The VA Interest Rate Reduction Refinance Loan (IRRRL) continues to be one of the strongest financial tools available to veterans and service members who already hold a VA-backed mortgage. Designed with clarity, speed, and borrower protection at its core, the IRRRL offers a path to improve loan terms with fewer barriers, less complexity, and a highly predictable refinance experience. For many borrowers, this program provides an opportunity to secure lower monthly payments, transition into a more stable fixed-rate mortgage, or refine their existing loan structure without the stress of a traditional refinance.

Unlike conventional refinance programs, the IRRRL keeps the process streamlined by removing unnecessary requirements, limiting documentation, and focusing on one core goal: delivering measurable financial benefit to the borrower. For veterans looking to strengthen their long-term housing stability and optimize their mortgage performance, the IRRRL remains one of the most trusted and efficient refinance options available today.

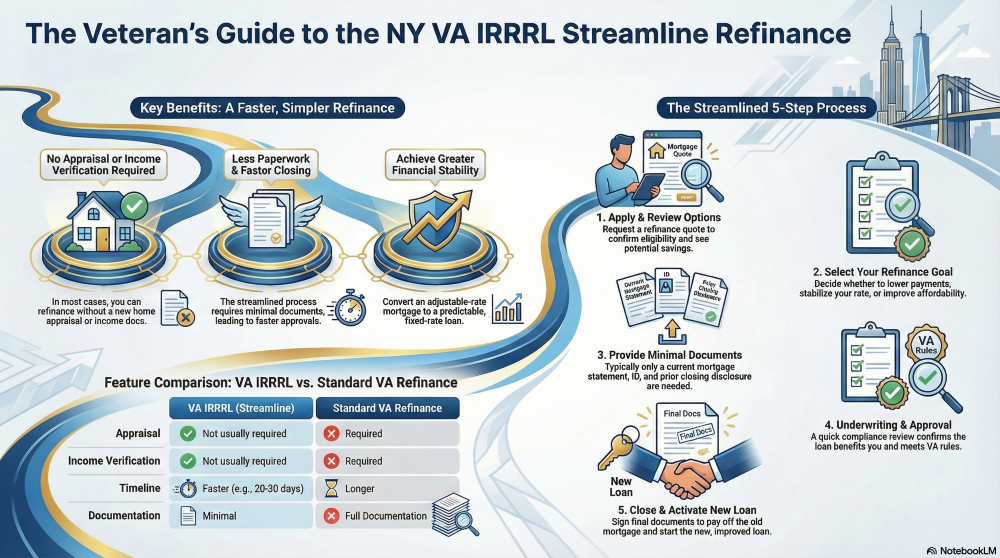

Why the VA IRRRL Remains One of the Most Valuable Mortgage Tools for Veterans

The VA IRRRL refinance program is built for simplicity and efficiency—two qualities that matter deeply to borrowers who want meaningful improvements without navigating a complex, time-consuming process. Its veteran-focused design ensures that borrowers experience a smooth, predictable refinance journey with fewer interruptions and faster results.

Key advantages that make the IRRRL stand out include:

- Access to lower interest rates when market conditions align

- A highly streamlined refinance structure requiring limited documentation

- No appraisal required in most cases, which can save time and reduce uncertainty

- A reduced funding fee compared to other VA refinances

- The ability to roll closing costs into the new loan

- A direct path to transition from an adjustable-rate mortgage into a stable fixed-rate loan

- No income verification requirements in many scenarios

- Exclusivity to existing VA borrowers, maintaining the benefit within the veteran community

For borrowers seeking confidence, simplicity, and long-term financial improvement, the IRRRL is one of the strongest VA refinance options available.

How the IRRRL Works: A Clear Look at the Structure Behind This Streamlined Refinance

The IRRRL is often described as a “streamline refinance” because the process is deliberately minimal. Instead of rebuilding the entire loan file or requiring extensive underwriting, the IRRRL focuses on replacing the existing VA loan with a more favorable structure—typically with a lower rate or more secure terms.

Borrowers often pursue an IRRRL when they want to:

- Capture savings through a lower interest rate

- Improve stability by moving out of an adjustable-rate mortgage

- Reduce their monthly mortgage payment

- Improve the predictability of long-term housing costs

- Complete a refinance quickly using the VA’s efficient approval framework

The IRRRL does not offer cash-out options. Instead, it specializes in strengthening loan performance—refining what already exists rather than restructuring everything from the ground up.

Essential VA IRRRL Guidelines: What Borrowers Should Understand Before Starting

The VA establishes clear guidelines to ensure the refinance improves the borrower’s financial position while protecting long-term outcomes. These rules help borrowers move forward with confidence and clarity.

