A Clear Path to Lower Payments and Faster Refinancing for Veterans

For Florida veterans, service members, and qualified surviving spouses, the VA Interest Rate Reduction Refinance Loan (IRRRL) offers one of the most efficient and impactful ways to improve the terms of an existing VA mortgage. In a state characterized by rising insurance premiums, shifting market conditions, and fluctuating interest environments, the IRRRL remains a uniquely powerful tool for achieving stability. The program is designed specifically for borrowers already using a VA-backed mortgage who want streamlined access to better affordability, faster timelines, and reduced monthly obligations.

The Florida housing market presents a combination of opportunities and challenges: coastal insurance requirements, rapidly growing home values in several counties, and interest-rate cycles that affect long-term planning. The VA IRRRL mortgage program helps existing VA borrowers navigate these dynamics by offering a simplified refinance path built to reduce monthly payments, secure more favorable terms, or transition from unpredictable adjustable-rate mortgages into fixed-rate stability.

Why Florida Borrowers Choose the VA IRRRL Program

Many Florida homeowners consider the VA IRRRL refinance program when interest rates shift or financial needs evolve. The program emphasizes simplicity, allowing borrowers to move forward with ease when seeking a VA rate reduction refinance or a transition from adjustable-rate terms to fixed stability.

Key drivers for Florida borrowers include:

- The opportunity to refinance a VA loan with a lower rate

- Ability to reduce VA mortgage payment obligations

- Streamlined underwriting and minimal documentation

- Options to switch from adjustable to fixed VA loan for long-term stability

- Faster approvals and closings, supporting those seeking fast VA refinance approval

The IRRRL is often the best choice for borrowers focused on lowering monthly mortgage costs or simplifying their future financial outlook.

Understanding the Florida VA IRRRL Program

What Is a VA Streamline Refinance?

A VA Streamline Refinance, formally known as the Interest Rate Reduction Refinance Loan (IRRRL), is a refinancing option exclusively for borrowers with an existing VA mortgage. Its purpose is to provide clear financial benefit, typically through lower interest rates, reduced monthly payments, or improved loan terms.

The program provides:

- A simplified refinance path

- The potential to lower my VA loan interest when market rates move favorably

- A reliable option for converting variable-rate mortgages into predictable fixed-rate loans

- Access to refinancing without extensive documentation, income verification, or appraisal

The IRRRL remains one of the few refinance programs that consistently balances accessibility, speed, and measurable financial impact.

Top Benefits of the Florida VA IRRRL

1. Lower Interest Rates and Monthly Payments

Borrowers can often lower VA mortgage interest through the IRRRL, helping reduce overall monthly housing expenses. When combined with insurance and tax obligations common in Florida, even modest reductions in rate may create meaningful long-term savings.

2. No Appraisal Needed in Most Situations

The no-appraisal VA refinance loan feature is a major benefit for Florida borrowers navigating unpredictable property valuations, especially in coastal regions. Borrowers can move forward without worrying about home-value fluctuations impacting eligibility.

3. Streamlined Documentation Requirements

Because the program is designed as a refinance of an existing VA loan, most borrowers enjoy:

- No income verification

- No employment documentation

- Minimal credit review

This significantly shortens the VA IRRRL refinance timeline, often making the process more efficient than other refinance programs.

4. Conversion from ARM to Fixed Rates

Borrowers with adjusting mortgages often want predictable monthly payments. The IRRRL supports:

- Converting an ARM to a fixed-rate structure

- Long-term payment stability

- Protection from future rate increases

5. Low or Rolled-In Closing Costs

With VA guidelines allowing many VA refinance closing costs to be rolled into the new loan amount, borrowers can often complete the refinance without upfront spending.

Florida VA IRRRL Eligibility Requirements

The IRRRL program includes clear, veteran-focused eligibility standards.

Basic Requirements

- The borrower must currently have a VA-backed loan.

- The new refinance must demonstrate a financial benefit such as a lower rate or improved stability.

- The borrower must currently live in—or have previously lived in—the home being refinanced.

