consistent property appreciation and principal reduction can create substantial equity positions.

Equity may allow homeowners to:

- Transition into a conventional mortgage

- Remove mortgage insurance

- Access funds for renovations

- Consolidate higher-cost financial obligations

Loan Restructuring for Stability

Some borrowers refinance to move from an adjustable loan into a fixed structure for payment predictability. Others shorten their repayment timeline to align with retirement planning or long-term financial goals.

Financial Rebalancing

Refinancing can also provide flexibility when restructuring household finances. This may include consolidating obligations into one mortgage payment or adjusting the repayment term to better fit future income projections.

Types of Mortgage Refinance Options in Nassau

Understanding the right refinance structure is essential. The most common refinance options available to Nassau County homeowners include:

1. Rate-and-Term Refinance

This is the most straightforward refinance option. It modifies your loan’s structure without withdrawing equity.

Common goals include:

- Adjusting loan duration

- Changing from adjustable to fixed

- Eliminating mortgage insurance

- Improving overall loan stability

This option works well for homeowners focused on long-term restructuring rather than accessing funds.

2. Cash-Out Refinance

A cash-out refinance allows you to replace your current mortgage with a larger loan and receive the difference in funds. In Nassau County, where home values often exceed state averages, this can be a powerful equity strategy.

Homeowners commonly use cash-out refinancing to:

- Renovate kitchens or bathrooms

- Upgrade roofing or energy systems

- Fund college tuition

- Consolidate higher-cost obligations

Because property values vary between neighborhoods, an appraisal is typically required to confirm available equity.

3. FHA Refinance Programs

Homeowners with Federal Housing Administration loans may qualify for refinance options backed by the Federal Housing Administration. These programs are designed to provide flexibility under specific eligibility guidelines.

Official program information can be found through the U.S. Department of Housing and Urban Development:

https://www.hud.gov/program_offices/housing/fhahistory

4. VA Refinance Programs

Eligible veterans may refinance through programs supported by the U.S. Department of Veterans Affairs. These options are available to qualified service members and may provide streamlined refinance pathways.

Official VA refinance guidance:

https://www.va.gov/housing-assistance/home-loans/

5. Conventional Refinance

Conventional refinancing is common in Nassau County due to higher property values. Borrowers with sufficient equity often move into conventional loans to remove mortgage insurance and simplify long-term repayment structures.

Step-by-Step: How to Refinance a Mortgage in Nassau County

Step 1: Define Your Objective

Before beginning the process, determine your primary goal. Are you restructuring long-term payments? Accessing equity? Adjusting loan length? Clear objectives help determine the most suitable loan type.

Step 2: Review Your Existing Loan

Collect your current mortgage statement and confirm:

- Remaining balance

- Loan term

- Escrow details

- Mortgage insurance status

Step 3: Evaluate Financial Standing

Lenders typically review:

- Credit profile

- Employment consistency

- Income documentation

- Debt-to-income ratio

The Consumer Financial Protection Bureau provides mortgage education resources:

https://www.consumerfinance.gov/consumer-tools/mortgages/

Step 4: Property Valuation

In Nassau County, valuation depends heavily on neighborhood, school district, proximity to waterfront, and housing type. A licensed appraiser confirms value before final loan approval.

Step 5: Submit Documentation

Typical refinance documentation includes:

- W-2s or 1099s

- Federal tax returns

- Bank statements

- Pay stubs

- Proof of homeowners insurance

Step 6: Underwriting Review

The lender verifies eligibility and financial stability before issuing final approval.

Step 7: Closing Process in Nassau County

Refinancing in New York often involves attorney participation. Title review, recording fees, and documentation review are standard components of Nassau County closings.

Nassau County–Specific Considerations

Property Taxes and Escrow

Nassau County is widely known for elevated property taxes compared to national averages. While refinancing does not directly reduce your tax rate, it may adjust how taxes are collected through escrow.

If your lender escrows taxes and homeowners insurance, changes in loan balance or escrow structure can affect your monthly mortgage payment. Understanding how taxes integrate into your payment is especially important for budgeting purposes after refinancing.

Co-Op and Condo Refinancing in Nassau

Co-ops and condominiums are common throughout Nassau County, particularly in areas such as Great Neck and Mineola. Refinancing these properties differs from single-family homes. Co-op loans are technically share loans, since ownership involves shares in a corporation rather than direct real estate ownership.

Condo refinancing often requires homeowners association documentation, occupancy ratios, and financial review of the association itself. Because underwriting for these properties can be more complex, working with a lender experienced in Long Island co-op and condo financing is critical for smooth processing.

Refinancing Costs in Nassau County

| Cost Category | Estimated Range | Required | Notes |

|---|---|---|---|

| Appraisal | $500–$900 | Often | Property dependent |

| Title Insurance | Varies | Yes | NY-specific |

| Recording Fees | Varies | Yes | Nassau County filing |

| Lender Fees | Varies | Yes | Loan program dependent |

How Long Does It Take to Refinance in Nassau?

