Having a low credit score doesn’t mean that you can’t be a homeowner. But if you are trying to qualify for a 600 credit score home loan in New York, you might be wondering: is that even possible? Which lenders will consider my application?

What kind of loan programs can I choose from? And what steps can I take right now to improve my chances of getting approved?

At Jet Direct Mortgage, we know that this process can be confusing, and that you may feel a little bit lost. We get it; it’s a big step, and without the right guidance, you can easily end up applying to the wrong lenders or choosing a loan that doesn’t truly fit your situation.

In this article, we’ll walk you through the 5 key steps you’ll need to take to qualify for a 600 credit score home loan. From improving your financial profile to choosing the right loan program, we will give some practical insights so you can move forward with confidence.

Let’s get started:

Can I Qualify For a 600 Credit Score Home Loan in New York?

Before we get into the practical steps, let’s get one key question out of the way: can you really qualify for a 600 credit score home loan? And we have good news for you.

Yes, you can qualify for a 600 credit score home loan in New York. Many lenders offer programs like FHA loans that accept scores around 580–600, depending on your financial profile. Approval will also depend on factors like your income, debt-to-income ratio, and down payment.

Some mortgage lenders with a low credit score may be more flexible and consider your overall financial stability.

5 Steps to Qualify For a 600 Credit Score Home Loan

1. Check and Improve Your Credit Profile

So, before you do anything else, you need to understand exactly where you stand. If you’re aiming to qualify for a 600 credit score home loan, your credit profile will be one of the first things lenders evaluate, and even small improvements can make a difference.

Essentially, they want to know if you are able to reliably manage your debt. Your credit score is just the surface. Lenders go deeper into your full credit report, focusing on:

- Payment history (35%) → Have you paid on time recently?

- Credit utilization (30%) → How much of your available credit are you using?

- Length of credit history (15%)

- Credit mix (10%)

- Recent inquiries (10%)

Here are some things that you can start doing to improve your credit score as much as possible in order to qualify for a 600 credit score home loan:

1.1 Audit Your Credit Report

Before making any moves, pull your full credit reports from all three bureaus:

Look specifically for incorrect late payments, accounts that aren’t yours, duplicate debts, or incorrect balances. Even one removed error has the potential to boost your score significantly, sometimes up to 50 points.

1.2. Lower Your Credit Utilization

If you’re carrying balances, lowering your credit utilization is the quickest way to improve your score in order to qualify for a 600 credit score home loan. Aim for under 30% utilization, but under 10% will be ideal.

For example, if you have a $1,000 limit, make sure to keep your balance under $300. Paying down balances can improve your score in as little as 30 days.

1.3. Fix Your Payment History

Late payments hurt your credit score more than anything else, so keep that in mind before you apply for a home loan. At Jet Direct Mortgage, we recommend setting up auto-payments, and avoid any late ones at all cost.

If you missed payments, call creditors and request a goodwill adjustment. Most lenders care more about recent behavior than old mistakes.

1.4. Avoid Common Mistakes

When preparing for a mortgage with a 600 credit score, avoid:

- Opening new credit accounts

- Applying for multiple loans or cards

- Closing old accounts (can hurt your score)

- Making large purchases on credit

Keep in mind that every hard inquiry or new account can temporarily lower your score, which might prevent you from qualifying for a 600 credit score home loan.

1.5. Show Positive Momentum

Many borrowers don’t realize that when it comes to how to qualify for a 600 credit score home loan, lenders don’t rely solely on your current score, they closely evaluate your overall credit trends.

If your profile shows consistent on-time payments, steadily decreasing balances, and no recent negative marks, it signals financial responsibility and improvement.

This kind of positive momentum can significantly strengthen your application, making you a more attractive borrower even if your credit score is around 600.