Key Restrictions

- Cash-out is not permitted.

- Energy-efficient improvements are capped at $6,000.

- The new interest rate must typically be lower unless converting from an ARM to a fixed loan.

Florida-Specific Considerations

Florida borrowers must account for:

- Higher homeowner insurance premiums

- Potential flood-zone requirements

- Regional variations in property taxes

These variables influence how much monthly savings a veteran may achieve.

VA IRRRL Refinance Process for Florida Borrowers

Step-by-Step Overview of the VA IRRRL Loan Steps Explained

The IRRRL uses a streamlined structure to avoid unnecessary steps.

Step 1: Get a VA Loan Refinance Quote

Borrowers begin by requesting a personalized quote that aligns with current market rates and desired financial benefits.

Step 2: Confirm Eligibility and Financial Improvement

A lender ensures the refinance meets VA requirements, including the Net Tangible Benefit test.

Step 3: Submit Limited Documentation

Documentation may include identification, mortgage statements, and verification of prior occupancy.

This process avoids burdensome requirements typical of traditional refinancing.

Step 4: Review Disclosures and Lock Terms

Borrowers receive disclosures detailing interest rate, APR, and estimated payments, alongside required compliance notices.

Step 5: Close and Finalize the Refinance

Borrowers sign the new loan documents, and the updated VA-backed loan replaces the prior mortgage.

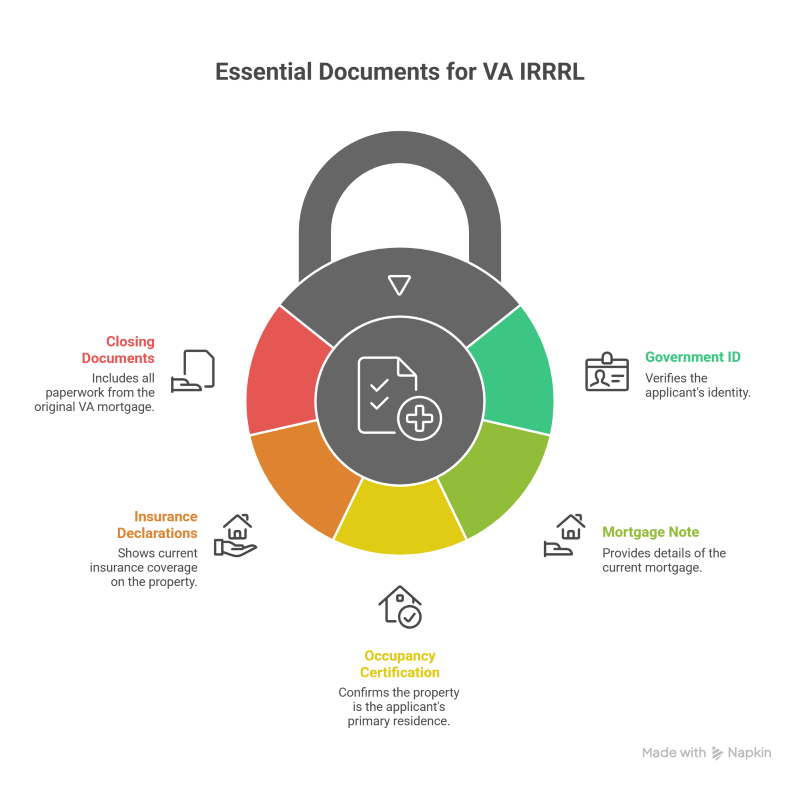

Documents Needed for VA IRRRL

Most borrowers complete the refinance with only a few items:

- Government-issued identification

- Current mortgage note or statement

- Occupancy certification

- Insurance declarations

- Closing documents from the original VA mortgage

Lenders often retrieve Certificates of Eligibility automatically through VA systems.

VA IRRRL Guidelines: What Florida Borrowers Should Know

The VA IRRRL refinance guidelines 2025 place emphasis on consumer protection and long-term benefit.