Key guidelines for 2026 include the following:

A Verified Net Tangible Benefit (NTB) Requirement

Borrowers must experience a measurable benefit from refinancing. This may include:

- A lower interest rate

- A reduction in monthly mortgage payment

- A transition to a fixed-rate loan for improved stability

- A more affordable or predictable loan structure

This requirement ensures that every IRRRL refinance genuinely supports the borrower’s financial interests.

Seasoning Requirements for Consumer Protection

To qualify, borrowers must meet two conditions:

- At least 210 days must pass from the due date of the first payment on the original VA mortgage.

- Borrowers must complete six consecutive on-time monthly payments.

These safeguards reinforce responsible lending and create a stable refinance timeline.

Reduced IRRRL Funding Fee

A reduced VA funding fee may apply to an IRRRL refinance. Some borrowers may qualify for a full exemption based on service-connected disability or other VA eligibility guidelines.

Occupancy Confirmation

Borrowers do not need to currently live in the property. They must only confirm that they previously occupied it as their primary residence.

Program Limitations That Protect Borrowers

- No cash-out is permitted

- Closing costs may be financed into the loan

- The refinance must meet new VA fee and cost rules

These program boundaries help maintain the IRRRL’s focus as a benefit-driven refinance option.

Documentation Borrowers May Need for an IRRRL Refinance

Part of what makes the IRRRL so appealing is the reduced documentation requirement. However, lenders must still gather enough information to verify eligibility and demonstrate a clear borrower benefit.

Borrowers may be asked for:

- Most recent mortgage statement

- Payment history for the existing VA loan

- Government-issued identification

- Existing loan note or payoff request

- Certificate of Eligibility (only if lender needs revalidation)

- Signed disclosures and authorization forms

One of the major advantages is that many borrowers complete the refinance with no income verification and no employment documentation—a feature unique to IRRRL refinances.

A Step-by-Step Guide to the IRRRL Process: What Borrowers Can Expect from Start to Finish

A streamlined refinance only works when the process is clear, structured, and predictable. The IRRRL is built around efficiency, and most borrowers move through the process with ease.

Typical steps include:

- Requesting a VA loan refinance quote

- Verifying eligibility and meeting seasoning requirements

- Reviewing loan projections, estimated savings, and closing cost options

- Providing required documentation and signing initial disclosures

- Lender review to verify net tangible benefit

- Limited underwriting process to confirm alignment with VA guidelines

- Preparation of final closing documents

- Closing on the new loan and funding the refinance

Because the IRRRL avoids full underwriting, credit overlays, and in many cases property valuation, borrowers often describe the experience as one of the fastest refinance programs available.

How Long Does an IRRRL Take? Updated Timelines for 2026

With fewer requirements and a streamlined approval structure, the IRRRL typically closes far faster than other refinance programs. Most refinances finalize within:

- 10 to 30 days on average

- Quicker timelines when borrowers submit all requested documents up front

- Slight delays only when servicer verification or administrative processing is required

For borrowers watching the market or considering a rate improvement, this efficiency can make a significant financial difference.

Why Veterans Continue to Choose the IRRRL: Long-Term Value and Everyday Savings

The IRRRL remains one of the most widely used VA refinance tools for several compelling reasons. Veterans consistently highlight benefits such as:

- Lower monthly payments made possible through reduced interest rates

- Greater predictability by transitioning away from adjustable-rate structures

- Access to a program specifically designed for military borrowers

- A simplified refinance experience that respects time and personal circumstances

- A more stable long-term financial profile

The IRRRL’s credibility comes from decades of consistent performance, making it a reliable option for veterans seeking financial strength and loan stability.

IRRRL vs. VA Cash-Out Refinance: Understanding Which Option Aligns With Your Goals

Understanding the difference between a VA IRRRL and a VA cash-out refinance helps borrowers select the right financial path.

| Feature | VA IRRRL | VA Cash-Out Refinance |

| Purpose | Rate or payment reduction | Access home equity |

| Appraisal Required? | Often no | Yes |

| Income Verification | Usually not required | Required |

| Cash Back Allowed? | No | Yes |

| Funding Fee | Reduced VA funding fee | Standard VA funding fee |

| Best For | Improved terms and stability | Equity utilization |

Borrowers looking for improved monthly affordability should consider the IRRRL, while those seeking liquidity may prefer a cash-out refinance.

How an IRRRL Could Impact Monthly Mortgage Costs

The example below shows how the IRRRL may lower monthly payments through a reduced interest rate. These numbers are hypothetical and for illustrative purposes only, not actual market rates.

Rates, APRs, and payments are subject to change without notice.

| Mortgage Type | Example Rate / APR | Estimated Monthly Payment (P&I) | Disclaimer |

| Current VA Loan | 6.50% / 6.60% APR | $1,580 | Hypothetical only |

| IRRRL Example | 5.25% / 5.35% APR | $1,368 | Hypothetical only |

Estimated savings: approximately $212 per month (not guaranteed)

Actual savings vary based on loan amount, credit, market conditions, and individual eligibility.

