Nearly half of Veterans (49%) feel homeownership is currently out of reach, according to a recent survey.

But many are closer than they think — and you might be, too.

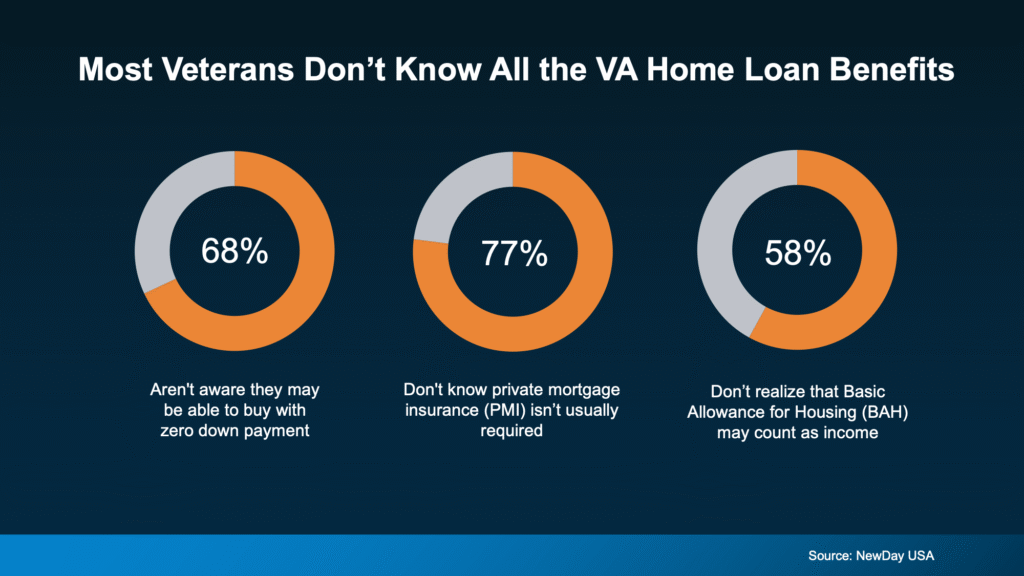

If you’re a Veteran, you probably know the Veterans Affairs (VA) home loan benefit exists. After all, it’s been helping Veterans become homeowners for more than 80 years. What many people don’t realize, though, is how powerful the benefit can actually be. Several common misconceptions continue to hold buyers back from taking the next step toward homeownership.

Any one of those misunderstandings could be keeping you from buying a home sooner than you expected. Let’s break down a few of the biggest myths surrounding VA loans.

You May Not Need a Down Payment

One of the biggest advantages of a VA loan is the potential to purchase a home with zero money down. Yet many buyers still believe they need to save tens of thousands of dollars before they can buy a home.

For many eligible Veterans and service members, that large upfront down payment may not be required at all. That can significantly reduce the time it takes to move from renting to owning.

You Could Pay Less in Closing Costs

According to the Department of Veterans Affairs, VA loans place limits on certain closing costs that buyers may be charged. That means you may have fewer upfront expenses compared to other loan options.

Combined with little to no down payment requirements, lower out-of-pocket costs can make homeownership much more accessible.

You May Not Have Monthly PMI Costs

Unlike many conventional loan programs, VA loans typically do not require private mortgage insurance (PMI), even when purchasing with little or no money down.

With some conventional loans, PMI can add hundreds of dollars to a monthly mortgage payment until enough equity is built in the home. Eliminating that extra expense can lead to meaningful monthly savings over time.

Your BAH & BAS Could Help You Qualify

If you’re active duty military or a qualifying reservist, your Basic Allowance for Housing (BAH) and Basic Allowance for Subsistence (BAS) may be counted as qualifying income when applying for a VA loan.

Because these allowances are generally non-taxable, they may help increase your purchasing power and improve the amount you qualify for.

Bottom Line

VA home loans offer valuable benefits that can help make homeownership more affordable and achievable for those who have served.

At Jet Direct Mortgage, we’re proud to help Veterans, active-duty service members, and military families understand their options and navigate the home loan process with confidence.

If you’re considering buying a home or refinancing, connect with a Jet Direct Mortgage loan professional to learn more about your VA loan opportunities and what you may qualify for.

Source: Keeping Current Matters

Experienced Chief Operating Officer with a 26 + year demonstrated history of working in the banking industry. Skilled in all aspects of the residential mortgage market . Strong business development professional with a Bachelor of Science (BS) focused in Business Administration and Management, from St. Joseph College. A direct endorsement underwriter and a licensed Mortgage Loan Originator.