1. Net Tangible Benefit Requirement

The refinance must produce a measurable improvement such as a lower rate, reduced payment, or more stable loan structure.

2. 36-Month Recoupment Rule

If closing costs are rolled into the new loan, they must be recouped through monthly savings within 36 months.

3. Seasoning Requirement

Borrowers must wait at least 210 days from the first payment on the original VA loan.

4. ARM-to-Fixed Conversions Allowed

Borrowers transitioning to a fixed rate do not need to show rate reduction.

Florida IRRRL Feature Summary

VA IRRRL at a Glance

| Feature | Description | Benefit to Florida Borrowers | Typical Requirement |

| Rate Reduction | Lower fixed or ARM interest rates | Helps lower VA mortgage interest and reduce payments | Must meet NTB standard |

| No Appraisal | Often not required | Faster approval during high-value fluctuations | Property must meet VA criteria |

| Low Documentation | No income or employment verification in most cases | Speeds up approval and underwriting | Existing VA loan required |

| Payment Stability | Option to convert ARM to fixed | Protects against Florida market volatility | ARM-to-fixed conversions allowed |

Fixed vs. Adjustable VA IRRRL Options

Comparison Table

| Loan Type | Best For | Pros | Potential Considerations |

| Fixed-Rate IRRRL | Long-term homeowners | Predictable payments | May start at slightly higher rate |

| ARM IRRRL | Short-term homeowners | Lower introductory rates | Future rate adjustments possible |

| ARM-to-Fixed Conversion | Borrowers seeking stability | Locks in consistent payments | Rate may increase slightly |

| Low-Rate IRRRL | Qualified veterans | Immediate payment relief | Rates subject to market change |

How to Refinance a VA Loan in Florida

Borrowers typically follow this sequence when determining how to refinance a VA loan through the IRRRL program:

- Establish goals such as lowering rate, reducing payment, or switching rate types.

- Contact a VA-approved lender to start VA refinance application steps.

- Review personalized quotes and disclosures.

- Evaluate APR, payment structure, and long-term benefits.

- Complete minimal documentation and sign closing documents.

This simplified approach appeals to borrowers seeking VA refinance options without the complexity of traditional refinancing.

Why the IRRRL Is Especially Valuable in Florida

Florida’s market creates unique conditions where the IRRRL is particularly impactful:

- Insurance volatility makes payment reductions highly valuable.

- Rapid property-value swings increase the benefit of a no-appraisal VA refinance loan.

- Borrowers with adjusting-rate VA loans often seek fixed-rate stability to protect future budgets.

These factors make the IRRRL an effective solution for navigating Florida’s financial landscape.

Key Insights for Florida VA IRRRL Borrowers

- The IRRRL represents one of the most streamlined ways to refinance an existing VA mortgage.

- Benefits include faster processing, reduced documentation, and no appraisal requirement in most situations.

- Florida borrowers can experience significant value through lower payments, improved loan structure, or conversion to a fixed rate.

- Interest rate, APR, and payment disclosures must be presented with full transparency and remain subject to change without notice.

- Jet Direct Mortgage supports borrowers through every stage of the VA IRRRL refinance process, providing clarity, expertise, and consistent communication tailored to Florida’s market conditions.

Start Your Florida VA IRRRL Refinance With Jet Direct Mortgage

Jet Direct Mortgage helps Florida veterans secure lower payments, stronger terms, and dependable refinancing through the VA IRRRL program. With a focus on education, support, and clear communication, borrowers can navigate the refinance process with confidence.

Jet Direct Mortgage

4875 Sunrise Hwy, Suite 300, Bohemia, New York 11716

Call: +1.800.700.4JET

Email: express@jetdirectmortgage.com

Explore additional home loan options here:

https://jetdirectmortgage.com/home-loan-programs/

FAQ’s

What is a VA IRRRL and how does it help Florida homeowners?

The VA IRRRL is a streamlined refinancing option for borrowers with existing VA loans who want a lower interest rate, reduced monthly payment, or a fixed-rate mortgage. Florida homeowners benefit from simplified documentation, no appraisal in most cases, and faster processing. This program helps borrowers secure long-term affordability while avoiding the extensive underwriting requirements of traditional refinancing.

