Mortgage rates remain one of the hottest topics in real estate—and for good reason. Earlier this month, after a weaker-than-expected jobs report, the bond market reacted quickly. The result? Mortgage rates dipped to 6.55%—their lowest level so far this year.

At first glance, that drop might not seem dramatic. But for many buyers who’ve been waiting on the sidelines, even a small dip feels like a spark of hope that rates could be on their way down. So, what’s realistic to expect from here?

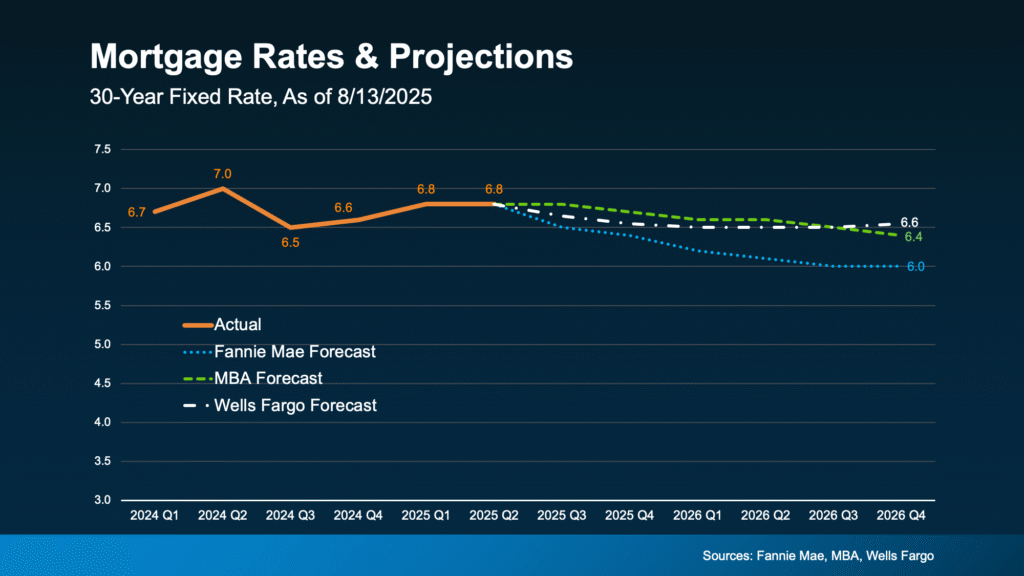

The Outlook for Rates

Current forecasts suggest mortgage rates aren’t headed for a big plunge anytime soon. Most experts expect them to hover in the mid-to-low 6% range through 2026. That means small ups and downs—like the recent drop—are still likely, especially as new economic data is released. With several key reports coming out this week, we’ll soon have a better sense of where inflation, the economy, and rates are headed.

The “Magic Number” for Buyers

For many buyers, the number to watch is 6%. And it’s not just psychological—it’s practical. According to the National Association of Realtors (NAR), if rates hit 6%:

- 5.5 million more households could afford the median-priced home.

- About 550,000 more people would likely buy a home within 12–18 months.

That’s a lot of pent-up demand. In fact, Fannie Mae predicts we may reach that level next year. But here’s the catch—when rates drop and more buyers jump in, competition heats up, inventory shrinks, and prices can rise.

The Tradeoff of Waiting

If you’re waiting for 6%, remember: thousands of others are too. When that happens, you could be competing in a busier market with fewer choices and less room to negotiate.

Right now, conditions are a little different:

- More inventory means more options.

- Slower price growth means more realistic pricing.

- Better negotiating room could mean getting a deal you can’t later.

As NAR puts it:

“Buyers who are holding out for lower mortgage rates may be missing a key opening in the market.”

Bottom Line

Rates may not hit 6% this year—and when they do, the market could be a lot more competitive. If you want less pressure, more options, and stronger negotiating power, that window may be open now, but it won’t stay that way forever.

Let’s connect to talk about what’s happening locally and whether it makes sense to make your move before everyone else does.

Source: Keeping Current Matters

Megan Ringhoff is a licensed loan officer at Jet Direct Mortgage who prides herself in helping people change their lives for the better, helping them build wealth, and putting people and their families into a home with a backyard to call their own. Megan strives to find ways for her clients to get the best possible deal to fit their situation and will do anything to make their dreams come to reality. NMLS#2040719