Programs, Costs, and Smart Strategies for 2026

Buying your first home in New York is a meaningful milestone that represents stability, independence, and long-term investment. It is also a process shaped by unique state regulations, competitive housing markets, and complex local requirements that can feel overwhelming without clear, reliable guidance. From New York City and Long Island to Westchester and upstate communities, first-time buyers face conditions that differ significantly from much of the country.

At the same time, New York offers some of the most comprehensive first-time home buyer support programs in the United States. With the right preparation, education, and professional support, homeownership is achievable for many residents who assume it may be out of reach.

Who Qualifies as a First-Time Home Buyer in New York?

In New York, a first-time home buyer is generally defined as an individual who has not owned a primary residence within the past three years. This definition is used by many state, city, and county housing programs and is broader than many buyers expect.

You may still qualify as a first-time home buyer if:

- You previously owned a home but sold it more than three years ago

- You are purchasing a home after a divorce and no longer own property

- You are buying with a spouse or partner who has owned a home, but you have not

- You owned an investment or rental property but not a primary residence

This expanded definition allows many buyers to access programs and benefits they might otherwise overlook. Because eligibility rules can vary slightly by program, it is important to confirm requirements with a knowledgeable local lender or housing counselor.

Why Buying Your First Home in New York Is Different

New York’s housing market is shaped by factors that set it apart from most other states. Understanding these distinctions early can help first-time buyers plan more effectively and avoid unexpected complications.

Key Characteristics of the New York Housing Market

- Higher home values in many regions, particularly in New York City, Long Island, and Westchester County

- Wide variation in property taxes, often influenced by school districts and local municipalities

- A large number of co-ops and condominiums, especially in urban and suburban areas

- Attorney involvement in most residential real estate transactions

- Highly competitive markets, where preparation and documentation matter

While these conditions can present challenges, New York also invests heavily in programs designed to promote sustainable homeownership, especially for first-time buyers.

New York First Time Home Buyer Programs

State of New York Mortgage Agency (SONYMA)

The State of New York Mortgage Agency (SONYMA) plays a central role in expanding access to homeownership throughout the state. SONYMA programs are specifically designed to support first-time buyers by improving affordability and reducing common barriers to entry.

SONYMA-backed mortgages often feature:

- Accessible eligibility requirements for first-time buyers

- Fixed-rate loan structures that support long-term stability

- Compatibility with additional assistance programs

- Standards designed to support sustainable homeownership

Some of the most well-known SONYMA programs include:

- Achieving the Dream

- Low Interest Rate Program

- Conventional Plus

- Down Payment Assistance Loan (DPAL)

Each program has specific income limits, purchase price limits, and property eligibility requirements that vary by location. Program details are administered and updated by New York State Homes and Community Renewal, which oversees SONYMA’s mission to promote safe and affordable housing statewide.

Authoritative reference:

https://hcr.ny.gov/sonyma

City and County First-Time Home Buyer Assistance

In addition to statewide programs, many New York municipalities offer localized assistance designed to address regional housing challenges. These programs often work alongside SONYMA or conventional financing options.

Examples of local assistance include:

- New York City’s HomeFirst Program

- Nassau County first-time buyer initiatives

- Suffolk County housing assistance programs

- Westchester County HOME Investment Partnership resources

Local programs may provide grants, deferred loans, or closing cost support, typically subject to income limits, residency requirements, and owner-occupancy rules. Because funding availability can change, early application and guidance from a local lender or housing counselor are especially important.

Authoritative reference:

https://www.nyc.gov/site/hpd/services-and-information/homefirst-down-payment-assistance-program.page

Understanding Financing Options as a First-Time Buyer

Financing a first home in New York involves selecting a mortgage structure that aligns with both current affordability and long-term financial goals. First-time buyers have access to several common loan types, each with distinct eligibility and property requirements.

Common Financing Options for First-Time Buyers

- Conventional loans, often used for single-family homes, condos, and some co-ops

- Government-backed loans, such as FHA or VA loans, depending on eligibility

- SONYMA-backed mortgages, designed specifically for New York residents

- Specialized programs, depending on profession, location, or household structure

The best option depends on factors such as credit profile, income, property type, and future plans. A knowledgeable mortgage professional can help evaluate which structure aligns best with a buyer’s goals.

The Step-by-Step Home Buying Process in New York

Understanding the process from start to finish helps first-time buyers feel more confident and prepared.

1. Mortgage Pre-Approval

Pre-approval verifies income, assets, and credit, establishing a realistic price range and strengthening a buyer’s position when submitting offers.

2. Home Search With a Local Real Estate Agent

A New York-based agent understands neighborhood trends, property taxes, and local market dynamics that can significantly affect affordability and resale value.

