If you’ve been asking yourself, “Can I buy a house with a 600 credit score?”, you’re not alone. It’s one of the most common questions among buyers who feel like their credit might be holding them back.

For years, there has been a strong belief that you need excellent credit to buy a home. In reality, that’s not how today’s mortgage market works. In 2026, there are multiple loan programs specifically designed for borrowers who fall into the “average” or even “below-average” credit range.

That includes people with a 600 credit score.

So, can you buy a house with a 600 credit score? The answer is yes. But like most things in lending, it depends on more than just the number itself. Lenders are not just evaluating your score.

They are evaluating your behavior, your consistency, and your ability to manage a mortgage long term. If you understand what they’re looking for, you can move from “maybe” to “approved” much faster than you think.

Our team at Jet Direct Mortgage has prepared this in-depth guide to help you better understand everything you need to do in order to buy a house with a 600 credit score. So, let’s get right into it:

Can You Really Buy a House with a 600 Credit Score in New York?

Yes, you can buy a house with a 600 credit score in New York, but approval is not automatic. The credit score gets your foot in the door.

Everything else determines whether you walk through it.

Lenders want to understand risk. A 600 credit score signals that there may have been past issues, such as missed payments, high balances, or financial instability at some point. But what matters more is whether those issues are recent or improving.

For example, if you have a 600 credit score, but you have made all payments on time for the past 12 to 24 months, you might be viewed much more favorably than someone with the same score but recent delinquencies. This is because lenders prioritize recent behavior as a predictor of future performance.

When you apply, they will look at your full financial profile. This includes your income, your employment stability, your existing debts, and how consistently you’ve handled your obligations over time.

So, while a 600 credit score may not be ideal, it is absolutely within a range where buying a home is possible, especially if the rest of your profile is solid.

What Credit Score Do You Need to Buy a House in New York?

One of the biggest myths in home buying is that you need a high credit score to get approved. While a higher score can help you secure better interest rates, it’s not always required to qualify.

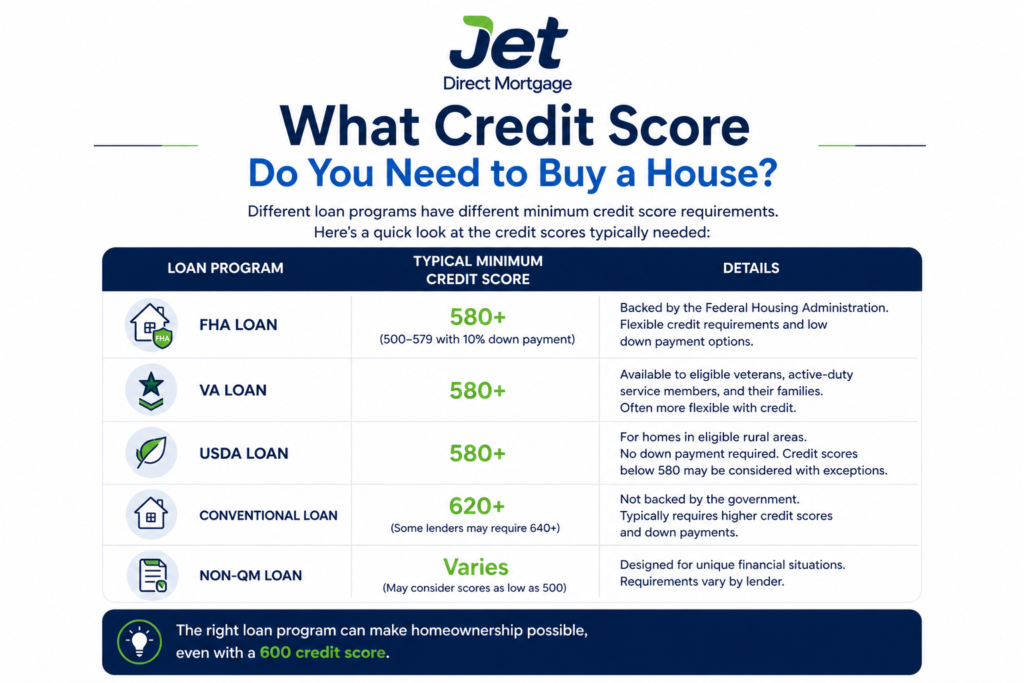

Different loan programs have different minimum requirements. FHA loans, for example, are known for their flexibility and typically allow borrowers with scores starting around 580. Some lenders may even consider lower scores with additional conditions.

