Landing a home purchase or refinance in New York when your credit report looks bruised can feel like hailing a cab in a snowstorm—every lender seems to glide past. Yet thousands of New Yorkers close every year with scores in the 500s and recent credit dings. This guide is for first-time buyers, owners eager to refinance, and anyone comparing lenders who fear a low score will slam every door. You’ll see how underwriters actually judge risk, which programs welcome imperfect credit, and what concrete steps move you from “maybe” to “approved.”

2. Why “Bad Credit” Isn’t a Deal-Breaker in New York

How Credit Scores Affect Offers

| Credit-Score Band | Typical NY Loan Paths | **Estimated Rate Premium *** | Approval Keys |

| 760 + | Conventional (Conforming) | baseline (prime) | Automated approval, best pricing |

| 700–759 | Conventional, High-balance | +0.25 – 0.50 pp | Solid DTI, steady employment |

| 660–699 | Conventional (manual), FHA | +0.50 – 1.00 pp | Compensating factors, reserves |

| 620–659 | FHA, VA | +1.00 – 1.75 pp | Lower debt ratios, full docs |

| 580–619 | FHA (manual) | +1.75 – 3.00 pp | Larger reserves, limited credit events |

| 500–579 | FHA (rare), True Sub-prime | case-by-case | Significant compensating factors |

* Versus a prime conforming 30-year fixed; pricing shifts daily.

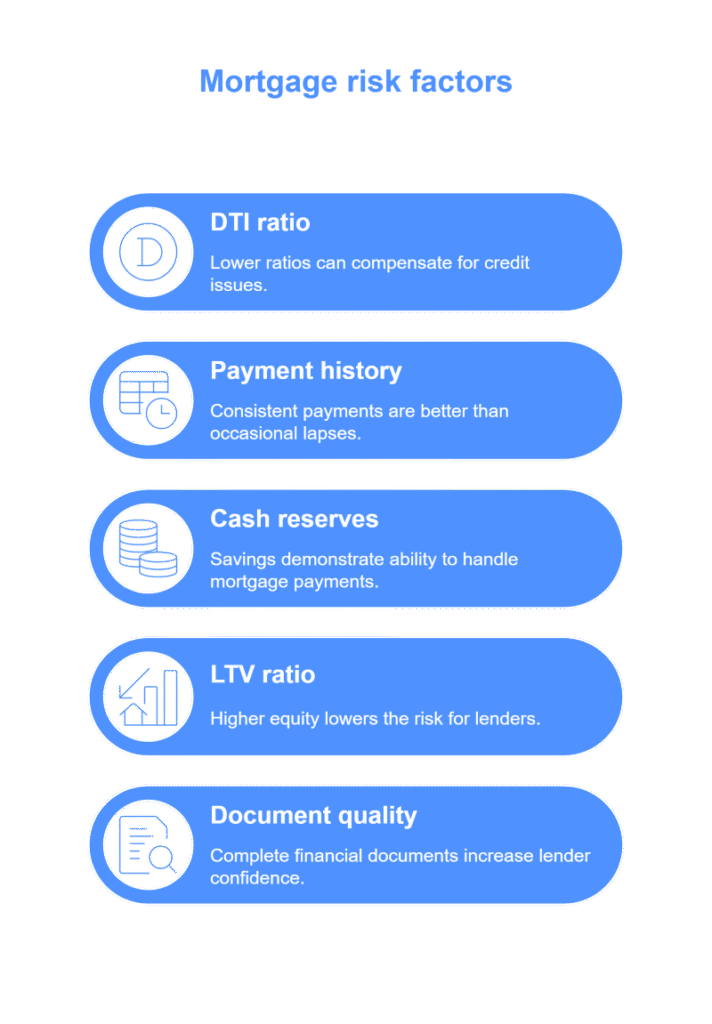

Why Lenders Look Beyond the Score

Lenders weigh several variables in tandem:

- Debt-to-Income (DTI) ratio – lower ratios offset weaker credit.

- Payment-history patterns – isolated medical collections weigh less than repeated late housing payments.

- Cash reserves – several months of principal & interest on hand shows staying power.

- Loan-to-Value (LTV) ratio – more equity reduces lender exposure.