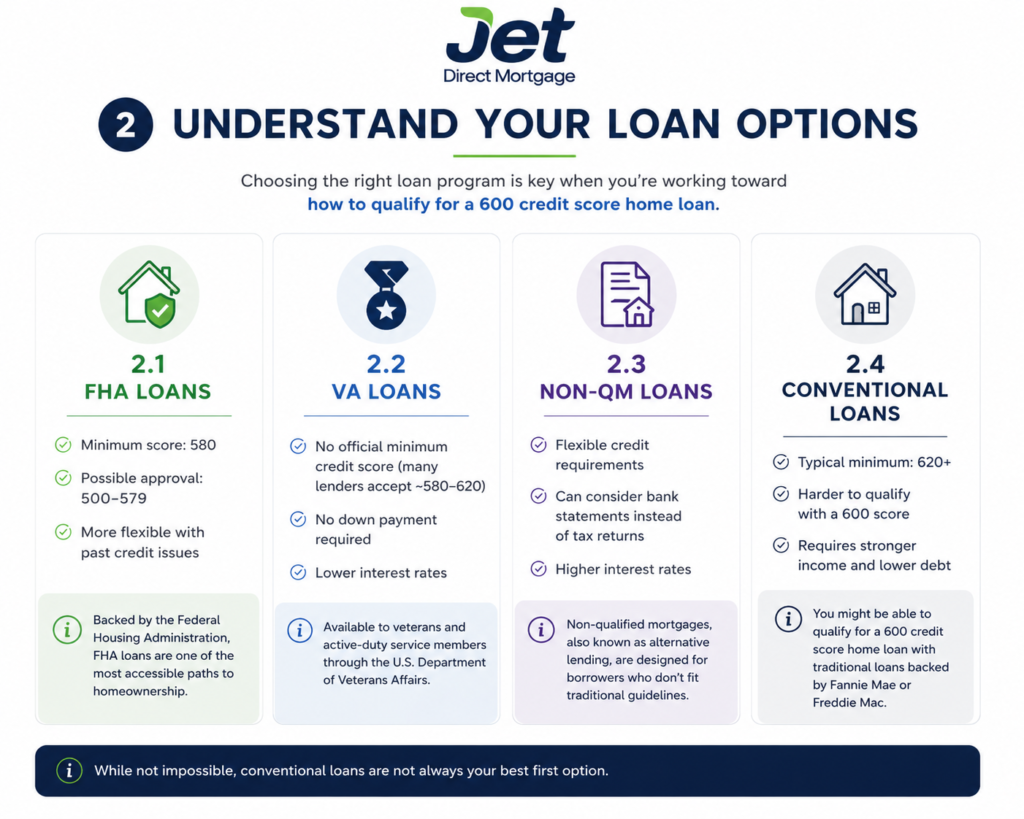

2. Understand Your Loan Options

If you’re serious about how to qualify for a 600 credit score home loan, choosing the right loan program is just as important as improving your credit. Not every mortgage is designed for borrowers with lower scores, and applying for the wrong one can lead to unnecessary rejections or delays.

So, which are the best loan options for a 600 credit score?

2.1. FHA Loans

Backed by the Federal Housing Administration, FHA loans are one of the most accessible paths to homeownership.

- Minimum score: 580

- Possible approval: 500–579

- More flexible with past credit issues

2.2. VA Loans

Available to veterans and active-duty service members through the U.S. Department of Veterans Affairs, VA loans can be another option depending on your eligibility.

- No official minimum credit score (many lenders accept ~580–620)

- No down payment required

- Lower interest rates

2.3. Non-QM Loans

Non-qualified mortgages, also known as alternative lending, are designed for borrowers who don’t fit traditional guidelines.

- Flexible credit requirements

- Can consider bank statements instead of tax returns

- Higher interest rates

2.4. Conventional Loans

You might be able to qualify for a 600 credit score home loan with traditional loans backed by Fannie Mae or Freddie Mac.

- Typical minimum: 620+

- Harder to qualify with a 600 score

- Requires stronger income and lower debt

While not impossible, conventional loans are not always your best first option.

3. Lower Your Debt-to-Income Ratio (DTI)

When it comes to how to qualify for a 600 credit score home loan in New York, your debt-to-income ratio (DTI) can be just as important as your credit score.

Lenders don’t just want to know if you pay your debts, they want to know how much of your monthly income is already committed. Your DTI measures this by comparing your total monthly debt payments to your gross monthly income, giving lenders a clear picture of your financial capacity.

Even with a 600 credit score, a lower DTI can significantly improve your chances of approval. It shows that you’re not overextended and that you’ll be able to handle a new mortgage payment without financial strain.

In many cases, borrowers with slightly lower credit scores but strong DTI ratios are viewed as less risky than those with higher scores but heavy debt loads.

What is a good DTI?

