So, you are looking to take a mortgage with a low credit score in New York, but you don’t know where to start. We get it; making such a big financial decision can be overwhelming, especially if you don’t know how to choose the right lender.

The truth is, having a low credit score doesn’t automatically disqualify you, but it does mean you need to be more strategic. Not all lenders evaluate applications the same way, and the difference between a good and a bad choice can determine whether you get approved at all, and under what terms.

In this article, we will tell you everything you need to know about using mortgage lenders with a low credit score in New York: from interest rates and hidden fees to loan requirements and flexibility. Our team at Jet Direct Mortgage has prepared this detailed go-to guide so you can improve your chances of getting approved, and avoid costly mistakes.

If that’s what you are here for, let’s get right into it:

Mortgage Lenders with a Low Credit Score in New York: 7 Key Checks

1. Pay Attention To The Minimum Credit Score Requirements

So, before anything else, you need to understand one simple truth: not all lenders play by the same rules.

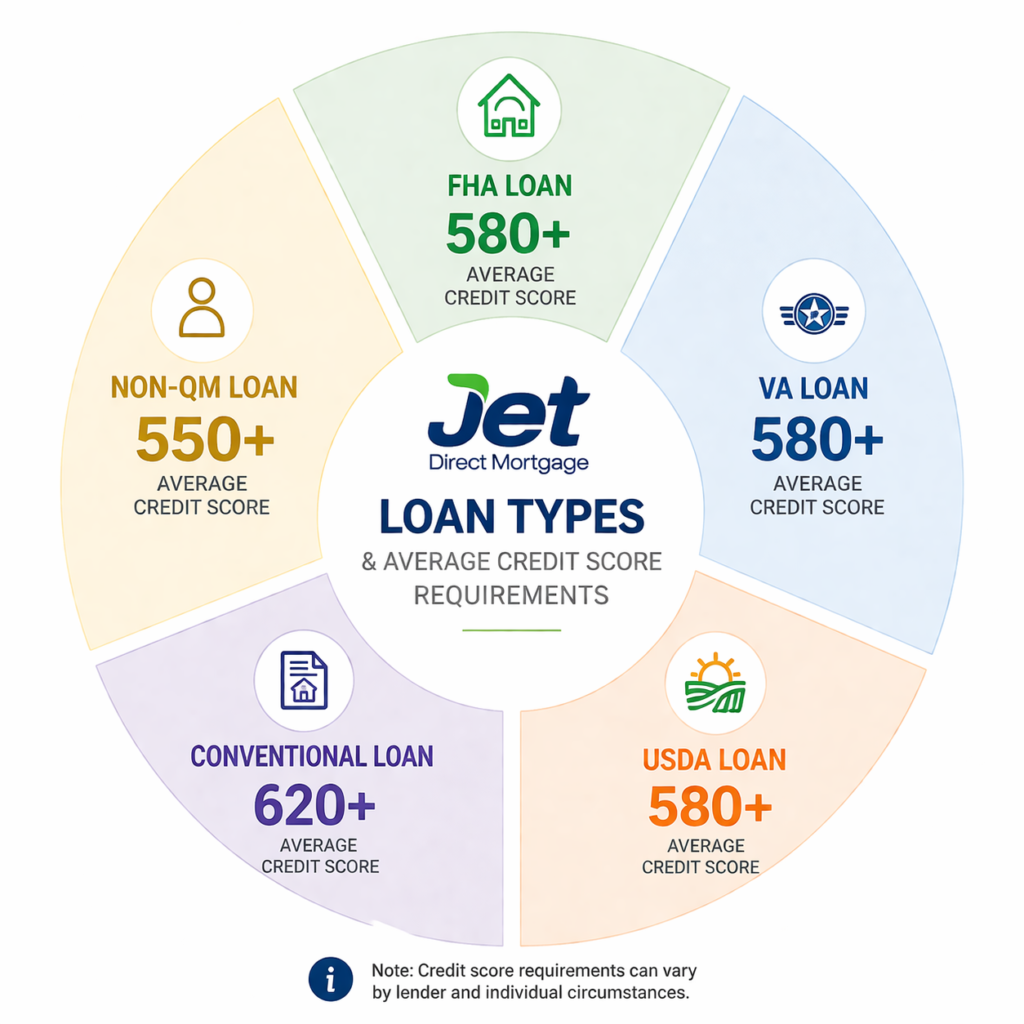

Some mortgage lenders with a low credit score are willing to work with borrowers in the 500–580 range, especially through government-backed programs. However, others won’t even consider an application below 620, which is the standard minimum for most conventional loans.