- Application and documentation: 1–5 days

- Processing and appraisal: 2–3 weeks

- Underwriting review: 1–2 weeks

- Closing preparation: Final week

Average total timeframe: 30–45 days.

When Refinancing Makes Sense in Nassau

Refinancing is often beneficial when:

- You plan to remain in the home for several years

- Equity levels are strong

- You want to remove mortgage insurance

- You are restructuring long-term financial planning

It may be less advantageous if selling in the near future, as closing costs require time to offset.

Refinance vs. Home Equity Loan Comparison

| Feature | Mortgage Refinance | Home Equity Loan |

| Replaces current loan | Yes | No |

| Provides lump sum | Yes (cash-out) | Yes |

| Single mortgage payment | Yes | No |

| Requires closing | Yes | Yes |

| Best for | Loan restructuring | Secondary borrowing |

Key Takeaways for Nassau County Homeowners

- Refinancing replaces your existing mortgage with updated terms.

- Nassau County property values often create meaningful equity opportunities.

- Co-op and condo refinances require specialized underwriting.

- Attorney involvement is common in New York refinance closings.

- Evaluating long-term residency plans is critical before refinancing.

Start Your Nassau Refinance with Jet Direct Mortgage

Refinancing requires local expertise, regulatory knowledge, and precision. Jet Direct Mortgage provides experienced support for Nassau County homeowners.

Contact Jet Direct Mortgage

Website: https://jetdirectmortgage.com

Phone: +1.800.700.4JET

Email: express@jetdirectmortgage.com

Address: 4875 Sunrise Hwy, Suite 300, Bohemia, New York 11716

Explore Additional Home Loan Programs

View all available mortgage solutions:

https://jetdirectmortgage.com/home-loan-programs/

FAQs

1. How do I refinance my mortgage in Nassau County step by step?

Begin by identifying your financial objective and reviewing your current mortgage statement. Contact a licensed lender familiar with Nassau County properties, submit required documentation, complete the appraisal process, proceed through underwriting review, and finalize the refinance at closing with attorney oversight if required.

2. How much equity do I typically need to refinance in Nassau County?

Most conventional refinance programs prefer at least 20 percent equity for optimal loan structures, though requirements vary depending on loan type. Government-backed programs may allow different thresholds, but equity strength significantly impacts approval flexibility and overall loan options.

3. How long does refinancing take in Nassau County?

Refinancing in Nassau County typically takes between 30 and 45 days from application to closing. Timeline factors include appraisal scheduling, underwriting review, attorney coordination, and documentation completeness. Co-op and condo refinances may require additional review time.

4. Will refinancing affect my property taxes in Nassau County?

Refinancing does not directly change your Nassau County property tax rate or assessment. However, if taxes are included in escrow, adjustments in loan balance or escrow collection structure may alter your monthly payment amount.

5. Is refinancing worth it if I plan to move in a few years?

Refinancing may not be ideal if you plan to sell shortly, since closing costs require time to offset. Evaluating your projected length of homeownership against total refinance costs helps determine whether the transaction aligns with your financial goals.

Jet Direct Mortgage © 2025. All Rights Reserved.

NMLS: 3542

Alabama Consumer Credit License – License/Registration #22632; Arizona Mortgage Banker License – Lic/Reg#:1040763; Licensed by the Department of Financial Protection and Innovation under the California Residential Mortgage Lending Act – #41DBO-81230; Colorado Mortgage Company Registration #LMB100014791; Connecticut Mortgage Lender License #20333; Delaware Lender License – License/Registration #032943; Florida Mortgage Lender Servicer License #MLD357; Licensed by the Georgia Department of Banking and Finance Company License Company – License #64345; Illinois Residential Mortgage License – Lic/Reg#:MB.6850070; Indiana DFI Mortgage Lending License No. 59981; Maine Supervised Lender License No. SLM9525; Maryland Mortgage Lender License #17365; MA Mortgage Lender License #ML3542; Michigan 1st Mortgage Broker/Lender/Servicer Registrant #FL10015703; Licensed Residential Mortgage Lender NJ Dept of Banking & Insurance #3542; New Mexico Mortgage Loan Company License 3542; Licensed Mortgage Banker NYS Department of Financial Services #B500903 – NMLS#3542; North Carolina Mortgage Lender License L-180193; Ohio Mortgage Broker Act Mortgage Banker Exemption # MBMB.850088.000; Oregon: State of Oregon ML-3542; Pennsylvania Mortgage Lender License No. 47421; South Carolina-BFI Mortgage Lender / Servicer License MLS–3542; Tennessee Mortgage License – License/Registration #17365; Texas – SML Mortgage Banker Registration; Virginia License/Registration # MC-4985; Washington Department of Financial Institutions, Consumer Loan Company License CL-3542; Wisconsin – Mortgage Banker License, #ML3542;