This means that if your goal is to buy a house with a 600 credit score, you’re already within the acceptable range for some of the most accessible loan options available.

Conventional loans, on the other hand, usually require a score of 620 or higher, making them less suitable for borrowers in this range. That’s why choosing the right loan program becomes so important.

Which Are The Best Loan Options to Buy a House With a 600 Credit Score in New York?

If you’re planning to buy a house with a 600 credit score in New York, choosing the right loan program is one of the most important decisions you’ll make. Not all mortgages are designed for lower credit profiles, and applying for the wrong one can lead to unnecessary rejections or delays.

Below are the most common loan options and how they compare.

FHA Loans

FHA loans are typically the most popular choice for borrowers looking to buy a house with a 600 credit score. These loans are backed by the Federal Housing Administration and are specifically designed for buyers who may not meet conventional lending standards.

Key benefits:

- Lower credit score requirements (starting around 580)

- Lower down payments

- More flexible approval criteria

- Higher tolerance for past credit issues

In most cases, FHA loans offer the highest approval chances for buyers in this credit range.

VA Loans

For eligible borrowers, VA loans can be even more advantageous than FHA loans. These are available to veterans, active-duty service members, and certain military families.

Key benefits:

- No down payment required

- Competitive interest rates

- No private mortgage insurance (PMI)

- Flexible credit guidelines

Many lenders accept scores around 600, making this a strong option if you qualify.

Conventional Loans

Conventional loans are not backed by the government, which means lenders take on more risk, and therefore apply stricter requirements. For you, this means that buying a house with a 600 credit score with a conventional loan isn’t impossible, but it’s harder.

What to expect:

- Typical minimum score: 620+

- Stricter debt-to-income requirements

- Higher interest rates for lower scores

- Stronger financial profile needed

While not impossible, conventional loans are usually harder to qualify for if your goal is to buy a house with a 600 credit score.

Non-QM Loans

Non-qualified mortgage (Non-QM) loans are designed for borrowers who don’t fit traditional lending criteria, such as self-employed individuals or those with non-standard income.

Key features:

- Flexible income verification (bank statements, etc.)

- No strict credit score rules

- Alternative approval methods

Trade-offs:

- Higher interest rates

- Larger down payments often required

- Less standardized guidelines

These loans can work as a backup option, but they are usually more expensive. So, while you can still buy a house with a 600 credit score with them, you need to consider the trade-offs.

Step-by-Step: How to Buy a House With a 600 Credit Score in Long Island & New York

If you’re planning to buy a house with a 600 credit score, following a clear step-by-step process can make everything feel more manageable. While the overall journey is similar to any mortgage, preparation is especially important at this credit level.

Step 1: Review Your Credit Report

Start by checking your credit report in detail, you can do it in credit bureaus such as Experian or Equifax.

Look for errors, outdated accounts, or negative items that could be improved. Even small corrections can increase your chances of approval and help you qualify for better terms.

Step 2: Strengthen Your Financial Profile

Before applying, take time to improve the key factors lenders care about. Focus on lowering your credit card balances, making all payments on time, and avoiding new debt. These changes can quickly make your application stronger, even within a few weeks.

Step 3: Get Pre-Approved

Once you’re in a better position, apply for pre-approval with a lender such as Jet Direct Mortgage. This step helps you understand exactly how much you can afford and shows sellers that you’re a serious buyer.

It also allows lenders to flag any potential issues early in the process.

Step 4: Choose the Right Loan Program

Work with your lender to select the best loan option for your situation. For most buyers looking to buy a house with a 600 credit score, FHA loans are the most common and accessible choice.

