Getting approved for a mortgage in New York is often easier than it seems.

You may think that you need a perfect credit score or a six-figure income before you can qualify for a mortgage. While strong finances can certainly help, mortgage approval is usually less about perfection and more about preparation.

The reality is that lenders want to see that you can comfortably manage the responsibilities of homeownership. Your income, credit history, savings, debt levels, and employment situation all play a role, but no single factor determines whether you’ll be approved.

That’s why understanding how to get approved for a mortgage in New York before you start house hunting can save you time, reduce stress, and help you avoid costly mistakes.

Many buyers don’t begin thinking about mortgage approval until they’ve already found a home they want to purchase. Unfortunately, that’s often when financing issues, missing documents, or credit concerns become urgent problems instead of manageable tasks.

A better approach is to prepare in advance. Whether you’re buying your first home on Long Island, purchasing a condo in New York City or relocating elsewhere in the state, taking the right steps early can significantly improve your chances of approval.

In this guide, we’ll walk through the five key steps that can help you get approved for a mortgage in New York, strengthen your application, and put yourself in the best possible position before you submit an offer on a home.

The good news is that most mortgage approval challenges can be addressed with enough planning. By understanding what lenders look for and taking action before you apply, you’ll be able to move through the process with greater confidence and clarity.

Our team at Jet Direct Mortgage has prepared a guide with all the steps you need to take in order to get approved, so let’s get into it:

Step #1: Know Where You Stand Financially Before Applying

If you’re trying to get approved for a mortgage in New York, the first step isn’t contacting lenders or browsing real estate listings. It’s understanding your financial position.

Many buyers start house hunting before they know whether they’re financially ready to purchase a home. As a result, they often waste time looking at properties that don’t fit their budget or discover financing issues at the worst possible moment.

Before applying for a mortgage, take time to evaluate four key areas:

- Your credit profile

- Your income

- Your savings

- Your existing debt

These factors will heavily influence the loan programs available to you and how much you may be able to borrow.

1.1. Review Your Credit Profile

Your credit score isn’t the only factor lenders consider, but it plays an important role in the mortgage approval process.

A stronger credit profile may provide access to:

- More loan options

- Lower down payment requirements

- Better interest rates

- More favorable loan terms

Before applying, review your credit reports carefully and look for:

- Incorrect account information

- Late payments reported in error

- Accounts that don’t belong to you

- High credit card balances

Addressing these issues early can help strengthen your mortgage application before lenders begin reviewing it, and help you get approved for a mortgage in New York.

1.2. Understand Your Monthly Budget

One of the biggest mistakes homebuyers make is focusing solely on the maximum amount they can borrow. Instead, focus on what payment fits comfortably within your lifestyle.

Ask yourself:

- How much can I comfortably spend on housing each month?

- Will I still be able to save money?

- Can I handle unexpected expenses?

- How will this payment affect my other financial goals?

Remember that homeownership involves more than just the mortgage payment. Property taxes, homeowners insurance, maintenance, utilities, and repairs all contribute to the true cost of owning a home.

1.3. Evaluate Your Savings

When people think about mortgage approval, they often focus entirely on the down payment. However, lenders may also want to see that you have sufficient funds available for:

- Closing costs

- Moving expenses

- Cash reserves

- Unexpected homeownership expenses

Having savings after closing can make you a stronger borrower and help you avoid financial stress during your first months as a homeowner.

