Compare Today’s Mortgage Rates

Key Takeaways

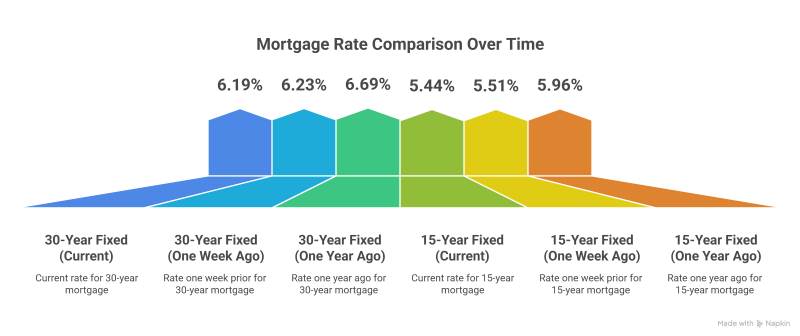

- National averages have eased: As of the week ending December 4, 2025, the average 30-year fixed mortgage rate is 6.19%, down from 6.23% the prior week; 15-year fixed averages 5.44%. (Freddie Mac)

- Refinance rates ticked slightly higher: By December 8, 2025, Zillow data (reported by Yahoo Finance) shows the 30-year fixed refinance rate around 6.10%, about 0.13 percentage points higher than the prior week. (Yahoo Finance)

- “Remember, these are the national averages and rounded to the nearest hundredth.” Your individual rate can be higher or lower depending on credit score, down payment, property type, and loan product.

- Markets remain volatile: Rates are reacting to Federal Reserve policy expectations, inflation data, and movements in the 10-year U.S. Treasury yield — all of which can push mortgage pricing up or down quickly. (AP News)

- New York borrowers still face affordability pressure, but slightly lower rates compared with a year ago mean improved purchasing power for some households. (Freddie Mac)

- Jet Direct Mortgage uses these national figures as educational benchmarks, not as live quotes. Even though the data comes from credible sources, rates can change daily or even several times per day.

- For current, scenario-specific numbers, Jet Direct Mortgage encourages borrowers to request a customized quote or pre-approval, rather than relying solely on national averages.

Where Mortgage Rates Stand Right Now

Recent reports from Realtor.com, Freddie Mac, AP News, and Yahoo Finance all paint a similar picture: rates have pulled back from their recent peaks but continue to bounce within a narrow band above 6%. (Realtor)

National Purchase-Mortgage Averages (Early December 2025)

| Loan Type | Average Rate* | One Week Ago | One Year Ago |

| 30-Year Fixed (FRM) | 6.19% | 6.23% | 6.69% |

| 15-Year Fixed (FRM) | 5.44% | 5.51% | 5.96% |

Refinance-Focused Snapshot (Zillow Data via Yahoo Finance)

| Loan Purpose | Key Product | Approx. National Average* | Weekly Move |

| Refinance | 30-Year Fixed Refinance | ≈ 6.10% | +0.13 pts |

| Refinance | 15-Year Fixed Refinance | High-5% range | Slightly up |

Remember, these are the national averages and rounded to the nearest hundredth.

Even though these rates are drawn from reliable, nationally recognized sources, they are not guaranteed offers. Lenders like Jet Direct Mortgage price loans based on live market conditions, investor demand, and your individual risk profile.

Why Have Rates Moved This Way?

Several overlapping forces are shaping mortgage rates in early December 2025:

- Bond yields have come down slightly as investors anticipate additional Federal Reserve rate cuts and moderating inflation. The 10-year Treasury — a key benchmark for mortgage pricing — has eased from prior highs. (AP News)

- Freddie Mac’s weekly survey shows a two-week decline in the average 30-year fixed rate — from 6.26% (mid-November) to 6.23%, then to 6.19% by December 4. (Freddie Mac)

- Short-term volatility persists: Zillow’s daily readings, cited by Yahoo Finance, show that refinance rates moved back up by about 13 basis points into December 8 — a reminder that markets don’t move in a straight line. (Yahoo Finance)

- Fed policy remains a wild card: While additional rate cuts are expected, mortgage rates are influenced more by investor expectations and inflation outlooks than by the Fed’s benchmark rate alone. (Investopedia)

For borrowers, the main takeaway is simple: we’re off the peak, but we’re not back to pandemic-era lows — and conditions can shift quickly.