3. Making an Offer

Offers may include negotiations around price, contingencies, and closing timelines. In competitive markets, strong documentation and flexibility can make a meaningful difference.

4. Home Inspection

Inspections help identify potential structural or mechanical issues and provide an opportunity to negotiate repairs or credits.

5. Attorney Review and Contract Execution

Attorney involvement is standard in New York, helping ensure contracts accurately reflect negotiated terms and protect buyer interests.

6. Mortgage Processing and Appraisal

Lenders confirm property value, finalize underwriting conditions, and prepare for closing.

7. Closing

Most New York home purchases close within 45 to 75 days, though timelines can vary depending on property type and transaction complexity.

Credit Expectations for First-Time Buyers

A strong credit profile can improve financing options, but perfect credit is not required to buy a first home in New York.

General guidelines often include:

- More flexible credit standards for government-backed and SONYMA loans

- Conventional financing that typically requires higher credit benchmarks

- Additional review for co-op purchases, which may involve board-level financial scrutiny

Improving credit before applying—by paying down balances, avoiding new debt, and correcting errors—can expand options and improve overall affordability.

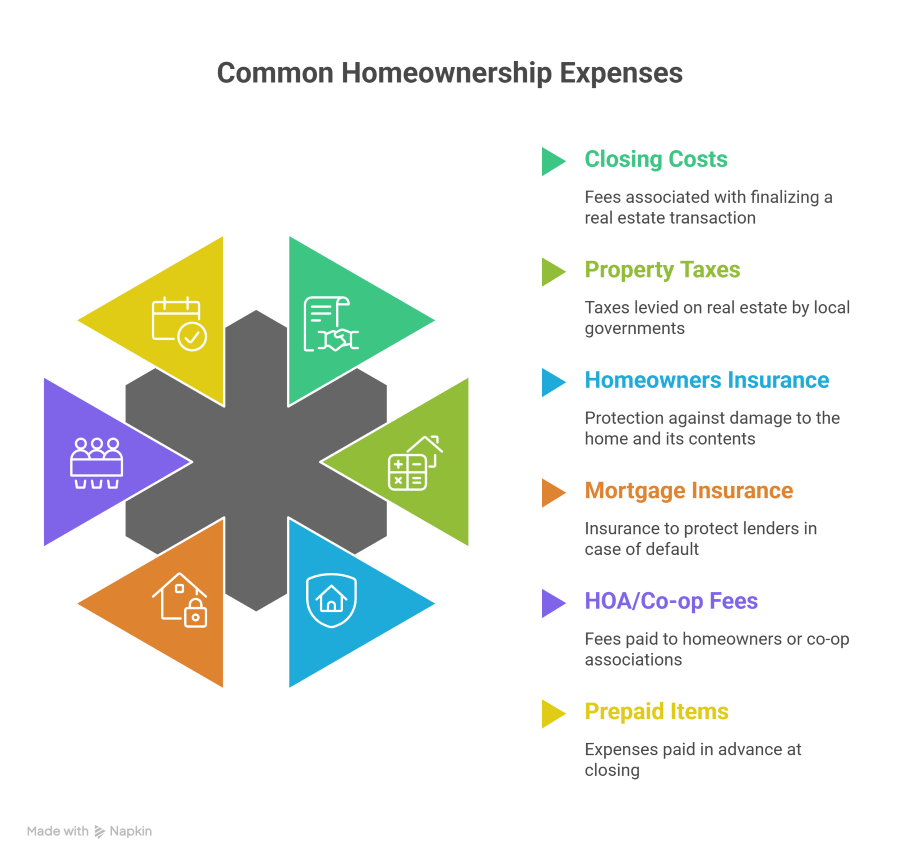

Costs Beyond the Purchase Price

First-time buyers often focus on the home price itself, but ownership comes with additional costs that should be planned for in advance.

Common expenses include:

- Closing costs, which may include lender fees, legal fees, and title charges

- Property taxes, which vary widely across New York counties

- Homeowners insurance

- Mortgage insurance, if applicable

- HOA or co-op maintenance fees

- Prepaid items collected at closing

Understanding these expenses early helps buyers budget responsibly and avoid financial strain after closing.

Co-Ops, Condos, and Single-Family Homes: Key Differences

New York offers a wide range of property types, each with unique considerations.

Single-Family Homes

- Typically offer full ownership and control

- Property taxes and maintenance are the owner’s responsibility

Condominiums

- Individual ownership with shared common areas

- Monthly association fees apply

- Financing guidelines vary by project

Co-Ops

- Ownership is structured as shares in a corporation

- Board approval is required

- Financial requirements can be more stringent

Choosing the right property type depends on lifestyle, budget, and long-term goals.