1.4. Take a Close Look at Your Existing Debt

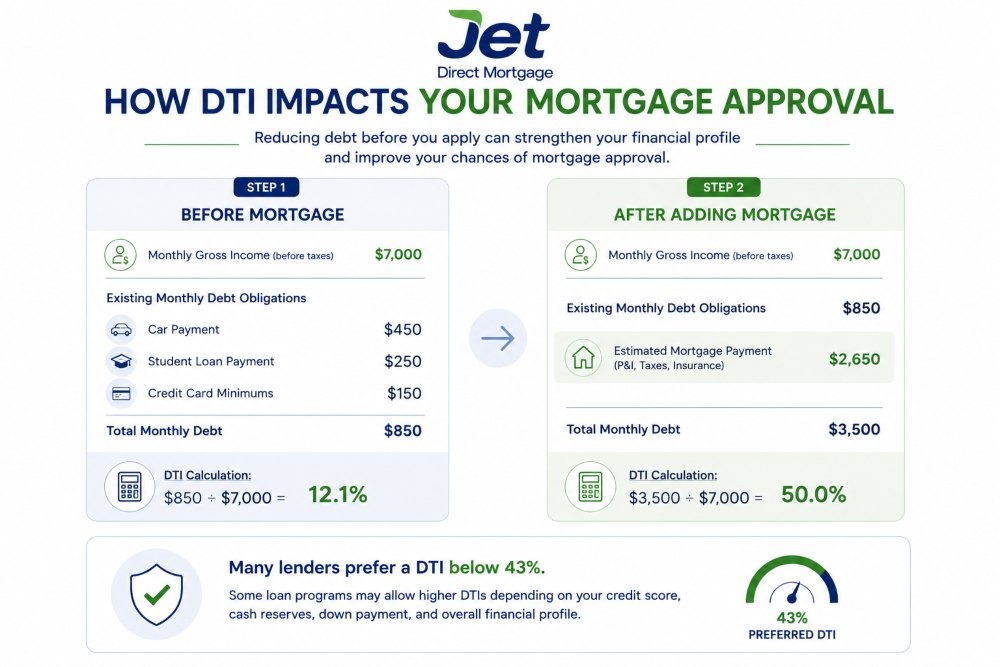

Lenders evaluate how much debt you currently have compared to your income.This is commonly referred to as your debt-to-income ratio (DTI). Common debts include:

- Student loans

- Auto loans

- Credit cards

- Personal loans

- Child support obligations

Reducing existing debt before applying can strengthen your financial profile and improve your chances of mortgage approval. For example, let’s say that you earn $7,000 per month before taxes, and you currently have a $450 car payment, $250 student loan payment, and $150 minimum credit card payments.

That’s already $850 in monthly debt obligations before adding a mortgage payment, which gives you a DTI of approximately 12.1% ($850 ÷ $7,000).

Now imagine your future mortgage payment, including principal, interest, property taxes, and homeowners insurance, is estimated at $2,650 per month. Your total monthly debt obligations would increase to $3,500, resulting in a DTI of 50% ($3,500 ÷ $7,000).

Many lenders prefer to see a debt-to-income ratio below 43%, although some loan programs may allow higher DTIs depending on factors such as your credit score, cash reserves, down payment, and overall financial profile.

In general, a lower DTI can improve your approval odds and may provide access to more favorable financing options when it comes to getting approved for a mortgage in New York.

1.5. Mortgage Readiness Checklist

Before moving to the next step, ask yourself:

- Have I reviewed my credit?

- Do I understand my monthly budget?

- Do I have savings for both the down payment and closing costs?

- Do I have cash reserves after closing?

- Have I evaluated my existing debt obligations?

The clearer your financial picture, the easier it will be to get approved for a mortgage in New York and move through the process with confidence. Understanding where you stand today will help you identify any areas that need improvement before you submit your application.

Step #2: Strengthen Your Mortgage Profile Before You Apply

Once you understand where you stand financially, the next step is improving the areas that lenders pay the most attention to. Many buyers assume mortgage approval is determined by a single factor, such as their credit score or income. In reality, lenders evaluate your overall financial profile.

Small improvements made a few months before applying can sometimes have a meaningful impact on your financing options.

If your goal is to get approved for a mortgage in New York, focus on strengthening the parts of your application that are within your control.

2.1. Pay Down Credit Card Balances

One of the fastest ways to improve your mortgage profile is reducing credit card debt. Even if you make all your payments on time, carrying high balances can increase your credit utilization ratio and affect your credit score.

For example, if your credit card limit is $10,000 and your balance is $8,000, you’re using 80% of your available credit. Many lenders prefer to see significantly lower utilization levels because they indicate less financial stress and lower borrowing risk.

