The Complete Homeowner Guide

Refinancing a mortgage in Suffolk County is not just about replacing one loan with another. It is a financial strategy that can reshape your monthly obligations, improve long-term stability, remove mortgage insurance, or unlock home equity built through years of ownership in one of New York’s most competitive housing markets.

From Bohemia to Huntington, Patchogue to Smithtown, Suffolk homeowners operate in a real estate environment defined by strong property values, significant property taxes, coastal considerations, and attorney-driven closings. Understanding how to refinance a mortgage in Suffolk means understanding both the financial mechanics and the local nuances that affect approval, timing, and overall cost.

What Refinancing a Mortgage Actually Means

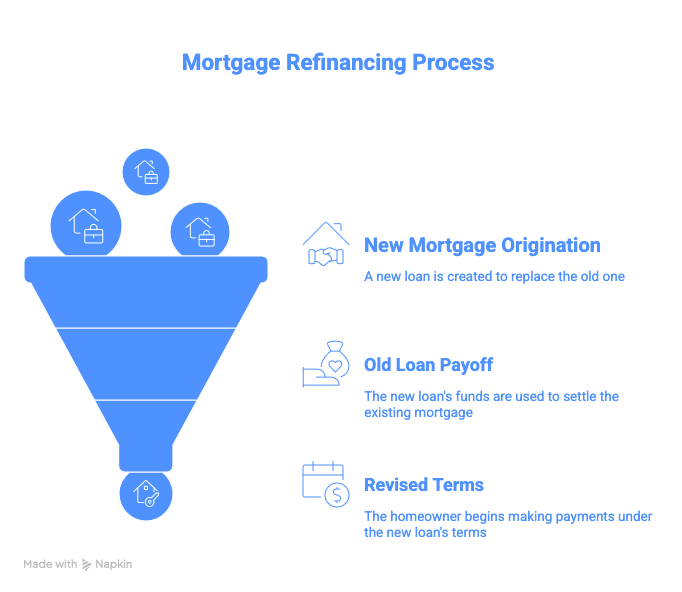

Refinancing replaces your existing home loan with a new mortgage. The new loan pays off the current one, and you begin repayment under revised terms.

Homeowners in Suffolk typically refinance to:

- Lower their monthly mortgage payment

- Transition from an adjustable-rate loan to a fixed structure

- Shorten the loan term

- Remove mortgage insurance

- Access home equity

- Consolidate debt into one manageable payment

Unlike purchasing a home, refinancing does not involve changing ownership. The property remains yours — only the financing structure changes.

Why Suffolk County Homeowners Refinance

1. Improve Monthly Cash Flow

In a region where property taxes and living expenses are higher than the national average, even modest monthly savings can provide breathing room. Restructuring your mortgage may reduce the principal and interest portion of your payment, creating more predictable housing costs.

2. Remove Mortgage Insurance

Many Suffolk homeowners initially purchase with less than 20% down. Government-backed loans, particularly Federal Housing Administration (FHA) loans, may carry mortgage insurance for the life of the loan depending on initial terms.

Refinancing into a conventional mortgage after building sufficient equity may eliminate that ongoing insurance cost.

Official FHA program information is available through the U.S. Department of Housing and Urban Development:

https://www.hud.gov/program_offices/housing/sfh

3. Access Home Equity in a Strong Market

Suffolk County property values have appreciated steadily over time. If your home’s value has increased, you may have accumulated significant equity. A cash-out refinance allows homeowners to convert a portion of that equity into funds for:

- Home renovations

- College tuition

- Business expansion

- Debt restructuring

- Major life events

Equity is calculated as:

Current Home Value – Outstanding Mortgage Balance = Equity

4. Shorten the Loan Term

Some homeowners refinance from a 30-year mortgage into a 15- or 20-year term to accelerate payoff and reduce total long-term borrowing costs.

Understanding Refinance Options Available in Suffolk

Rate-and-Term Refinance

This is the most common refinance option. It changes the loan structure — such as term length or loan type — without taking cash out.

Best suited for:

- Lowering monthly payment

- Transitioning from adjustable to fixed

- Removing mortgage insurance

- Adjusting repayment timeline

Cash-Out Refinance

A cash-out refinance replaces your current mortgage with a larger loan. The difference between the old balance and the new loan amount is provided to you at closing.

| Estimated Home Value | Current Loan Balance | Estimated Equity | Possible Cash-Out (Subject to LTV Limits) |

|---|---|---|---|

| $750,000 | $450,000 | $300,000 | Portion of equity, based on guidelines |

Lenders typically require you to retain a certain percentage of equity after refinancing.