In other words, there isn’t a universal “cut-off”. In fact, some programs are designed specifically for borrowers with less-than-perfect credit. For example, FHA loans can offer up to higher percentages of financing, and are more flexible with credit requirements. This makes them a good option if you are looking for mortgage lenders with a low credit score in New York.

But here’s the reality most people don’t talk about: applying without knowing these thresholds can hurt you. Every rejected application can trigger a hard inquiry, which may lower your score even further.

And statistically, mortgage denials are more common than you think: about 1 in 9 applications gets denied, often because borrowers don’t meet the requirements of the lender that they are applying with.

2. Check The Loan Types That The Lender Offers

Another important thing that you need to check when it comes to using mortgage lenders with a low credit score in New York is the types of loans that they actually offer. Keep in mind that not every loan is designed for every borrower, especially if your credit score is not high.

Some mortgage lenders with a low credit score specialize in programs that are specifically built to be more flexible, while others focus almost entirely on conventional loans with stricter requirements.

This is where understanding your options becomes key. For example, FHA loans are one of the most common paths for borrowers with lower credit, often allowing scores as low as 580, and in some cases even lower with a larger upfront contribution.

These loans are backed by the government, which reduces the risk for lenders and makes approval more accessible.

But FHA isn’t the only route. Depending on your situation, you may also come across:

- VA loans (for eligible veterans and active-duty service members), which can offer more flexible credit guidelines

- USDA loans, designed for rural and suburban buyers, sometimes with more lenient requirements

- Non-QM (non-qualified mortgage) loans, which allow lenders to evaluate factors beyond just your credit score

The key here is not to assume that all lenders offer all loan types, because we can already tell you that they don’t. Some mortgage lenders with a low credit score focus heavily on FHA and government-backed programs, while others may not offer them at all.

At the end of the day, the loan you choose will shape your entire mortgage experience, from how easy it is to get approved to how manageable your payments feel over time. And when your credit score isn’t perfect, choosing the right loan type is key.

3. Understand The Down Payment Requirements

So, here’s something many borrowers don’t fully realize upfront: when you’re working with mortgage lenders with a low credit score, your down payment becomes a much bigger part of the equation. It’s not just about how much you can afford, it’s about how much confidence you can show to the lender.

In practical terms, a lower credit score often means you’ll be expected to put more money down. But the exact amount can vary depending on the loan type.

This is where strategy starts to matter. A higher down payment can sometimes compensate for a lower credit score, improving your chances of approval and making you a more attractive borrower overall. In fact, lenders often view larger upfront contributions as a sign of financial stability and lower risk.

That’s why it’s important to know your numbers before applying. Look at how much you can realistically put down, but also explore programs that could support you. Many borrowers aren’t aware that down payment assistance programs exist at the state and local level, and in some cases, they can significantly reduce the upfront burden.

Here are a few questions that you can ask mortgage lenders with a low credit score:

- What is the minimum down payment required based on my current credit score?

- Would increasing my down payment improve my chances of approval?

- Are there specific loan programs that allow lower down payments in my situation?

- Do you offer or work with any down payment assistance programs?

- How does my down payment impact my interest rate or loan terms?

- Are there any grants, credits, or incentives I may qualify for?

- What is the total upfront cash I’ll need at closing, beyond the down payment?

4. Get Familiar With The Debt-to-Income (DTI) Ratio Limits

So, while your credit score gets most of the attention, it’s not the only number lenders care about.