- Document quality – full tax returns, W-2s, or profit-and-loss statements tighten underwriting confidence.

3. Loan Options for Credit-Challenged Borrowers

Below are the core paths New Yorkers rely on when scores fall under roughly 660. Each carries its own eligibility rules, strengths, and cautions.

3.1 FHA Loans

Backed by the Federal Housing Administration, FHA loans dominate New York’s bad-credit landscape because the program officially permits scores as low as 580—and in rare cases 500–579 with strong compensating factors.

Advantages

- More forgiving credit guidelines than conventional loans.

- Past bankruptcy or foreclosure often acceptable once waiting periods expire.

- Streamline refinance available later with minimal documentation.

Watch-Outs

- Up-front and annual mortgage-insurance premiums raise total borrowing cost.

- Properties must meet FHA appraisal standards—stricter on fixer-uppers.

3.2 VA & USDA Loans (If Eligible)

Though designed for veterans and rural buyers, these programs frequently approve scores in the low 600s—and sometimes lower—because a federal guarantee absorbs much of the risk.

Who Qualifies

- VA: Active-duty, certain reservists, veterans, and eligible surviving spouses.

- USDA: Primary residences in USDA-approved rural zones plus income under county caps.

Benefits

- Credit overlays often accept 580–620.

- Interest rates usually beat comparable conventional offers.

- Lower fee structure than typical sub-prime products.

4. Specialized New York Programs for Credit Challenges

New York supplements federal products with state and municipal solutions that can bridge affordability gaps.

4.1 SONYMA “Achieving the Dream”

The State of New York Mortgage Agency targets first-time buyers who meet moderate-income limits.

Key Points

- Usually requires a 620 minimum score (some lenders may dip lower with manual underwriting).

- Must occupy the home as a primary residence and meet SONYMA price caps.

- Below-market interest rates and capped lender fees help offset credit premiums.

4.2 Neighborhood & Municipal Grants

City-specific grants—such as NYC’s HomeFirst or Rochester’s Home Purchase Assistance Program—cover select closing costs for buyers with scores in the 580–640 band. Most require a multi-year owner-occupancy pledge.

4.3 Community Development Financial Institutions (CDFIs)

Mission-driven lenders like LISC create portfolio products that tolerate thin files or recent credit score drops, pairing financing with HUD-certified counseling and budgeting classes.

5. Refinance & Cash-Out Paths for Low-Score Homeowners

5.1 FHA Streamline Refinance

If you already hold an FHA loan, the streamline option can cut rates or shorten terms without a new appraisal or income verification—as long as the refinance yields a “net tangible benefit.”

5.2 Credit-Union or Portfolio Alternatives

Select credit unions and regional banks will consider limited cash-out requests for scores below 640, provided you’ve shown 12–24 consecutive on-time mortgage payments and hold meaningful equity.

6. Preparing a Strong Application

6.1 Credit Repair vs. Rapid Rescore

- Traditional repair (disputing errors, negotiating collections) may raise scores 20-40 points over several months.

- Rapid rescore tools—available through many lenders—update balances and deletions in days instead of months.

6.2 Boosting Compensating Factors

| Factor | Typical Threshold | How It Lowers Perceived Risk |

| Debt-to-Income ratio | ≤ 40 % | Shows capacity to absorb new payments |

| Cash reserves | 3–6 months of P&I | Provides cushion against income shocks |

| Job tenure | ≥ 2 years in same field | Signals steady earnings potential |

| Co-borrower credit | ≥ 700 | Blends overall file for stronger decision |

| Verified rent history | 12 on-time payments | Demonstrates payment reliability |

6.3 Document Checklist

Have these ready before contacting a lender:

- Two years of W-2s or 1099s (self-employed add P&L and balance sheet).

- Most recent two months of bank/asset statements.

- Government-issued ID and Social Security verification.

- Letter of explanation for any recent late payments or major credit events.

7. Current NY Rate & Fee Expectations (Credit < 660)

Bad-credit mortgage rates in New York typically sit 1.0–2.5 percentage points above prime conforming quotes. Expect:

- Rate locks of 30–60 days; longer locks cost extra.

- Discount points: Paying one point can shave roughly 0.25–0.375 percentage points off the note rate; calculate breakeven near the five-year mark.