- Most lenders prefer: below 43%

- Stronger applications: below 36%

- FHA loans may allow higher, depending on your profile

In order to lower your DTI, you should:

- Pay down high-interest debt first

- Avoid taking on new debt

- Increase your income (if possible)

- Refinance or consolidate debt

- Pay off smaller balances completely

4. Save for a Strong Down Payment

When you’re working on how to qualify for a 600 credit score home loan, your down payment becomes one of your strongest advantages. While your credit score reflects past behavior, your down payment shows current financial discipline and commitment, and lenders pay close attention to that.

A larger down payment helps reduce the lender’s risk. It means you’re borrowing less relative to the home’s value, which can make your application more appealing even if your credit score isn’t perfect. In many cases, this can lead to better loan terms, smoother approval, and more flexibility during underwriting.

Beyond approval, a strong down payment also improves your overall financial position. It can lower your monthly payment, reduce the total interest you pay over time, and potentially minimize additional costs tied to higher-risk loans.

More importantly, it signals to lenders that you’re serious, prepared, and financially stable; qualities that matter just as much as your credit score when evaluating how to qualify for a 600 credit score home loan.

5. Get Pre-Approved with the Right Lender in New York

When you’re navigating how to qualify for a 600 credit score home loan, who you choose as your lender can make or break the process.

Not all lenders evaluate applications the same way; some rely strictly on credit scores, while others take a more holistic approach, looking at your income, recent financial improvements, and overall stability.

This is where working with a lender like Jet Direct Mortgage can make a real difference. They specialize in helping borrowers with a wide range of credit profiles, including those around the 600 range, and focus on finding solutions rather than issuing quick denials.

Getting pre-approved is more than just a formality, it’s a strategic step. It gives you a clear understanding of what you can afford, what loan programs you qualify for, and what adjustments (if any) can improve your chances before you officially apply.

What Loan Amount Can You Get With a 600 Credit Score?

When it comes to how much you can get approved for with a 600 credit score, your credit score is only one piece of the puzzle. The actual loan amount you qualify for depends much more on your income, debt, and overall financial profile than the score itself.

Two people with the same 600 score can be approved for completely different amounts, sometimes dramatically different. Most borrowers fall into the $150K–$400K+ range.

Lenders calculate how much you can afford based on a few key factors:

- Your income – the higher and more stable it is, the more you can qualify for

- Your debt-to-income ratio (DTI) – lower monthly debt = higher approval amount

- Your down payment – more upfront = lower loan needed

- Interest rate – affects how much home fits into your monthly budget

- Loan program – FHA, VA, and other options have different limits and flexibility

Ready to qualify for a 600 credit score home loan? Let’s get you started.

FAQ

What income do I need to qualify for a 600 credit score home loan?

There’s no fixed income requirement to qualify for a 600 credit score home loan. Lenders focus on your debt-to-income ratio (DTI), income stability, and consistency rather than a specific salary.

Higher, well-documented income can increase your approval chances and loan amount, especially when paired with lower debt and a strong financial profile.

How much can I borrow with a 600 credit score home loan in New York?

With a 600 credit score home loan in New York, borrowing amounts typically range from moderate to higher tiers depending on your income, debt, and interest rate.

Lenders calculate affordability based on your monthly income and obligations, not just your score. Strong income and low debt can significantly increase your borrowing power even with a 600 credit score.

What debt-to-income ratio is required to qualify with a 600 credit score?

To qualify for a 600 credit score home loan, most lenders prefer a debt-to-income ratio below 43%, though some programs may allow higher with compensating factors.

A lower DTI improves approval chances by showing you can manage monthly payments comfortably. Reducing debt before applying can significantly strengthen your application.

Can I get an FHA loan with a 600 credit score in Long Island?

Yes, you can qualify for an FHA loan with a 600 credit score in Long Island. FHA loans are designed for borrowers with lower credit and offer more flexible requirements than conventional loans.

Approval depends on additional factors like income, DTI, and down payment, but FHA remains one of the most accessible options for lower credit borrowers.

How can I improve my chances of approval with a 600 credit score?

To improve approval odds for a 600 credit score home loan, focus on lowering debt, making consistent on-time payments, and avoiding new credit inquiries.

Strengthening your down payment and showing stable income can also help. Lenders value recent positive financial behavior, so even small improvements can significantly boost your chances.

Can I get approved for a mortgage with a 600 credit score?

Yes, it’s possible to get approved for a mortgage with a 600 credit score, especially through flexible loan programs like FHA.

Approval depends on your full financial profile, including income, DTI, and down payment. Working with the right lender and demonstrating financial stability can significantly increase your chances of getting approved.