2.2. Avoid Applying for New Credit

When you’re preparing to apply for a mortgage, this is not the ideal time to:

- Open new credit cards

- Finance furniture

- Take out a personal loan

- Lease a vehicle

- Apply for multiple financing products

Every new debt obligation can affect your debt-to-income ratio and potentially impact your mortgage approval. Even if you’re approved, new debt can reduce the amount you’re able to borrow for a home.

2.3. Organize Your Financial Documents Early

Many buyers underestimate how much documentation is required during the mortgage process. Gathering these documents in advance can make the process significantly smoother. Common documents include:

- Recent pay stubs

- W-2 forms

- Tax returns

- Bank statements

- Investment account statements

- Identification documents

Having everything organized before you apply can help avoid delays later.

2.4. Keep Your Employment Stable

Lenders value consistency. A job change doesn’t automatically prevent you from getting approved, but changing employers, industries, or compensation structures shortly before applying can create additional questions during the underwriting process.

If possible, avoid making major employment changes while preparing for a mortgage application.

2.5. Simple Actions That Can Improve Your Mortgage Readiness

| Action | Potential Impact | Difficulty |

| Pay down credit card balances | Can improve credit profile and DTI | Medium |

| Make all payments on time | Helps build a strong payment history | Easy |

| Avoid opening new credit accounts | Prevents unnecessary changes to your profile | Easy |

| Reduce existing debt | May improve borrowing capacity | Medium |

| Organize financial documents | Helps speed up the approval process | Easy |

| Maintain stable employment | Creates a more consistent application | Easy |

You don’t need perfect finances to get approved for a mortgage in New York. Most successful borrowers simply take time to prepare before applying.

Paying down debt, avoiding unnecessary financial changes, and organizing your documentation can put you in a much stronger position when lenders begin reviewing your application.

The goal isn’t to create the perfect mortgage profile. The goal is to present the strongest and most accurate financial picture possible before moving on to the next step: choosing the right loan program.

Step #3: Choose the Right Loan Program

Many buyers assume that getting approved for a mortgage is simply a matter of finding a lender and submitting an application. In reality, choosing the right loan program can be just as important as choosing the right lender.

Different mortgage programs have different requirements for:

- Credit scores

- Down payments

- Debt-to-income ratios

- Cash reserves

- Property types

As a result, a buyer who doesn’t qualify for one program may be approved through another. That’s why understanding your options is an important step if you’re trying to get approved for a mortgage in New York.

3.1. Conventional Loans

Conventional loans are among the most popular mortgage options for homebuyers in New York. They typically work best for borrowers with stable income, strong credit, and a solid financial profile.

One of the biggest advantages of a conventional loan is flexibility. These loans can be used for primary residences, second homes, and investment properties, and private mortgage insurance (PMI) can often be removed once sufficient equity is built.

3.2. FHA Loans

FHA loans are designed to make homeownership more accessible, particularly for buyers who may have limited savings or less-than-perfect credit.

Because these loans are insured by the Federal Housing Administration, lenders can often offer more flexible qualification requirements than some conventional mortgage programs. FHA loans remain especially popular among first-time homebuyers.

3.3. VA Loans

VA loans provide valuable financing benefits for eligible veterans, active-duty service members, and certain surviving spouses.

One of the most attractive features of a VA loan is that eligible borrowers may be able to purchase a home without a down payment while also avoiding monthly mortgage insurance requirements.

If you are looking to get approved for a mortgage in New York as a military family, this can be one of the most affordable paths to homeownership.

3.4. Jumbo Loans

Home prices in many New York markets exceed conventional loan limits, which is where jumbo loans become important.

Jumbo financing is designed for higher-priced properties that require larger loan amounts than standard conforming mortgages allow. These loans can help buyers finance homes in competitive and high-cost areas throughout New York.

3.5. First-Time Homebuyer Programs

Many buyers assume they need years of savings before they can purchase a home.

