A New York reverse mortgage has become an increasingly relevant financial option for homeowners who want to remain in their homes while accessing the value they have built over years of ownership. Across New York City, Long Island, and upstate communities, many homeowners are asset-rich but seeking greater financial flexibility as living costs and lifestyle priorities evolve later in life.

What Is a Reverse Mortgage in New York?

A reverse mortgage allows eligible homeowners to convert a portion of their home’s value into accessible funds while maintaining ownership and occupancy. Unlike traditional mortgage products, homeowners are not required to make ongoing monthly mortgage payments as long as they live in the property and meet basic obligations.

- Higher-than-average property values

- Long-term homeownership trends

- Strong state-level consumer protections

- Diverse housing types

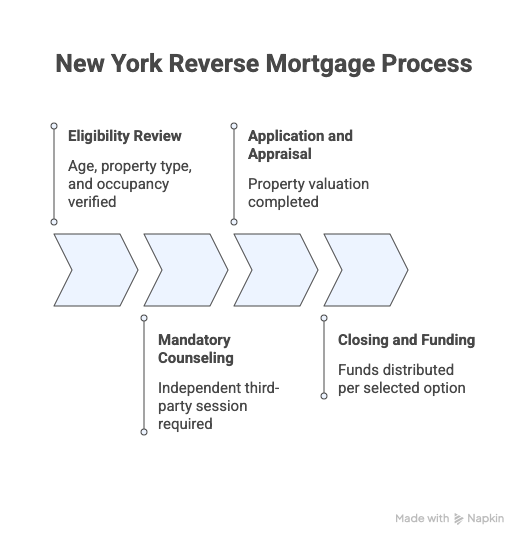

How a New York Reverse Mortgage Works

Step-by-Step Overview

- Eligibility Review – Age, property type, and occupancy verified

- Mandatory Counseling – Independent third-party session required

- Application and Appraisal – Property valuation completed

- Closing and Funding – Funds distributed per selected option

Ongoing Responsibilities

- Maintain primary residence occupancy

- Keep property in reasonable condition

- Pay property taxes

- Maintain homeowners insurance

Reverse Mortgage Options Available in New York

Home Equity Conversion Mortgage (HECM)

The HECM is the most widely used reverse mortgage program in the United States and is federally insured.

- Administered under federal guidelines

- Mandatory third-party counseling

- Available for eligible primary residences

- Subject to national lending limits

Official HUD information:

https://www.hud.gov/program_offices/housing/sfh/hecm

Proprietary (Jumbo) Reverse Mortgages

Designed for higher-value properties common throughout New York City, Long Island, and affluent suburban areas.

- Suitable for properties exceeding federal limits

- Flexible structures for qualifying borrowers

- Additional consumer safeguards under New York law

Reverse Mortgage Options Comparison

| Feature | HECM | Proprietary Reverse |

|---|---|---|

| Insurance | Federally insured | Privately offered |

| Property Value Limits | National lending cap applies | Designed for higher-value homes |

| Counseling Requirement | Mandatory | Mandatory in NY |

| Best For | Standard property values | Luxury / high-value properties |

Eligibility Requirements

Borrower Qualifications

- Minimum age requirement

- Primary residence status

- Ability to meet ongoing obligations

- Completion of approved counseling

Property Eligibility

- Single-family homes

- Approved condominiums

- Certain multi-unit properties (owner-occupied)

Location Differences in New York

New York City & Long Island

- High property values favor proprietary options

- Co-ops often have limited eligibility

- Condominiums require strict approval

Upstate & Suburban Regions

- Single-family homes most common

- HECM often sufficient

- Lower property values still offer flexibility

Reverse Mortgage vs. Selling the Home

| Reverse Mortgage | Selling the Home |

|---|---|

| Remain in home | Relocate required |

| Access home value gradually | Receive lump sum from sale |

| No required monthly mortgage payments | No mortgage after sale |

| Maintain ownership | Transfer ownership |

Common Uses for Reverse Mortgage Funds

- Daily household expenses

- Healthcare needs

- Home improvements

- Family support

Frequently Asked Questions

Can heirs keep the home?

Yes. Heirs may resolve the loan balance through refinancing, sale, or other resources.

Does it affect Social Security or Medicare?

Generally no, but needs-based assistance recipients should consult a professional.

Is counseling required?

Yes. New York mandates approved third-party counseling.

What happens if I move?

If the home is no longer your primary residence, the loan becomes due.

Contact Jet Direct Mortgage

Website: https://jetdirectmortgage.com

Phone: +1.800.700.4JET

Email: express@jetdirectmortgage.com

Address: 4875 Sunrise Hwy, Suite 300, Bohemia, New York 11716

Jet Direct Mortgage © 2026. All Rights Reserved.

NMLS: 3542

Alabama Consumer Credit License – License/Registration #22632; Arizona Mortgage Banker License – Lic/Reg#:1040763; Licensed by the Department of Financial Protection and Innovation under the California Residential Mortgage Lending Act – #41DBO-81230; Colorado Mortgage Company Registration #LMB100014791; Connecticut Mortgage Lender License #20333; Delaware Lender License – License/Registration #032943; Florida Mortgage Lender Servicer License #MLD357; Licensed by the Georgia Department of Banking and Finance Company License Company – License #64345; Illinois Residential Mortgage License – Lic/Reg#:MB.6850070; Indiana DFI Mortgage Lending License No. 59981; Maine Supervised Lender License No. SLM9525; Maryland Mortgage Lender License #17365; MA Mortgage Lender License #ML3542; Michigan 1st Mortgage Broker/Lender/Servicer Registrant #FL10015703; Licensed Residential Mortgage Lender NJ Dept of Banking & Insurance #3542; New Mexico Mortgage Loan Company License 3542; Licensed Mortgage Banker NYS Department of Financial Services #B500903 – NMLS#3542; North Carolina Mortgage Lender License L-180193; Ohio Mortgage Broker Act Mortgage Banker Exemption # MBMB.850088.000; Oregon: State of Oregon ML-3542; Pennsylvania Mortgage Lender License No. 47421; South Carolina-BFI Mortgage Lender / Servicer License MLS–3542; Tennessee Mortgage License – License/Registration #17365; Texas – SML Mortgage Banker Registration; Virginia License/Registration # MC-4985; Washington Department of Financial Institutions, Consumer Loan Company License CL-3542; Wisconsin – Mortgage Banker License, #ML3542.

All loan programs are subject to credit approval, underwriting guidelines, and property eligibility.

Experienced Chief Operating Officer with a 26 + year demonstrated history of working in the banking industry. Skilled in all aspects of the residential mortgage market . Strong business development professional with a Bachelor of Science (BS) focused in Business Administration and Management, from St. Joseph College. A direct endorsement underwriter and a licensed Mortgage Loan Originator.