The Federal Reserve (the Fed) meets this week, and most experts expect them to cut the Federal Funds Rate. But before you assume that means mortgage rates will fall, let’s break down how this really works.

The Fed Doesn’t Directly Set Mortgage Rates

The Federal Funds Rate is the short-term interest rate banks charge one another. While it influences borrowing costs across the economy, it is not the same thing as mortgage rates. Still, the Fed’s actions can set the tone for where mortgage rates may go next.

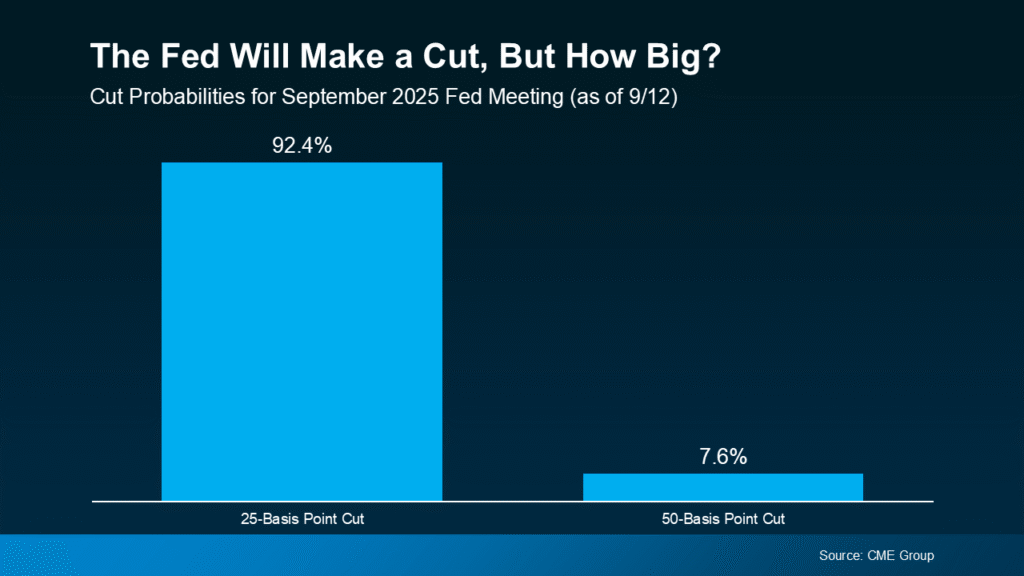

According to the CME FedWatch Tool, markets see nearly a 100% chance of a September rate cut. Most expect a modest 25-basis point move, though there’s a small chance the Fed could go bigger with a 50-basis point cut.

Why Mortgage Rates May Not React Immediately

Here’s the catch: mortgage rates usually move ahead of the Fed. That’s because they react to what markets expect will happen, not just to the official announcement.

For example, after weaker-than-expected job reports on August 1 and September 5, mortgage rates ticked lower because markets grew more confident a cut was on the way. Even a recent bump in inflation hasn’t changed that outlook.

So, if the Fed delivers the expected 25-basis point cut, mortgage rates may not shift much since that’s already priced in. However, if the Fed surprises with a larger 50-basis point cut, mortgage rates could ease further.

What’s Next for Mortgage Rates?

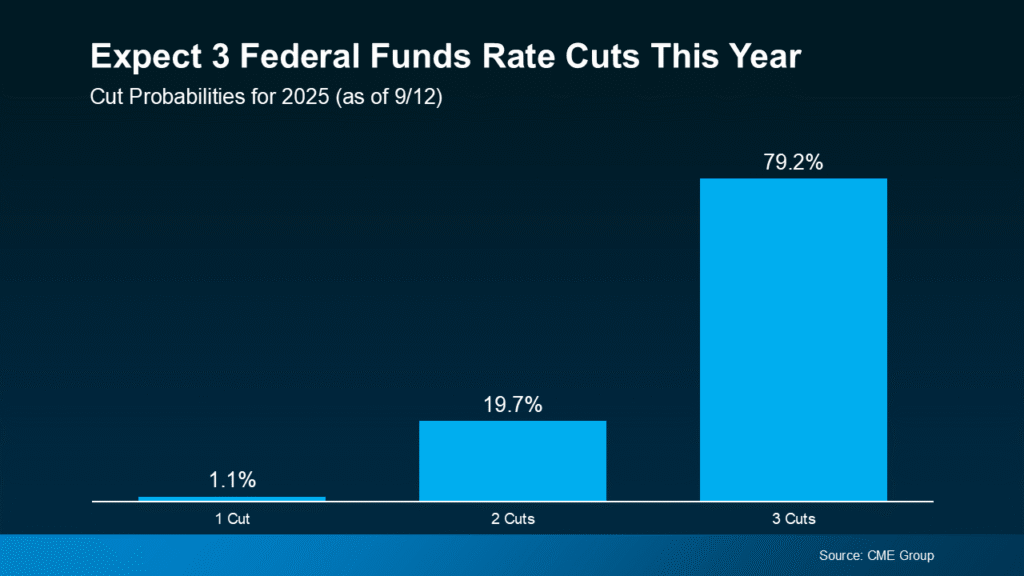

One rate cut alone may not dramatically change the housing market. But many economists think this could be the start of a series of cuts if the economy continues to cool.

Sam Williamson, Senior Economist at First American, explains:

“For mortgage rates, investor confidence in a forthcoming rate-cutting cycle could help push borrowing costs lower in the back half of 2025, offering some relief to housing affordability and potentially helping to boost buyer demand and overall market activity.”

If markets believe more cuts are coming—or if they actually happen—mortgage rates could trend lower over the next several months. Still, much depends on how the economy performs. Unexpected inflation data or shifts in growth could quickly change the picture.

The Bottom Line

Mortgage rates won’t fall overnight, and they won’t match the Fed’s cuts point-for-point. But if the Fed starts a broader cycle of rate reductions and markets remain confident, rates could gradually move lower later this year and into 2026.

If you’ve been waiting on the sidelines, this is a smart time to start planning. Even a small drop in rates can make a big difference in affordability. Talking through your options now ensures you’re ready to act when the right opportunity comes along.

Source: Keeping Current Matters

Experienced Chief Operating Officer with a 26 + year demonstrated history of working in the banking industry. Skilled in all aspects of the residential mortgage market . Strong business development professional with a Bachelor of Science (BS) focused in Business Administration and Management, from St. Joseph College. A direct endorsement underwriter and a licensed Mortgage Loan Originator.