First-time homebuyer programs are designed to help make homeownership more accessible through specialized financing options, down payment assistance opportunities, and programs tailored to new buyers. Exploring these options early may open doors you didn’t realize were available.

3.6. Refinancing Options

Although refinancing isn’t used to purchase a home, it’s worth understanding how refinancing may fit into your long-term homeownership strategy.

Refinancing can help homeowners lower monthly payments, change loan terms, or access home equity as their financial situation evolves. Many buyers appreciate knowing these options exist before they commit to a mortgage.

Step #4: Get Pre-Approved Before You Start House Hunting

Many buyers begin their home search by browsing listings online. The smarter approach is to get pre-approved first. If you’re trying to get approved for a mortgage in New York, a pre-approval can help you understand exactly how much you may be able to borrow before you start touring homes.

This can save you time, prevent disappointment, and make the homebuying process significantly more efficient. Many buyers confuse pre-qualification and pre-approval, but they are not the same thing.

A pre-qualification is typically based on information you provide about your finances and can give you a rough estimate of your purchasing power.

A pre-approval involves a more detailed review of your financial profile, including documents such as pay stubs, tax returns, bank statements, employment information, and credit history. Because more information is verified, a pre-approval provides a much clearer picture of what you may qualify for.

4.1. Why Pre-Approval Matters

In competitive New York housing markets, sellers often receive multiple offers. When reviewing those offers, sellers don’t just look at the purchase price. They also want confidence that the buyer can secure financing and successfully reach the closing table.

A pre-approved buyer may appear more prepared and financially ready than someone who has not yet started the mortgage process.

Pre-approval can also help you avoid disappointment.

For example, you may believe you can comfortably afford a $750,000 home. After reviewing your income, debt, savings, and monthly obligations, you may discover that a lower price point creates a much healthier monthly budget.

It’s far better to learn this before falling in love with a property than after submitting an offer.

4.2. What You’ll Need

While requirements vary, most lenders will request:

- Government-issued identification

- Recent pay stubs

- W-2s or tax returns

- Bank statements

- Investment account statements

- Employment information

Having these documents ready can help speed up the process and reduce unnecessary delays. One of the most common mistakes buyers make is waiting until they’ve found the perfect home before speaking with a mortgage professional.

By then, time is often working against them.

If you’re serious about buying, obtaining a pre-approval is one of the most effective ways to get approved for a mortgage in New York and position yourself as a strong buyer when the right opportunity comes along.

Once you’re pre-approved, the final step is protecting that approval and avoiding mistakes that could create problems before closing.

Step #5: Avoid Common Mistakes That Can Delay or Derail Your Approval

Getting pre-approved is a major milestone, but it doesn’t mean the mortgage process is finished.

One of the most common misconceptions among homebuyers is that once they’re pre-approved, they can make major financial decisions without affecting their mortgage application.

In reality, lenders often continue reviewing your financial situation throughout the process and may verify certain information again before closing.

If you’re working to get approved for a mortgage in New York, it’s important to keep your finances as stable as possible until the transaction is complete.

5.1. Common Mistakes to Avoid

Some of the most common issues that can create problems during the mortgage process include:

- Opening new credit cards

- Financing a vehicle

- Taking out a personal loan

- Missing credit card or loan payments

- Making large unexplained bank deposits

- Changing jobs or income sources

- Increasing credit card balances significantly

Even actions that seem harmless can sometimes trigger additional reviews, documentation requests, or delays.

5.2. Financial Changes That Can Affect Approval

| Action | Potential Impact |

| Opening a new credit card | May affect your credit score and debt profile |

| Financing a car | Increases monthly debt obligations and DTI |

| Taking out a personal loan | Can reduce borrowing capacity |

| Missing a payment | May negatively affect your credit profile |

| Large unexplained deposits | May require additional documentation |

| Changing jobs | Can create additional underwriting requirements |

| Large credit card purchases | May increase credit utilization and debt |

The period between pre-approval and closing is not the ideal time to finance furniture, buy a new vehicle, switch careers, or make significant financial changes. The goal is simple: maintain the same financial profile that helped you qualify in the first place.