How National Averages Are Calculated (And Why They Matter)

Most of the figures you see in the headlines come from large-scale surveys and data feeds:

- Freddie Mac Primary Mortgage Market Survey (PMMS) averages rates from lenders around the country, based on applications received from Thursday through Wednesday each week. (Freddie Mac)

- Zillow & other marketplace platforms track rate quotes and applications in real time, then aggregate them into daily “average” or “index” values. (Yahoo Finance)

- News outlets like Realtor.com, AP, and Yahoo Finance package that data into consumer-friendly stories, often adding context about Fed policy, housing demand, and affordability. (Realtor)

These averages are helpful benchmarks, but they are:

- Based on typical borrower profiles (often solid credit, moderate LTV, owner-occupied properties).

- Not tailored to a specific state like New York or to specialized loan types (e.g., VA, FHA, jumbo, reverse).

- Updated weekly or daily, so they can lag intraday movements.

That’s why Jet Direct Mortgage uses these figures to inform and educate readers, but always emphasizes a personalized quote before you make a decision.

What Today’s Rates Mean in Real Dollars

To understand the impact of 6.19% vs. higher levels, let’s look at a simple illustration for a standard 30-year fixed mortgage:

Example (for illustration only, not a quote):

- Loan amount: $400,000

- 30-year fixed at 6.19% → monthly principal & interest ≈ $2,447

- 30-year fixed at 7.00% → monthly principal & interest ≈ $2,661

That’s a difference of roughly $214 per month, or more than $2,500 per year in cash flow — without factoring in property taxes, insurance, or mortgage insurance.

This is exactly why even a 0.25%–0.50% shift in rates can materially change:

- Your maximum home price while keeping the same monthly budget.

- How soon you might want to refinance if rates move lower in the future.

- Whether shorter-term products (like 15-year loans) make sense for accelerated equity build-up.

The New York Context: Affordability & Existing Low-Rate Mortgages

National averages only tell part of the story. In markets like New York:

- Home prices remain elevated, so a moderate move in rates can significantly affect total monthly payments. (AP News)

- A large share of current homeowners still hold “legacy” mortgages below 6% — many even below 4% — making them reluctant to sell and take on a higher rate. (AP News)

That combination can:

- Keep inventory relatively tight, since owners with very low rates are less inclined to list their homes.

- Put more pressure on first-time buyers, who don’t have a low-rate mortgage to “trade in.”

- Make strategic refinancing, cash-out refinances, or HELOCs more nuanced decisions that require careful planning.

Jet Direct Mortgage works within these realities every day, helping New York borrowers navigate:

- Conventional home loans for purchases and refinances .

- Government-backed options like FHA and VA loans for borrowers needing more flexible credit or down-payment structures.

- Jumbo and specialty products for higher-priced New York properties.

Is Now a Good Time to Buy?

There is no one-size-fits-all answer, but current conditions suggest a few guidelines:

You may consider buying now if:

- Your income and employment are stable.

- You have enough funds for a responsible down payment and reserves.

- Current monthly payments at ~6.19% fit comfortably within your budget.

- You plan to stay in the home long enough to build equity and offset closing costs.

Potential advantages in the current environment:

- Rates are lower than a year ago, improving borrowing power for some households. (Freddie Mac)

- You can always explore options to refinance later if rates fall further.

- In some local pockets, slower demand has given buyers more room to negotiate.

You may want to pause or prepare if:

- You’re stretching beyond a safe debt-to-income ratio.

- You have very limited savings after closing.

- Your job or income is uncertain over the next 12–24 months.

Jet Direct Mortgage can help you model multiple scenarios — including different price points, down-payment levels, and rate assumptions — so you can decide if now is the right moment for you.

Is Now a Good Time to Refinance?