Step 5: Start Your Home Search

With pre-approval in hand, begin searching for homes within your budget. Keep in mind that certain loan types, like FHA loans, require the property to meet specific safety and livability standards.

Step 6: Make an Offer and Begin Underwriting

After finding the right home, you’ll submit an offer. Once accepted, your loan enters underwriting, where the lender verifies your financial information and reviews the property details.

Step 7: Complete the Appraisal and Final Approval

The lender will order an appraisal to confirm the home’s value and condition. If everything checks out, you’ll move toward final approval and closing.

Step 8: Close on Your Home

At closing, you’ll sign the final documents, pay any required costs, and officially become a homeowner! Congratulations – you have proved that you can buy a house with a 600 credit score.

Why You Should Buy a House With a 600 Credit Score in New York With Jet Direct Mortgage

Buying a home with a lower credit score in New Yorkcan feel uncertain, but the right lender makes all the difference. If your goal is to buy a house with a 600 credit score, working with a team that understands your situation, and knows how to navigate it, is key.

At Jet Direct Mortgage, the focus isn’t just on your credit score. It’s on your full financial picture. That means looking beyond the number and helping you build a strong, approvable application based on your income, payment history, and overall stability.

What sets them apart is their experience with borrowers who don’t fit the “perfect credit” mold. Instead of taking a one-size-fits-all approach, they guide you step by step; whether that means helping you choose the right loan program, identifying ways to improve your approval odds, or getting you pre-approved faster.

If you’re ready to buy a house with a 600 credit score, having the right support can turn a complicated process into a clear path forward. With the right guidance, what once felt out of reach becomes a realistic next step.

Ready to apply for a 600 credit score home loan? Let’s get you started.

FAQ

Is 600 a good enough credit score to buy a house in Long Island?

Yes, a 600 credit score is generally good enough to buy a house in Long Island, especially through FHA loans. While it’s not considered a strong score, it falls within the acceptable range for many lenders.

Approval depends on your full financial profile, including income, debt-to-income ratio, and recent payment history. With stable finances, buying a home at this level is realistic.

How hard is it to buy a house with a 600 credit score in Long Island?

Buying a house with a 600 credit score in Long Island is moderately challenging but far from impossible. FHA loans make the process more accessible, but lenders will still review your income, debt, and payment history closely.

If you have consistent on-time payments and manageable debt, the process becomes significantly easier and your chances of approval improve.

How much house can I afford with a 600 credit score?

How much house you can afford with a 600 credit score depends mainly on your income and debt, not just your score. Most lenders use a debt-to-income ratio of around 43% to determine your budget.

In many cases, borrowers can qualify for homes between $150,000 and $300,000, depending on income, expenses, and current interest rates.

Can I get denied when trying to buy a house with a 600 credit score?

Yes, you can be denied when trying to buy a house with a 600 credit score if other factors don’t meet lender requirements. Common reasons include high debt-to-income ratio, recent late payments, unstable income, or insufficient documentation.

Even though some loan programs are flexible, lenders still evaluate your overall financial stability before approving a mortgage.

How can I improve my chances to buy a house with a 600 credit score?

You can improve your chances to buy a house with a 600 credit score by lowering your debt, making all payments on time, and avoiding new credit before applying.

Reducing credit card balances below 30% utilization and maintaining stable income can strengthen your application. Even small improvements can make a noticeable difference in approval odds.

How long does it take to buy a house with a 600 credit score?

Buying a house with a 600 credit score typically takes between 30 and 60 days once you’re under contract. Pre-approval can take a few days, while the full process includes underwriting, appraisal, and final approval.

The timeline depends on how quickly you provide documents and whether any issues arise with your finances or the property.

Experienced Chief Operating Officer with a 26 + year demonstrated history of working in the banking industry. Skilled in all aspects of the residential mortgage market . Strong business development professional with a Bachelor of Science (BS) focused in Business Administration and Management, from St. Joseph College. A direct endorsement underwriter and a licensed Mortgage Loan Originator.