Staten Island Mortgage Refinance: Everything You Need to Know

If you’ve been a homeowner for a while, but you are looking to improve your position in the real estate market, mortgage refinancing can be an excellent opportunity to get better loan terms and improve your financial stability.

The “borough of parks – Staten Island, is an especially attractive market for mortgage refinancing. It boasts a steady demand for housing, has access to numerous parks and green spaces, and has a low perceived risk for investment.

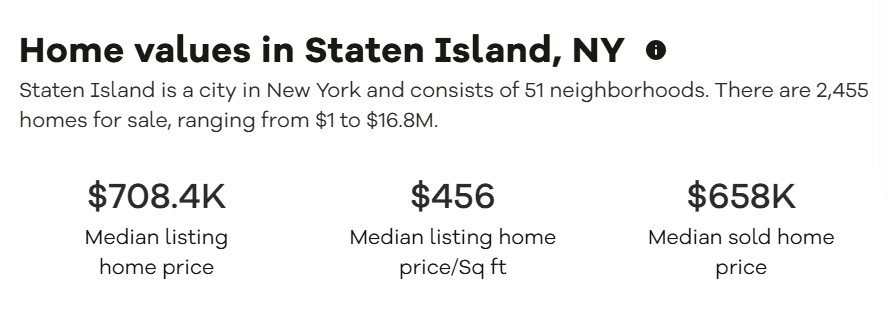

With a median listing home price of $708k, Staten Island is more affordable compared to other New York City boroughs. At the same time, it is a highly desired location thanks to its suburban lifestyle and quiet atmosphere.

In this article, we will deep dive into everything you need to know about Staten Island mortgage refinance – continue reading to learn more.

Ready to Start the Mortgage Process?

Image source: realtor.com

What is a Staten Island mortgage refinance?

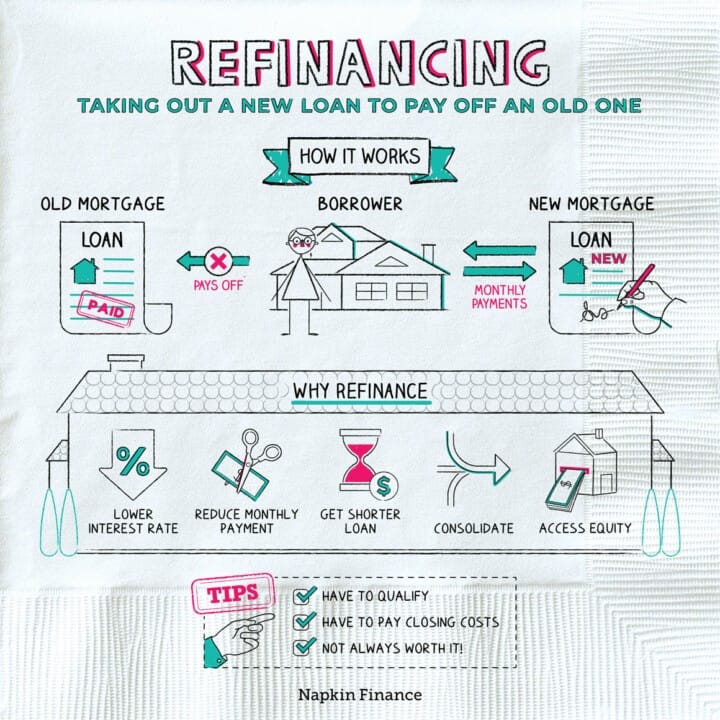

A Staten Island mortgage refinance is really just mortgage refinancing in one of New York City’s top boroughs – in other words, a financial product that allows you to replace your existing mortgage with a new one to unlock benefits such as better terms and rates.

While mortgage refinancing in Staten Island is subject to the same economic influences as New York City and the national housing markets, it still has some distinctive characteristics that you need to consider before application.

Some of them include:

- Market Volatility – Compared to other boroughs such as Manhattan and Brooklyn, Staten Island’s real estate market tends to be less volatile. However, this is good news for you as a borrower – it means more stability in housing prices, which leads to safer bets for lending institutions. This often leads to better refinancing terms.

- Property Values – The local economy, including employment rates and major economic developments, can impact property values and the attractiveness of Staten Island mortgage refinance. For example, new transportation projects or commercial developments can enhance property values and influence refinancing decisions.

- Interest Rate Environment – Another key consideration that you’ll need to keep in mind before applying for Staten Island mortgage refinance is the interest rate environment. Refinancing rates in the area are influenced by the overall economic climate, which includes federal interest rate decisions.

- Property Types – The type of property that you are looking to refinance also matters when it comes to Staten Island mortgage refinance. The value of the property relative to the rest of the NYC market can affect the terms that your lending institution will offer you.

Why Should I Apply For a Staten Island Mortgage refinance?

So, you might be wondering – why should I apply for a mortgage refinancing in Staten Island instead of staying with my current mortgage rates and terms? Logically, this financial move will only make sense if it offers benefits that outweigh your time, effort, and costs involved.

Here are some of the main reasons why you should apply for a Staten Island mortgage refinance:

So You Can Lower Your Monthly Payments

If you play your cards right, you can reap one of the main benefits of getting a mortgage refinance – and that is, lowering your monthly payments. By getting an interest rate that’s lower than your original mortgage, you will pay less interest each month.