Many mortgage delays don’t happen because borrowers are unqualified. They happen because something changes during the process that requires additional review.

The smoother and more predictable your finances remain, the easier it is for lenders to finalize your loan.

If you’re trying to get approved for a mortgage in New York, consistency can be just as important as preparation. Once you’ve reached the finish line, avoid making changes that could move it farther away.

Conclusion

Getting approved for a mortgage isn’t about having perfect finances. It’s about preparation.

By understanding your financial situation, strengthening your mortgage profile, choosing the right loan program, obtaining a pre-approval, and avoiding common mistakes before closing, you can put yourself in a much stronger position to secure financing and move forward with confidence.

The good news is that most mortgage approval challenges can be identified and addressed before they become major obstacles.

Whether you’re purchasing your first home, upgrading to a larger property, or relocating within the state, taking these five steps can make the process smoother and significantly improve your chances of success.

If you’re looking to get approved for a mortgage in New York, working with an experienced mortgage professional can help you understand your options, prepare your application, and avoid costly mistakes along the way.

At Jet Direct Mortgage, we help homebuyers throughout New York navigate the mortgage process from pre-approval to closing. Our team can help you compare loan programs, evaluate financing options, and build a mortgage strategy that aligns with your goals.

Ready to take the next step? Contact us today.

Frequently Asked Questions

What credit score do I need to get approved for a mortgage in New York?

The minimum credit score depends on the loan program and lender. While higher credit scores often provide access to more favorable financing options, many borrowers can qualify with lower scores than they expect. The best way to understand your options is to review your specific financial situation with a mortgage professional.

Can I get approved for a mortgage with less than 20% down?

Yes. Many buyers purchase homes with significantly less than a 20% down payment. Depending on the loan program, eligible borrowers may qualify for low-down-payment financing options that require much less cash upfront.

How much income do I need to qualify for a mortgage?

There is no universal income requirement. Lenders evaluate your income alongside factors such as debt obligations, credit history, savings, and the size of the mortgage you’re requesting.

What documents do I need for mortgage approval?

While requirements vary, lenders commonly request:

- Government-issued identification

- Recent pay stubs

- W-2 forms or tax returns

- Bank statements

- Employment information

- Investment account statements (if applicable)

Having these documents organized early can help streamline the approval process.

How long does it take to get approved for a mortgage?

The timeline varies depending on the lender, loan program, and complexity of your financial situation. In many cases, buyers can obtain a pre-approval within a few days after providing the necessary documentation.

Can I get approved if I’m self-employed?

Yes. Self-employed borrowers can qualify for mortgages, although additional documentation may be required. Tax returns, business records, and proof of income are often important parts of the review process.

What is a debt-to-income ratio (DTI)?

Your debt-to-income ratio compares your monthly debt obligations to your gross monthly income. Lenders use DTI to evaluate your ability to manage mortgage payments alongside your existing debts.

What can hurt my mortgage approval after pre-approval?

Common issues include:

- Opening new credit accounts

- Financing a vehicle

- Taking out additional loans

- Missing payments

- Making large undocumented deposits

- Changing jobs or income sources

Keeping your finances stable until closing can help avoid unnecessary complications.

Should I get pre-approved before looking at homes?

Yes. Pre-approval can help you understand your budget, identify potential financing issues early, and strengthen your position when making an offer in a competitive market.

Can a mortgage broker help me get approved for a mortgage in New York?

A mortgage broker can help you compare loan options, understand lender requirements, prepare your application, and identify financing solutions that fit your situation. For many buyers, professional guidance can make the approval process significantly easier to navigate.

Experienced Chief Operating Officer with a 26 + year demonstrated history of working in the banking industry. Skilled in all aspects of the residential mortgage market . Strong business development professional with a Bachelor of Science (BS) focused in Business Administration and Management, from St. Joseph College. A direct endorsement underwriter and a licensed Mortgage Loan Originator.