- Third-party fees: Appraisals, attorney review, and title insurance vary; shop bundled packages when possible.

8. Comparing Lenders: Big Banks vs. Local Specialists

| Feature | Big Bank | Credit Union | Jet Direct Mortgage |

| Minimum score | 620–640 | 600–620 | As low as 580 on select products |

| Underwriting style | Algorithmic | Manual | Hybrid—local manual overrides |

| Turn-time to close | 45–60 days | 30–45 days | ≈ 21–30 days |

| Program variety | Limited | Moderate | FHA, VA, SONYMA, CDFI partnerships |

| Personalized guidance | Low | Medium | High—dedicated NY bad-credit team |

9. Step-by-Step Loan Timeline in New York

- Pre-approval (Day 1-2) – Soft credit pull, scenario review, tentative rate quote.

- Contract accepted (Week 1) – Full disclosures; appraisal ordered.

- Processing (Weeks 2-3) – Verify income/assets; clear credit conditions.

- Underwriting decision (Week 3) – Conditional approval; gather trailing docs.

- Commitment & clear-to-close (Week 4) – Attorneys receive package; title clears.

- Closing (Week 4-5) – Sign documents, funding, county-clerk recording.

10. Common Pitfalls & How to Avoid Them

- Opening new credit lines during the mortgage process.

- Leaving credit disputes open—many automated systems require them removed first.

- Paying excessive “junk” fees disguised as processing or application charges—demand a Loan Estimate up front and compare.

11. Frequently Asked Questions

| Question | Quick Answer |

| 1. What is the minimum credit score for an FHA loan in New York? | Most lenders set 580 as the floor; a few will review 500–579 if you have strong compensating factors and a low DTI. |

| 2. Can I buy a multifamily property with bad credit? | Yes. FHA and some portfolio lenders finance two- to four-unit homes with scores in the 600s, provided rental income supports the payment and you occupy one unit. |

| 3. How long after bankruptcy can I buy a home? | FHA and VA require two years after Chapter 7 discharge; many portfolio lenders look for at least 24 months of re-established credit. |

| 4. Are “credit-repair” companies worth it? | Sometimes. If your report contains genuine errors, a reputable firm can speed up corrections; disputing legitimate debts often backfires. |

| 5. Can I combine SONYMA assistance with an FHA loan? | Yes. SONYMA frequently allows its closing-cost support programs to pair with FHA financing. |

| 6. Will paying discount points help if I have a low score? | Often, yes—buying points lowers the lender’s long-term risk and can offset credit-related pricing add-ons. |

| 7. How soon after a foreclosure can I buy again in NY? | FHA = 3 years, VA = 2 years, conventional = 7 years. Some portfolio lenders may review files sooner if you hold strong reserves and stable income. |

| 8. Do lenders verify rent if I pay cash each month? | Yes—provide 12 months of canceled checks or a notarized letter from your landlord plus bank statements showing corresponding withdrawals. |

| 9. Will refinancing reset my property-tax assessment? | No. Refinancing does not trigger reassessment in New York; taxes continue on the existing valuation schedule. |

12. Conclusion & Next Steps

Bad credit doesn’t have to sideline your homeownership or refinance goals. New Yorkers succeed every day by pairing flexible federal programs with state resources such as SONYMA and city-level grants, then bolstering applications with compensating factors. Compare quotes across multiple lender types, gather solid documentation, and lean on a specialist who understands New York underwriting nuances.

Ready to turn credit challenges into keys?

Contact Jet Direct Mortgage for a personalized game plan:

• Call +1-800-700-4JET

• Email express@jetdirectmortgage.com

• Visit 4875 Sunrise Hwy, Suite 300, Bohemia, NY 11716

• Start your secure application at JetDirectMortgage.com

This guide is for informational purposes and should not be considered financial advice. Always consult a licensed mortgage professional about your specific circumstances.

Experienced Chief Operating Officer with a 26 + year demonstrated history of working in the banking industry. Skilled in all aspects of the residential mortgage market . Strong business development professional with a Bachelor of Science (BS) focused in Business Administration and Management, from St. Joseph College. A direct endorsement underwriter and a licensed Mortgage Loan Originator.