Common First-Time Buyer Mistakes to Avoid

- Skipping mortgage pre-approval

- Underestimating total ownership costs

- Ignoring property tax implications

- Making large financial changes before closing

- Choosing a loan structure without understanding long-term impact

Avoiding these pitfalls can reduce stress and improve the overall buying experience.

Why Local Expertise Matters in New York

New York’s regulatory environment, housing stock, and assistance programs make local expertise especially valuable. A lender familiar with New York can help navigate:

- State and municipal assistance guidelines

- Co-op and condo financing rules

- Local appraisal standards

- Compliance requirements unique to New York

This expertise often results in smoother transactions and fewer unexpected delays.

Quick Answers for New York First Time Home Buyers

How much money do I need to buy my first home in New York?

The total amount needed varies based on location, property type, and financing structure. Many buyers qualify for assistance programs that reduce upfront costs.

Are first-time buyer programs income-restricted?

Most programs have income limits that vary by household size and location.

Is homebuyer education required?

Some state and local programs require completion of an approved homebuyer education course.

How long does the home buying process take?

Most transactions close within 45 to 75 days, depending on the property and financing.

FAQ’s

Do first-time buyers receive special tax treatment in New York?

Some local programs may offer incentives, but property taxes are generally based on assessed value rather than buyer status.

Can first-time buyers purchase co-ops?

Yes, though co-ops often require board approval and stricter financial review.

Can multiple assistance programs be combined?

In many cases, state and local programs can be layered, subject to eligibility rules.

What role does a real estate attorney play?

Attorneys review contracts, manage negotiations, and help protect buyer interests throughout the transaction.

Key Takeaways for New York First Time Home Buyers

- First-time buyer status often applies if you have not owned a home in the past three years

- New York offers strong state and local assistance programs

- Understanding total ownership costs is essential

- Preparation and education are critical in competitive markets

- Local mortgage and real estate expertise can simplify the process

Take the Next Step Toward Homeownership

Homeownership in New York is achievable with the right planning, professional guidance, and realistic expectations. With clear information and experienced support, first-time buyers can move forward confidently and build a strong foundation for the future.

Jet Direct Mortgage is committed to helping first-time buyers across New York understand their options and navigate the home financing process with clarity and care.

Contact Information

Website: https://jetdirectmortgage.com

Phone: +1.800.700.4JET

Email: express@jetdirectmortgage.com

Address: 4875 Sunrise Hwy, Suite 300, Bohemia, New York 11716

Explore Mortgage Programs

Learn more about available home loan options:

https://jetdirectmortgage.com/home-loan-programs/

Licensing and Legal Disclosure

Jet Direct Mortgage © 2026. All Rights Reserved.

NMLS: 3542

Alabama Consumer Credit License – License/Registration #22632; Arizona Mortgage Banker License – Lic/Reg#:1040763; Licensed by the Department of Financial Protection and Innovation under the California Residential Mortgage Lending Act – #41DBO-81230; Colorado Mortgage Company Registration #LMB100014791; Connecticut Mortgage Lender License #20333; Delaware Lender License – License/Registration #032943; Florida Mortgage Lender Servicer License #MLD357; Licensed by the Georgia Department of Banking and Finance Company License Company – License #64345; Illinois Residential Mortgage License – Lic/Reg#:MB.6850070; Indiana DFI Mortgage Lending License No. 59981; Maine Supervised Lender License No. SLM9525; Maryland Mortgage Lender License #17365; MA Mortgage Lender License #ML3542; Michigan 1st Mortgage Broker/Lender/Servicer Registrant #FL10015703; Licensed Residential Mortgage Lender NJ Dept of Banking & Insurance #3542; New Mexico Mortgage Loan Company License 3542; Licensed Mortgage Banker NYS Department of Financial Services #B500903 – NMLS#3542; North Carolina Mortgage Lender License L-180193; Ohio Mortgage Broker Act Mortgage Banker Exemption # MBMB.850088.000; Oregon: State of Oregon ML-3542; Pennsylvania Mortgage Lender License No. 47421; South Carolina-BFI Mortgage Lender / Servicer License MLS–3542; Tennessee Mortgage License – License/Registration #17365; Texas – SML Mortgage Banker Registration; Virginia License/Registration # MC-4985; Washington Department of Financial Institutions, Consumer Loan Company License CL-3542; Wisconsin – Mortgage Banker License, #ML3542.

All loan programs are subject to credit approval, underwriting guidelines, and property eligibility.

Experienced Chief Operating Officer with a 26 + year demonstrated history of working in the banking industry. Skilled in all aspects of the residential mortgage market . Strong business development professional with a Bachelor of Science (BS) focused in Business Administration and Management, from St. Joseph College. A direct endorsement underwriter and a licensed Mortgage Loan Originator.