FHA Streamline Refinance

If you currently have an FHA loan, you may qualify for a streamlined refinance option with reduced documentation requirements.

Official FHA guidance is available from HUD:

https://www.hud.gov/program_offices/housing/sfh/fharesourcectr

VA Interest Rate Reduction Refinance Loan (IRRRL)

Eligible veterans and service members in Suffolk County may refinance using the VA streamline program, designed to reduce monthly obligations with simplified documentation.

Official VA information:

https://www.va.gov/housing-assistance/home-loans/

Conventional Refinance

Conventional loans often provide flexibility for borrowers with strong credit and sufficient equity. These loans typically allow removal of private mortgage insurance once equity thresholds are met.

Step-by-Step: How to Refinance a Mortgage in Suffolk County

Refinancing in New York involves multiple parties and legal considerations. Here’s how the process typically unfolds.

Step 1: Define Your Objective

Before submitting an application, clarify your purpose:

- Are you reducing monthly payments?

- Accessing equity?

- Removing mortgage insurance?

- Shortening your loan term?

Your goal determines loan structure.

Step 2: Review Your Equity Position

Most conventional refinance programs perform best when homeowners have at least 20% equity. However, certain government-backed programs may allow lower equity levels.

A professional appraisal will confirm current value.

Step 3: Submit Application and Documentation

You will typically provide:

- Income documentation (W-2s or tax returns)

- Pay stubs

- Bank statements

- Current mortgage statement

- Homeowners insurance information

Self-employed borrowers in Suffolk may need to provide additional documentation.

Step 4: Appraisal and Underwriting

An independent appraisal determines market value. Underwriting evaluates:

- Income stability

- Employment history

- Debt-to-income ratio

- Credit profile

- Property eligibility

In Suffolk County, attorney involvement is standard at closing.

Step 5: Closing and Right of Rescission

After signing documents, primary residence refinances typically include a three-day rescission period before funds are disbursed.

Suffolk-Specific Refinance Considerations

Property Taxes

Suffolk County property taxes are among the highest in New York State. While refinancing does not directly reduce property taxes, restructuring your mortgage can offset overall housing expenses.

Flood Zones and Coastal Regulations

Communities near the South Shore, North Shore, and Hamptons may require flood insurance verification during refinancing.

FEMA flood map information:

https://msc.fema.gov/

Co-Ops and Condos

Some Suffolk co-op boards require additional approvals during refinancing. Documentation may include:

- Board financial review

- Shareholder approval

- Building financial statements

How Long Does It Take to Refinance in Suffolk?

Refinancing timelines vary, but most Suffolk County transactions close within 30 to 45 days.

| Phase | Estimated Timeframe |

| Application | 1–3 days |

| Appraisal | 1–2 weeks |

| Underwriting | 2–3 weeks |

| Closing | 30–45 days total |

Attorney scheduling can influence timing.

Costs Associated with Refinancing

Refinancing a mortgage involves several closing costs that are similar to those encountered when purchasing a home. These expenses may include:

- Appraisal fee

- Title insurance

- Attorney fees

- Recording fees

- Lender-related fees

The total cost of refinancing can vary depending on the loan structure, property details, and the specific services required to complete the transaction.

To evaluate whether refinancing is financially worthwhile, many homeowners calculate a break-even point.

Total Closing Costs ÷ Monthly Savings = Months to Break Even

If you plan to remain in your home longer than the break-even period, refinancing may provide meaningful long-term financial benefit.

Refinance vs. Home Equity Loan

Some homeowners consider a home equity loan instead of refinancing.

| Feature | Refinance | Home Equity Loan |

| Replaces existing mortgage | Yes | No |

| Accesses equity | Yes | Yes |

| Single monthly payment | Yes | No |

| Keeps current mortgage intact | No | Yes |

Refinancing restructures the entire loan, while a home equity loan creates a second lien.

When Refinancing Makes Strategic Sense

Refinancing is often beneficial when:

- You’ve built substantial equity

- Mortgage insurance can be removed

- You want predictable, stable payments

- You plan to remain in the property long enough to recover closing costs

- You are consolidating higher-interest debt

FAQ’s

1. How do I refinance a mortgage in Suffolk County, New York?

To refinance a mortgage in Suffolk County, you apply with a licensed lender, submit income and asset documentation, complete a property appraisal, and go through underwriting approval. After final approval, you close with a real estate attorney, and once the rescission period ends, your new mortgage replaces the old one.

2. How long does it take to refinance a home in Suffolk County?

Most mortgage refinances in Suffolk County close within 30 to 45 days. The timeline depends on appraisal scheduling, document submission speed, underwriting conditions, and attorney availability. Complex properties such as co-ops or multi-family homes may take slightly longer.