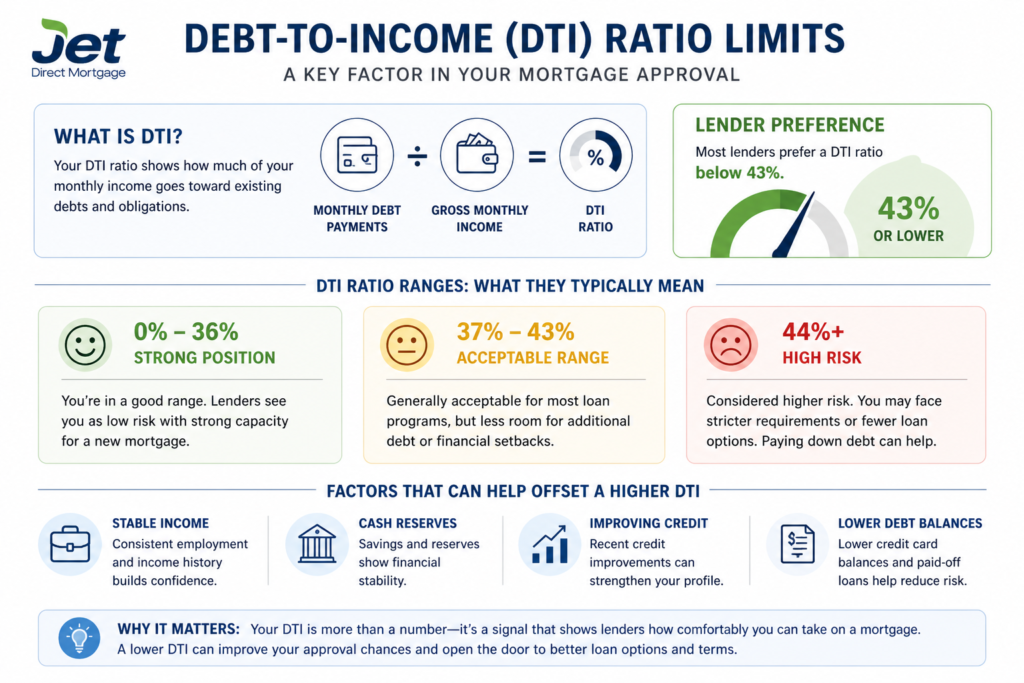

Your debt-to-income (DTI) ratio plays a major role in how lenders evaluate your application: it shows how much of your monthly income is already going toward existing obligations like credit cards, car loans, or student debt.

In most cases, lenders prefer a DTI ratio below 43%, although some programs may allow higher thresholds depending on the full financial picture.

This is where things can vary. Some mortgage lenders with a low credit score may be more flexible and consider compensating factors like stable income or cash reserves, while others apply stricter limits regardless of your situation.

This is why knowing your DTI before applying is so important. It gives you a clear sense of whether you’re in a strong position, or whether it might make sense to pay down some debt first. Even small improvements can make a noticeable difference in how your application is viewed.

At the end of the day, your DTI isn’t just a number, it’s a signal. It tells mortgage lenders with a low credit score how comfortably you can take on a mortgage, and it can directly influence both your approval chances and the type of loan options available to you.

5. Check The Interest Rate Structure That The Lender Offers

Getting approved is one thing, but understanding the terms is another. When you’re working with mortgage lenders with a low credit score in New York, interest rates can vary more than you might expect, and even small differences can shape your overall financial commitment.

That’s why it’s important to look beyond the initial rate you’re quoted.

Ask yourself: is it a fixed-rate mortgage, where your payments stay consistent over time, or an adjustable-rate mortgage (ARM), where the rate can change after an initial period? And if it’s adjustable, how often does it reset, and by how much?

For borrowers with lower credit scores, lenders may price in additional risk, which can result in higher starting rates or less favorable adjustments over time. But this isn’t always set in stone. Some lenders offer more competitive structures depending on factors like your down payment, income stability, or overall financial profile.

The key here is clarity. Understanding how your rate works today, and how it could change in the future, helps you make a more informed decision. Because in the long run, it’s not just about getting approved: it’s about choosing a loan that remains manageable over time.

6. Ask About The Fees & Prepayment Conditions

It’s easy to focus only on the loan itself, but the fine print matters just as much. When comparing mortgage lenders with a low credit score in Long Island, you’ll often find that fees and conditions can vary just as much as interest rates.

These can include:

- Origination fees

- Underwriting fees

- Closing costs

- Prepayment penalties (in some cases)

While some of these costs are standard across the industry, others can differ significantly from one lender to another.

This is why transparency is key. Before you apply, ask for a full breakdown of all expected costs and conditions. Understanding the total financial picture, and not just the monthly payment, can help you avoid surprises later on.

A good lender will be upfront about these details and willing to walk you through them. And when you’re comparing options, even small differences in fees or flexibility can have a meaningful impact on your overall experience.

7. Evaluate Flexibility & Underwriting Approach

Finally, not all lenders evaluate borrowers the same way, and this is where things can really start to work in your favor. Some lenders rely strictly on automated systems and rigid criteria, while others take a more complete, human approach to underwriting.

When dealing with mortgage lenders with a low credit score, this difference can be critical. A more flexible lender may look beyond your score and consider factors like employment history, income consistency, recent improvements in credit behavior, or overall financial trajectory.