Refinancing decisions are even more individualized. The current ~6.10% refinance average suggests a mixed picture. (Yahoo Finance)

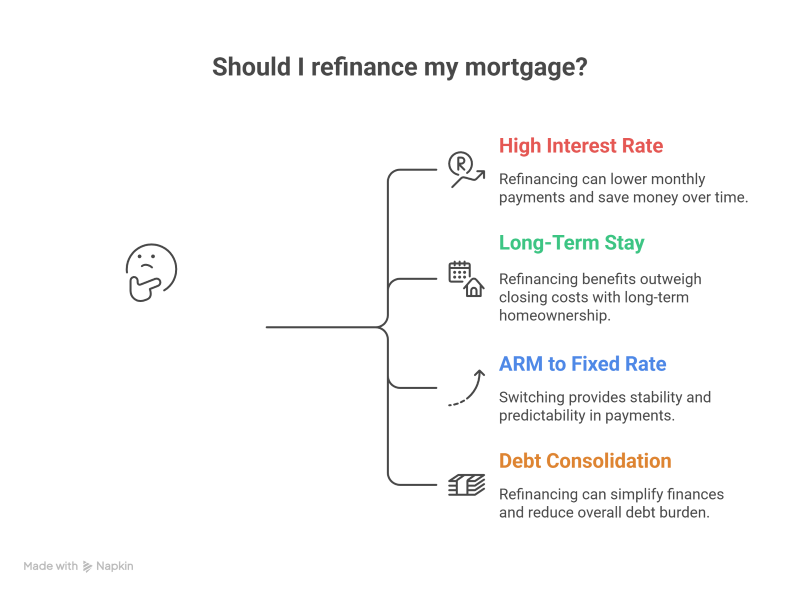

Refinancing might make sense if:

- Your existing mortgage rate is meaningfully higher (for example, mid-6s or 7%+).

- You plan to stay in the home long enough to recoup closing costs via interest savings.

- You want to switch from an adjustable-rate mortgage (ARM) to a fixed rate for stability.

- You’re consolidating higher-rate debts (credit cards, personal loans) into your mortgage, and the math still works in your favor.

Refinancing might be less attractive if:

- Your current rate is below today’s averages (e.g., under 6%).

- You’re planning to sell or relocate in the next 2–3 years.

- Your credit profile or income has weakened since you obtained your original loan.

For some New York borrowers, a target threshold might be:

- Refinance when you can lower your rate by 0.5–0.75 percentage points or more,

- Or when a refi helps you shorten the loan term without increasing your monthly payment by too much.

Because there’s no universal threshold, Jet Direct Mortgage runs break-even analyses, comparing:

- Current payment vs. new payment

- Upfront costs vs. long-term interest savings

- Impact on cash flow and equity over time

How Jet Direct Mortgage Uses Rate Data to Guide — Not Mislead — Borrowers

Even though the data presented here comes from credible, nationally recognized sources (Freddie Mac, AP, Realtor.com, Yahoo Finance, etc.), mortgage rates:

- Change periodically — sometimes daily, sometimes several times per day.

- Can vary significantly between purchase, refinance, cash-out, jumbo, FHA, VA, and reverse mortgage scenarios.

- Are strongly influenced by your unique borrower profile.

Jet Direct Mortgage relies on these national averages to inform and educate readers, but we do not treat them as guaranteed offers. Instead, we:

- Use them as context when discussing the market.

- Compare them with our live pricing systems to estimate potential savings or payment structures.

- Encourage borrowers to contact us directly for the latest rate numbers tailored to their situation.

Next Steps for New York Borrowers

If you’re:

- Buying a home in New York,

- Refinancing an existing mortgage, or

- Exploring specialized options like FHA, VA, jumbo, or reverse mortgages,

we recommend:

- Get a personalized rate quote

- Share your credit range, income, property type, and down-payment plans.

- Jet Direct will provide a tailored quote and break down estimated payments.

- Request a pre-approval

- Strengthen your offers in competitive New York markets.

- Understand your realistic price range before you start viewing homes.

- Discuss loan programs in detail

- Conventional vs. FHA vs. VA vs. jumbo.

- Fixed vs. adjustable-rate options.

