A New York conventional mortgage is one of the most widely used and versatile home financing options available to buyers and homeowners across the state. From high-density urban markets like New York City to suburban communities on Long Island and quieter upstate regions, conventional mortgages continue to be a cornerstone of residential real estate financing.

Whether purchasing a primary residence, acquiring a second home, or refinancing an existing mortgage, a conventional loan offers a practical and reliable path to homeownership in New York’s dynamic housing market.

Understanding Conventional Mortgages in New York

A conventional mortgage is a home loan that is not backed by a federal government agency. These loans follow standards set by Fannie Mae and Freddie Mac and are funded through private lending institutions.

- Owner-occupied primary residences

- Cooperative apartments and condominiums

- Second homes and vacation properties

- Residential investment properties

- Multifamily homes with up to four units

Why Conventional Mortgages Are So Popular in New York

New York’s real estate market demands financing solutions capable of handling complexity. Property values vary widely, ownership structures differ by region, and transactions often involve multiple professional parties.

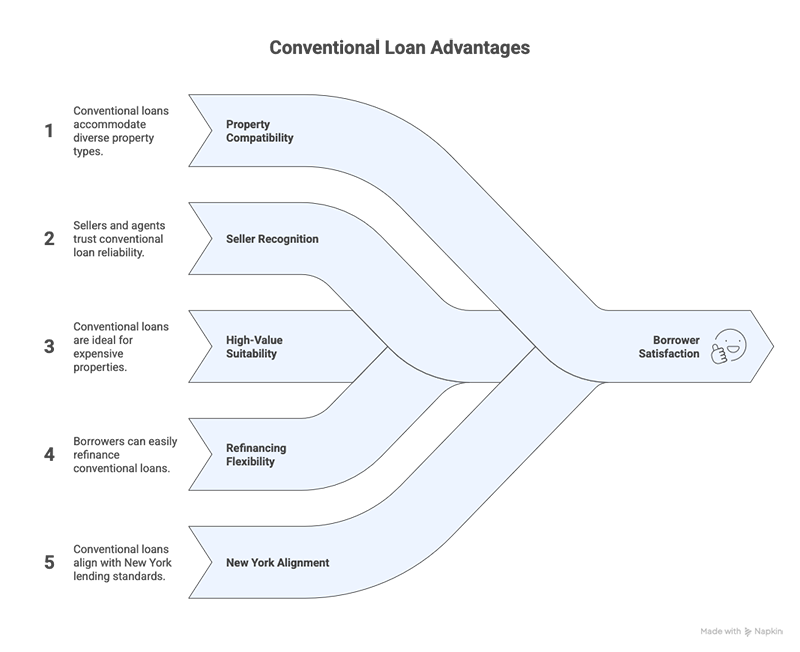

Key Reasons Borrowers Choose Conventional Loans

- Broad property compatibility including co-ops and condos

- Strong recognition among sellers and agents

- Suitability for higher-value properties

- Long-term refinancing flexibility

- Alignment with New York lending practices

Types of Conventional Mortgages Available in New York

Conforming Conventional Loans

Conforming loans adhere to established loan size guidelines and are the most common type of conventional mortgage used in New York.

Jumbo Conventional Loans

When a home’s price exceeds conforming loan thresholds, a jumbo conventional mortgage may be required. These are frequently used in higher-cost markets such as Manhattan, Brooklyn, Nassau, Suffolk, and Westchester counties.

Who Is a Good Candidate?

- Professionals with consistent employment histories

- Self-employed individuals with documented income

- Buyers seeking condo or co-op financing

- Homeowners refinancing existing loans

- Investors purchasing rental properties

Credit and Financial Profile Considerations

Credit History

A strong credit profile expands available loan options and often provides more favorable terms.

Income Stability

Consistent income establishes repayment reliability and supports underwriting approval.

Existing Financial Obligations

Lenders assess how current obligations align with projected housing costs.

Property Types Commonly Financed

- Single-family homes

- Townhomes and row houses

- Condominiums

- Cooperative apartments

- Two- to four-unit residential properties

- Second homes

- Investment properties

Conventional Loans Compared to Other Mortgage Options

| Feature | Conventional Loan | Government-Backed Loan |

|---|---|---|

| Government Insurance | No | Yes |

| Property Flexibility | High | Program-Specific |

| Refinancing Options | Flexible | Structured Guidelines |

| Use for Investment Property | Yes | Limited |

The Conventional Mortgage Process in New York

- Initial Consultation and Pre-Approval – Financial review and planning

- Property Selection and Contract – Offer submission

- Formal Application – Documentation submission

- Underwriting Review – Detailed evaluation

- Final Approval and Closing – Loan funding

Frequently Asked Questions

What is a conventional mortgage in New York?

A privately backed home loan that follows established lending guidelines and is widely used across New York residential markets.

Can conventional mortgages be used for co-ops?

Yes. They are one of the most common financing options for cooperative apartments in New York City.

Are conventional loans only for primary residences?

No. They can also be used for second homes and residential investment properties.

Is a conventional mortgage a good option for refinancing?

Yes. Many homeowners use conventional mortgages to restructure and improve long-term financing strategies.

Contact Jet Direct Mortgage

Website: https://jetdirectmortgage.com

Phone: +1.800.700.4JET

Email: express@jetdirectmortgage.com

Address: 4875 Sunrise Hwy, Suite 300, Bohemia, New York 11716

Jet Direct Mortgage © 2026. All Rights Reserved.

NMLS: 3542

Alabama Consumer Credit License – License/Registration #22632; Arizona Mortgage Banker License – Lic/Reg#:1040763; Licensed by the Department of Financial Protection and Innovation under the California Residential Mortgage Lending Act – #41DBO-81230; Colorado Mortgage Company Registration #LMB100014791; Connecticut Mortgage Lender License #20333; Delaware Lender License – License/Registration #032943; Florida Mortgage Lender Servicer License #MLD357; Licensed by the Georgia Department of Banking and Finance Company License Company – License #64345; Illinois Residential Mortgage License – Lic/Reg#:MB.6850070; Indiana DFI Mortgage Lending License No. 59981; Maine Supervised Lender License No. SLM9525; Maryland Mortgage Lender License #17365; MA Mortgage Lender License #ML3542; Michigan 1st Mortgage Broker/Lender/Servicer Registrant #FL10015703; Licensed Residential Mortgage Lender NJ Dept of Banking & Insurance #3542; New Mexico Mortgage Loan Company License 3542; Licensed Mortgage Banker NYS Department of Financial Services #B500903 – NMLS#3542; North Carolina Mortgage Lender License L-180193; Ohio Mortgage Broker Act Mortgage Banker Exemption # MBMB.850088.000; Oregon: State of Oregon ML-3542; Pennsylvania Mortgage Lender License No. 47421; South Carolina-BFI Mortgage Lender / Servicer License MLS–3542; Tennessee Mortgage License – License/Registration #17365; Texas – SML Mortgage Banker Registration; Virginia License/Registration # MC-4985; Washington Department of Financial Institutions, Consumer Loan Company License CL-3542; Wisconsin – Mortgage Banker License, #ML3542.

All loan programs are subject to credit approval, underwriting guidelines, and property eligibility.

Experienced Chief Operating Officer with a 26 + year demonstrated history of working in the banking industry. Skilled in all aspects of the residential mortgage market . Strong business development professional with a Bachelor of Science (BS) focused in Business Administration and Management, from St. Joseph College. A direct endorsement underwriter and a licensed Mortgage Loan Originator.