Considering that interest is an important part of each mortgage payment, getting a lower rate usually means that you will pay less to the bank, and keep more of your money for other uses. Even a small decrease can lead to substantial savings!

For example, let’s say that you took out a $700k mortgage on your Staten Island home at a 4.5% interest rate with a 30-year term. In that case, you would pay $3,543 towards your monthly principal and interest payment.

However, if you refinance your remaining balance of $630k to a new 30-year loan at a rate of 3.5%, your new monthly payment would drop to $2,832 (for both principal and interest). Let’s take a look at the numbers at a glance:

- Original Loan: $700,000 at 4.5% for 30 years = $3,543/month

- Refinanced Loan: $630,000 at 3.5% for 30 years = $2,832/month

By getting a Staten Island mortgage refinance, your annual savings would amount to almost $8.5k, which is great – but the savings over 30 years can be more than $255k!

So You Can Shorten The Term Of Your Loan

Another reason why you should get a Staten Island mortgage refinance is so you can shorten the term of your loan.

If you feel comfortable paying higher monthly payments, but reducing the term of the loan from 30 years to 15 years, you can save a lot of money as you will be paying a lot less overall interest throughout the life of the loan.

Let’s go back to our example of $700k. If your current home loan is for a $700k property (which is the median listing price in Staten Island), and your interest rate is 4.5%, you are probably paying around $3.5k in monthly payments for a term of 30 years.

However, the total interest paid on your loan, considering these parameters, will be $3,543 × 360 − 700,000 ≈ $975,480.

If you refinance to a 15-year mortgage at a 3.5% interest rate, you will probably pay higher monthly payments – around $5k, but the total interest paid throughout the life of the loan will be less: Total Interest = $5,006 ×180− 700,000 ≈ $200,080.

So You Can Access Home Equity

The benefits of a Staten Island mortgage refinance don’t end here. You can also take advantage of this financial strategy in order to access home equity. But what does this mean exactly?

Accessing home equity through mortgage refinancing means that you can convert a portion of the equity you’ve built up in your home into cash.

This is often done through a cash-out refinance, where you take out a new mortgage for more than you owe on your existing mortgage and receive the difference in cash. You can use this cash to make home improvements, update your kitchen, or pay off high-interest credit card debt.

To give you a practical example, let’s say that the value of your home is $600k, and the remaining balance on your mortgage is $300k. If you are looking for a cash-out amount of $100k, you can get a new loan for $400k to achieve that.

So You Can Consolidate Debt

Another key benefit of getting a Staten Island mortgage refinance is debt consolidation. One way to approach this is by combining debt – in other words, you can choose to borrow more than the amount you currently owe on your home, and use the excess funds to pay off other debts, such as car loans or student loans.

This new loan will replace your old mortgage, and it will include the additional funds you need to cover your other debts. So, instead of making multiple debt payments each month, you only make one consolidated payment toward your mortgage.

When Is a Good Time to Apply For a Staten Island Mortgage refinance?

You might be thinking that a State Island mortgage refinance is always a good idea, and while it certainly can be very beneficial, there are some scenarios in which you should wait until you are in a better position.

You will know it’s time to refinance if:

- Interest rates have dropped since you took out your initial mortgage

- Your credit score has improved since you took your home loan

- You want to pay off your mortgage faster

- You need cash for a major expense, such as a home renovation

- Rates are starting to rise, and you want to switch from ARM to FRM

On another hand, you might want to hold off refinancing if:

- You plan to sell your home soon, meaning your closing costs might not be recouped

- Your new interest rate won’t be sufficiently lower compared with your previous one

- You don’t owe much on your mortgage

- Your current mortgage has benefits you could lose, such as no prepayment penalties

- Economic conditions are unstable, or your income is not secure

Getting a Staten Island Mortgage Refinance With Jet Direct Mortgage

If you are looking to get a Staten Island mortgage refinance, look no further than Jet Direct Mortgage, your trusted partner in the local real estate market. Our team of highly experienced professionals will ensure a smooth, transparent and efficient refinancing process from start to finish. Apply here.

FAQ

What are the closing costs for refinancing in Staten Island, and who covers them?

In Staten Island, the closing costs for refinancing include appraisal fees, attorney fees, title insurance, and origination fees.

The borrower is generally responsible for covering these costs, which can be paid upfront or sometimes rolled into the loan balance, depending on the lender’s terms and the type of refinancing.

How long will it take to break even on my refinancing costs?

The break-even point on refinancing costs is calculated by dividing the total closing costs by the monthly savings from the new lower payment.

For example, if refinancing costs $5,000 and you save $250 per month, it will take 20 months to break even. This timeframe is crucial for deciding whether refinancing is worth it, especially if you plan to move or pay off the loan within that period.

Do I qualify for a refinance loan in Staten Island?

To qualify for a refinance loan in Staten Island, you typically need a good credit score, a stable income, and sufficient home equity. Lenders will also look at your debt-to-income ratio to ensure you can manage the new loan payments.

Meeting these criteria makes you a strong candidate for refinancing.

How long does the refinance process take?

The refinancing process typically takes between 30 to 45 days to complete. This timeframe includes the application, documentation gathering, appraisal, underwriting, and finally closing.

The exact duration can vary based on the lender’s efficiency, the complexity of your financial situation, and external factors such as market demand and legal considerations.

Learn more about Staten Island.