3. How much equity do I need to refinance in Suffolk?

Many conventional refinance programs perform best when homeowners have at least 20 percent equity. However, certain government-backed refinance programs may allow lower equity levels depending on borrower qualifications and loan structure.

4. Can I refinance my Suffolk home to remove mortgage insurance?

Yes, refinancing may eliminate mortgage insurance if you qualify for a conventional loan and have built sufficient equity. Once you meet the required loan-to-value threshold, the new mortgage can be structured without ongoing mortgage insurance.

5. Do I need a new appraisal to refinance in Suffolk County?

In most refinance transactions, a new appraisal is required to confirm the home’s current market value. However, certain streamlined government programs may allow an appraisal waiver depending on eligibility guidelines.

6. Is refinancing worth it if I plan to sell my Suffolk home soon?

Refinancing typically makes sense if you plan to stay in the home long enough to recover closing costs. Calculating your break-even point helps determine whether the monthly savings justify refinancing before selling.

7. Can I refinance a mortgage in Suffolk if I am self-employed?

Yes, self-employed borrowers can refinance in Suffolk County, but lenders typically require additional documentation such as two years of tax returns, profit and loss statements, and proof of consistent income stability.

8. What are the typical closing costs to refinance in Suffolk County?

Refinance closing costs in Suffolk County often range between 2 percent and 5 percent of the loan amount. Costs may include appraisal fees, title services, attorney fees, recording charges, and lender-related expenses.

9. Can I refinance and take cash out of my Suffolk home?

Yes, a cash-out refinance allows you to access a portion of your home’s equity and receive funds at closing. Lenders require you to maintain a minimum equity percentage after the transaction is complete.

10. Will refinancing affect my property taxes in Suffolk County?

Refinancing does not directly change your property tax assessment. Property taxes are determined by your local municipality, but adjusting your mortgage structure may help manage overall housing expenses more efficiently.

Key Takeaways for Suffolk Homeowners

- Refinancing replaces your existing mortgage with new terms.

- It may reduce monthly payments or eliminate mortgage insurance.

- Suffolk’s property values can improve eligibility.

- Closing costs must be weighed against long-term savings.

- Coastal and co-op properties may require additional documentation.

Work With a Local Suffolk Mortgage Professional

Refinancing involves financial, legal, and property-specific factors. Working with a Long Island-based lender ensures familiarity with Suffolk County attorney closings, appraisal expectations, and regional housing trends.

Jet Direct Mortgage provides refinance solutions tailored to Suffolk homeowners.

Contact Jet Direct Mortgage

Website: https://www.jetdirectmortgage.com

Phone: +1.800.700.4JET

Email: express@jetdirectmortgage.com

Address: 4875 Sunrise Hwy, Suite 300, Bohemia, New York 11716

Explore additional home loan programs:

https://jetdirectmortgage.com/home-loan-programs/

Licensing and Compliance

Jet Direct Mortgage © 2025. All Rights Reserved.

Alabama Consumer Credit License – License/Registration #22632; Arizona Mortgage Banker License – Lic/Reg#:1040763; Licensed by the Department of Financial Protection and Innovation under the California Residential Mortgage Lending Act – #41DBO-81230; Colorado Mortgage Company Registration #LMB100014791; Connecticut Mortgage Lender License #20333; Delaware Lender License – License/Registration #032943; Florida Mortgage Lender Servicer License #MLD357; Licensed by the Georgia Department of Banking and Finance Company License Company – License #64345; Illinois Residential Mortgage License – Lic/Reg#:MB.6850070; Indiana DFI Mortgage Lending License No. 59981; Maine Supervised Lender License No. SLM9525; Maryland Mortgage Lender License #17365; MA Mortgage Lender License #ML3542; Michigan 1st Mortgage Broker/Lender/Servicer Registrant #FL10015703; Licensed Residential Mortgage Lender NJ Dept of Banking & Insurance #3542; New Mexico Mortgage Loan Company License 3542; Licensed Mortgage Banker NYS Department of Financial Services #B500903 – NMLS#3542; North Carolina Mortgage Lender License L-180193; Ohio Mortgage Broker Act Mortgage Banker Exemption # MBMB.850088.000; Oregon: State of Oregon ML-3542; Pennsylvania Mortgage Lender License No. 47421; South Carolina-BFI Mortgage Lender / Servicer License MLS–3542; Tennessee Mortgage License – License/Registration #17365; Texas – SML Mortgage Banker Registration; Virginia License/Registration # MC-4985; Washington Department of Financial Institutions, Consumer Loan Company License CL-3542; Wisconsin – Mortgage Banker License, #ML3542;

NMLS: 3542