This is especially important if your credit score doesn’t fully reflect your current situation. For example, if you’ve recently paid down debt, increased your income, or corrected past issues, a more holistic underwriting approach can help bring those improvements into the conversation.

At the end of the day, choosing a lender isn’t just about rates or requirements, it’s about fit. Working with a lender that understands your full financial picture can significantly improve your chances of approval and help you secure terms that actually align with your goals.

Which Are The Best Mortgage Lenders with a Low Credit Score in Long Island?

If you’re asking this question, you’re already thinking the right way, because not all lenders are equipped to work with lower credit profiles.

The truth is, the best mortgage lenders with a low credit score in Long Island aren’t necessarily the biggest names. They’re the ones that offer flexibility, multiple loan options, and a more personalized underwriting approach. You want a lender that looks beyond just your credit score and evaluates your full financial picture.

That’s exactly where Jet Direct Mortgage stands out.

Jet Direct Mortgage is known for working with a wide range of borrowers, including those with less-than-perfect credit. We offer access to FHA loans, low down payment programs, and down payment assistance options, making them a strong choice if your credit score isn’t ideal.

More importantly, our approach focuses on understanding your situation: your income, your stability, and your potential, not just a single number.

Another key advantage is their ability to guide you through the process. Instead of simply approving or denying applications, they help you understand what you qualify for today and what steps you can take to improve your position if needed.

That kind of support can make a real difference when you’re navigating the mortgage process with a lower credit score.

Of course, it’s always smart to compare a few lenders and review your options. But if you’re looking for a lender that combines flexibility, transparency, and a borrower-focused approach, Jet Direct Mortgage is consistently one of the best options to consider.

FAQ

Can I get a mortgage with a low credit score?

Yes, you can get a mortgage with a low credit score. Many mortgage lenders with a low credit score offer flexible options like FHA loans, which may accept scores as low as 500–580 depending on your down payment.

Approval depends on factors like income, debt-to-income ratio, and financial stability, so a lower score doesn’t automatically disqualify you, it just means lenders will evaluate your overall profile more closely.

What is the minimum credit score needed to qualify for a mortgage?

The minimum credit score needed to qualify for a mortgage typically ranges from 500 to 620, depending on the loan type. FHA loans may allow scores as low as 500 with a higher down payment, while most conventional loans require at least 620.

Some mortgage lenders with a low credit score may accept lower scores by considering your overall financial profile.

What loan programs are available for low credit borrowers?

Low credit borrowers can access several mortgage programs, including FHA loans, which may accept scores as low as 500–580, VA loans for eligible military borrowers, and USDA loans for rural areas.

Some mortgage lenders with a low credit score also offer non-QM loans, which use alternative criteria beyond credit scores. The right program depends on your income, down payment, and overall financial profile.

What fees should I expect with a low credit mortgage?

With a low credit mortgage, you can expect fees such as origination fees, closing costs, appraisal fees, and mortgage insurance (PMI or MIP). Some mortgage lenders with a low credit score may also charge higher rates or additional risk-based pricing.

In certain cases, there may be prepayment penalties or underwriting fees, so it’s important to review the full loan estimate carefully before committing.

Can I avoid PMI with a low credit score in Long Island?

Avoiding PMI with a low credit score in Long Island is possible, but it’s more difficult. Most lenders require private mortgage insurance (PMI) if your down payment is below 20%, especially with lower credit.

However, some mortgage lenders with a low credit score may offer alternatives like higher down payments, lender-paid PMI, or piggyback loans. VA loans are one exception, as they don’t require PMI regardless of credit score.

How can I increase my chances of getting approved with bad credit?

To increase your chances of approval with bad credit, focus on improving key factors lenders evaluate. Pay down existing debt to lower your debt-to-income ratio, make all payments on time, and avoid new credit inquiries before applying.

Saving for a larger down payment can also help. Many mortgage lenders with a low credit score will consider your overall financial stability, not just your credit score.

How long does it take to improve my credit score before applying?

Improving your credit score can take 30 to 90 days for small gains, while more significant improvements may take 3 to 6 months or longer, depending on your starting point.

Paying down balances, making on-time payments, and correcting errors can speed up progress. Many mortgage lenders with a low credit score look for recent positive trends, so even short-term improvements can strengthen your application.

Experienced Chief Operating Officer with a 26 + year demonstrated history of working in the banking industry. Skilled in all aspects of the residential mortgage market . Strong business development professional with a Bachelor of Science (BS) focused in Business Administration and Management, from St. Joseph College. A direct endorsement underwriter and a licensed Mortgage Loan Originator.