Do I need an appraisal for a Florida VA IRRRL refinance?

Most Florida borrowers completing an IRRRL do not need an appraisal. Because the refinance is based primarily on eligibility tied to the original VA loan, current property value typically does not affect qualification. This is especially helpful in Florida markets experiencing fluctuating home values. Borrowers benefit from a faster, more predictable refinance timeline.

Can I refinance a VA loan in Florida without income verification?

Yes. The IRRRL program generally does not require borrowers to provide income or employment documentation, as eligibility is tied to the performance of the existing VA loan. This streamlined approach is especially useful for Florida homeowners with complex income structures, variable self-employment earnings, or recent transitions in their employment or financial profile.

How long does the VA IRRRL refinance timeline take?

The IRRRL typically closes more quickly than traditional refinancing options. Many Florida borrowers experience timelines ranging from a couple of weeks to slightly longer depending on documentation and lender volume. The streamlined structure helps borrowers secure improved terms without prolonged review or multi-layer underwriting, making it one of the fastest refinance options available.

What costs are included in a Florida VA IRRRL refinance?

Borrowers may include lender fees, title charges, and other standard closing costs in their refinance. Many Florida borrowers choose loan-rollover options to avoid out-of-pocket expenses. VA rules require these costs to be recouped through monthly savings within 36 months, ensuring that the refinance remains financially beneficial.

Who qualifies for a VA Streamline Refinance in Florida?

Qualification requires an existing VA-backed mortgage, proof of prior occupancy, and a measurable financial benefit such as reduced interest or increased payment stability. Borrowers must also meet VA seasoning guidelines, including a 210-day period after first loan payment. The IRRRL offers an accessible refinance option for Florida veterans seeking improved loan terms with minimal documentation.

Licensing & Compliance Disclosure

Jet Direct Mortgage – NMLS: 3542

Jet Direct Mortgage © 2025. All Rights Reserved. Alabama Consumer Credit License – License/Registration #22632; Arizona Mortgage Banker License – Lic/Reg#:1040763; Licensed by the Department of Financial Protection and Innovation under the California Residential Mortgage Lending Act – #41DBO-81230; Colorado Mortgage Company Registration #LMB100014791; Connecticut Mortgage Lender License #20333; Delaware Lender License – License/Registration #032943; Florida Mortgage Lender Servicer License #MLD357; Licensed by the Georgia Department of Banking and Finance Company License – License #64345; Illinois Residential Mortgage License – Lic/Reg#:MB.6850070; Indiana DFI Mortgage Lending License No. 59981; Maine Supervised Lender License No. SLM9525; Maryland Mortgage Lender License #17365; MA Mortgage Lender License #ML3542; Michigan 1st Mortgage Broker/Lender/Servicer Registrant #FL10015703; Licensed Residential Mortgage Lender NJ Dept of Banking & Insurance #3542; New Mexico Mortgage Loan Company License 3542; Licensed Mortgage Banker NYS Department of Financial Services #B500903 – NMLS#3542; North Carolina Mortgage Lender License L-180193; Ohio Mortgage Broker Act Mortgage Banker Exemption # MBMB.850088.000; Oregon: State of Oregon ML-3542; Pennsylvania Mortgage Lender License No. 47421; South Carolina-BFI Mortgage Lender / Servicer License MLS–3542; Tennessee Mortgage License – License/Registration #17365; Texas – SML Mortgage Banker Registration; Virginia License/Registration # MC-4985; Washington Department of Financial Institutions, Consumer Loan Company License CL-3542; Wisconsin – Mortgage Banker License, #ML3542.

Experienced Chief Operating Officer with a 26 + year demonstrated history of working in the banking industry. Skilled in all aspects of the residential mortgage market . Strong business development professional with a Bachelor of Science (BS) focused in Business Administration and Management, from St. Joseph College. A direct endorsement underwriter and a licensed Mortgage Loan Originator.