- Shorter vs. longer terms (15-year vs. 30-year).

- Review long-term strategy

- When might it make sense to refinance in the future?

- How much equity could you build over 5, 10, or 15 years at current rates?

FAQ: U.S. Mortgage Rates & Late-2025 Changes

1. What is the average 30-year fixed mortgage rate as of early December 2025?

The national average for a 30-year fixed mortgage is about 6.19% for the week ending December 4, 2025, down from 6.23% the week before and from 6.69% a year earlier. (Freddie Mac)

2. How do refinance rates compare with purchase rates right now?

Refinance rates are similar but not identical. Zillow data, as reported by Yahoo Finance, puts the 30-year fixed refinance rate around 6.10% as of December 8, 2025 — slightly higher than some purchase-loan averages but still reflecting the broader downward trend from prior months. (Yahoo Finance)

3. Why did rates fall to 6.19% and are they likely to keep dropping?

Rates have eased due to lower Treasury yields, cooling inflation, and expectations of additional Fed cuts, but experts expect mortgage rates to hover slightly above 6% into 2026, not to return to the ultra-low levels seen during the pandemic. (AP News)

4. How often can mortgage rates change?

Rates can move:

- Daily, based on bond-market activity.

- Intraday, if markets are especially volatile.

That’s why the rate you see in a headline or article may differ from what you’re offered even a few hours later.

5. Are the national averages a good proxy for what I’ll pay in New York?

They’re a starting point, not a guarantee. Your actual rate depends on:

- Credit score and credit history

- Down-payment amount and loan-to-value ratio

- Debt-to-income ratio

- Property type (single-family, condo, co-op, multi-family)

- Loan product (Conventional, FHA, VA, jumbo, reverse, etc.)

Jet Direct Mortgage can help you translate national averages into real, personalized numbers for your New York transaction.

6. If I already have a rate below 6%, should I refinance now?

In most cases, a refinance is most compelling when you can reduce your rate by at least 0.5–0.75 percentage points, shorten your term, or meaningfully improve your cash flow or overall financial picture. If your current loan is already below 6%, you may not gain much from refinancing at today’s averages — but there are exceptions (e.g., changing loan type, removing a co-borrower, consolidating high-interest debt).

7. How can I get the latest rate numbers from Jet Direct Mortgage?

Because rates are from credible sources but may change periodically, the most reliable way to get up-to-the-minute figures is to contact Jet Direct Mortgage directly. A loan specialist can review your profile and provide live, scenario-specific pricing rather than broad averages.

👉 Start here: https://jetdirectmortgage.com/contact/

Final Thoughts:

“In a market where rates move by the day and every borrower’s story is different, the smartest decision isn’t to chase headlines — it’s to get advice tailored to you. At Jet Direct Mortgage, we turn national averages into personalized strategies, so you can move forward with clarity and confidence.”

If you’re thinking about buying, refinancing, or simply want to understand what today’s mortgage rates mean for you, reach out to Jet Direct Mortgage for a personalized consultation and live rate quote:

➡️ Contact Jet Direct Mortgage: https://jetdirectmortgage.com/contact/

Sources

- Realtor.com – Article on early-December 2025 mortgage rate trends and the 6.19% national 30-year average. (Realtor)

- Yahoo Finance (via Zillow data) – Mortgage and refinance interest-rate update for Monday, December 8, 2025. (Yahoo Finance)

- Freddie Mac – Primary Mortgage Market Survey (PMMS) – Weekly national averages for 30-year and 15-year fixed-rate mortgages as of December 4, 2025. (Freddie Mac)

- AP News – Coverage of U.S. long-term mortgage rates falling to 6.19% and broader economic context. (AP News)

- Federal Reserve Bank of St. Louis (FRED) – Data series on the 30-year fixed mortgage average in the United States. (FRED)

Experienced Chief Operating Officer with a 26 + year demonstrated history of working in the banking industry. Skilled in all aspects of the residential mortgage market . Strong business development professional with a Bachelor of Science (BS) focused in Business Administration and Management, from St. Joseph College. A direct endorsement underwriter and a licensed Mortgage Loan Originator.