Who Qualifies for the IRRRL? What Borrowers Should Confirm Before Applying

Most borrowers who already have a VA-backed mortgage will qualify if they meet a few essential criteria:

- The refinance must demonstrate a net tangible benefit

- The existing loan must meet seasoning requirements

- Borrowers must verify prior occupancy

- The refinance must meet VA cost and fee guidelines

VA borrowers seeking a simpler, more efficient refinance often find the IRRRL to be a strong fit.

Essential VA IRRRL Insights Every Borrower Should Know

- The IRRRL offers VA borrowers a streamlined path to lower payments, reduced interest rates, and enhanced loan stability.

- Most borrowers benefit from a simplified approval process requiring fewer documents and no appraisal.

- The program remains one of the most trusted refinance solutions for veterans seeking long-term financial improvement.

- Borrowers can finance closing costs into the new loan and access competitive terms through a VA-approved lender.

- Jet Direct Mortgage provides borrowers with personalized support, clarity, and guidance throughout the IRRRL process.

Get a VA IRRRL Refinance Quote From Jet Direct Mortgage

For expert guidance, personalized quotes, or assistance beginning your IRRRL refinance:

Jet Direct Mortgage

Website: Jetdirectmortgage.com

Phone: +1.800.700.4JET

Email: express@jetdirectmortgage.com

Address: 4875 Sunrise Hwy, Suite 300, Bohemia, New York 11716

NMLS: 3542

Related Mortgage Resources

- VA Home Loans

- FHA Loans

- Jumbo Loans

- USDA Loans

- Renovation Loans

- First-Time Homebuyer Programs

FAQs

What is a VA streamline refinance?

A VA streamline refinance, also known as an IRRRL, is a simplified refinance option designed to help borrowers lower their interest rate, reduce monthly payments, or transition to a fixed-rate mortgage. It requires limited documentation and typically does not require an appraisal.

Does an IRRRL require an appraisal?

Most IRRRL refinances do not require an appraisal, though lenders may request one under specific circumstances.

How long does an IRRRL take to close?

Most refinances are completed within 10 to 30 days, depending on lender workflow and borrower readiness.

Can borrowers take cash out with an IRRRL?

No. The IRRRL does not allow cash-out; its purpose is rate and payment improvement only.

Are there closing costs for an IRRRL?

Yes. Borrowers may roll closing costs into the new loan, and a reduced VA funding fee may apply to IRRRL refinances. Certain borrowers, including those with qualifying service-connected disabilities, may be exempt under VA guidelines.

Jet Direct Mortgage Licensing Disclaimer

NMLS: 3542

Jet Direct Mortgage © 2025. All Rights Reserved. Alabama Consumer Credit License – License/Registration #22632; Arizona Mortgage Banker License – Lic/Reg#:1040763; Licensed by the Department of Financial Protection and Innovation under the California Residential Mortgage Lending Act – #41DBO-81230; Colorado Mortgage Company Registration #LMB100014791; Connecticut Mortgage Lender License #20333; Delaware Lender License – License/Registration #032943; Florida Mortgage Lender Servicer License #MLD357; Licensed by the Georgia Department of Banking and Finance Company License Company – License #64345; Illinois Residential Mortgage License – Lic/Reg#:MB.6850070; Indiana DFI Mortgage Lending License No. 59981; Maine Supervised Lender License No. SLM9525; Maryland Mortgage Lender License #17365; MA Mortgage Lender License #ML3542; Michigan 1st Mortgage Broker/Lender/Servicer Registrant #FL10015703; Licensed Residential Mortgage Lender NJ Dept of Banking & Insurance #3542; New Mexico Mortgage Loan Company License 3542; Licensed Mortgage Banker NYS Department of Financial Services #B500903 – NMLS#3542; North Carolina Mortgage Lender License L-180193; Ohio Mortgage Broker Act Mortgage Banker Exemption # MBMB.850088.000; Oregon: State of Oregon ML-3542; Pennsylvania Mortgage Lender License No. 47421; South Carolina-BFI Mortgage Lender / Servicer License MLS–3542; Tennessee Mortgage License – License/Registration #17365; Texas – SML Mortgage Banker Registration; Virginia License/Registration # MC-4985; Washington Department of Financial Institutions, Consumer Loan Company License CL-3542; Wisconsin – Mortgage Banker License, #ML3542;

Experienced Chief Operating Officer with a 26 + year demonstrated history of working in the banking industry. Skilled in all aspects of the residential mortgage market . Strong business development professional with a Bachelor of Science (BS) focused in Business Administration and Management, from St. Joseph College. A direct endorsement underwriter and a licensed Mortgage Loan Originator.