Compare Today’s Mortgage Rates

Key Takeaways

- Mortgage rates today in Q1 2026 remain in the low-6% range for many 30-year fixed loans, though rates continue fluctuating daily. (Freddie Mac)

- Inflation, Treasury yields, and Federal Reserve expectations continue driving changes in current mortgage rates and refinancing costs across the U.S.

- Even small mortgage rate changes can significantly affect monthly payments, affordability, and long-term borrowing costs.

- National mortgage averages are benchmarks, not personalized quotes. Actual rates depend on credit score, down payment, loan type, and financial profile.

- New York borrowers still face affordability pressure due to elevated home prices and limited housing inventory.

- Refinancing may still benefit homeowners with higher existing rates, adjustable-rate mortgages, or long-term ownership plans.

- Pre-approval and personalized mortgage planning remain important as mortgage rates today continue evolving throughout 2026.

- Jet Direct Mortgage uses national mortgage data for educational purposes, but borrowers should rely on personalized quotes for accurate pricing.

Where Mortgage Rates Stand Right Now in Q1 2026

Recent reports from Freddie Mac, Mortgage News Daily, Realtor.com, and Yahoo Finance continue to show a similar trend across the housing market in Q1 2026.

While mortgage rates today remain elevated compared to the ultra-low rates seen in previous years, national averages have stabilized and continue moving within a relatively narrow range as inflation and Federal Reserve policy expectations evolve.

National Purchase-Mortgage Averages (Q1 2026)

| Loan Type | Average Rate* | One Week Ago | One Year Ago |

| 30-Year Fixed (FRM) | 6.34% | 6.29% | 6.71% |

| 15-Year Fixed (FRM) | 5.58% | 5.53% | 5.94% |

(Freddie Mac / National Average Estimates)

Refinance-Focused Snapshot (Q1 2026)

| Loan Purpose | Key Product | Approx. National Average* | Weekly Move |

| Refinance | 30-Year Fixed Refinance | ≈ 6.22% | +0.08 pts |

| Refinance | 15-Year Fixed Refinance | High-5% range | Slightly up |

(Yahoo Finance / Zillow Market Data)

Mortgage rates today continue to react to Treasury yields, inflation reports, employment data, and overall lending demand across the U.S. housing market.

Borrowers comparing loan options in Q1 2026 are still seeing meaningful differences between FHA, VA, conventional, and refinance products depending on credit profile, loan amount, and down payment structure.

Remember, these figures reflect national averages and rounded market estimates. Actual mortgage rates and loan pricing can vary based on your credit score, debt-to-income ratio, property type, occupancy, and overall financial profile.

Why Have Mortgage Rates Today Moved This Way in Q1 2026?

Several economic and market forces are continuing to shape mortgage rates today throughout Q1 2026.

While rates have improved from the peaks seen in previous years, ongoing inflation concerns, Treasury yield volatility, Federal Reserve policy expectations, and global economic uncertainty are still influencing mortgage pricing across the United States.

Treasury yields remain one of the biggest drivers of mortgage rates today.

The 10-year Treasury yield, widely considered the benchmark for long-term mortgage pricing, has continued fluctuating in Q1 2026 as investors react to inflation data, geopolitical uncertainty, and Federal Reserve guidance.

When Treasury yields rise, lenders typically increase mortgage rates to offset investor risk and market volatility. (Kiplinger)

Inflation continues to pressure mortgage markets in 2026

Even though inflation has cooled compared to previous years, markets remain sensitive to energy prices, labor market strength, and consumer spending trends.

Recent inflation reports pushed bond yields higher during Q1 2026, creating additional upward pressure on current mortgage rates today and refinancing activity. (Reuters)

Mortgage rates are still expected to remain above 6%

In addition, Freddie Mac and national housing analysts still expect mortgage rates today to remain above 6% through much of 2026.

According to market forecasts from Freddie Mac, Fannie Mae, Bankrate, and Yahoo Finance coverage, mortgage rates today are expected to stay relatively elevated compared to the historically low pandemic-era environment.

While some temporary declines may occur, most economists do not expect a rapid return to sub-4% mortgage rates in the near term.

Federal Reserve policy continues influencing expectations in Q1 2026

Although the Federal Reserve does not directly set mortgage rates, investor expectations surrounding future Fed decisions strongly impact mortgage-backed securities, Treasury markets, and overall lending conditions.

Markets continue watching inflation reports and the Federal Open Market Committee (FOMC) updates closely for signs of future rate adjustments when it comes to mortgage rates today.

Mortgage-backed securities and bond market add short-term fluctuations

Mortgage-backed securities and bond market volatility are adding short-term fluctuations to mortgage rates today.

Investors in mortgage-backed securities continue adjusting portfolios as rates move higher, which can amplify sudden shifts in mortgage pricing across conventional, FHA, VA, and refinance loan products. This volatility has been especially noticeable during periods of inflation-driven bond selloffs in Q1 2026. (Reuters)

For homebuyers and homeowners, the key takeaway is that mortgage rates today in Q1 2026 remain heavily tied to broader economic conditions rather than Federal Reserve policy alone.

Borrowers comparing mortgage options should continue monitoring inflation trends, Treasury yields, and housing market forecasts while shopping lenders carefully to secure competitive financing terms.

How National Mortgage Rate Averages Are Calculated in Q1 2026 (And Why They Matter)

Most of the mortgage rates today you see across financial websites, news outlets, and lender comparisons come from large-scale national surveys, mortgage marketplaces, and real-time lending data feeds.

In Q1 2026, these average mortgage rate benchmarks continue helping homebuyers and homeowners understand broader market trends, compare loan options, and monitor changes across the U.S. housing market.

- Freddie Mac’s Primary Mortgage Market Survey (PMMS) remains one of the most widely referenced sources for current mortgage rates in Q1 2026. The survey collects rate data from lenders nationwide and publishes weekly averages for popular products like 30-year fixed-rate mortgages and 15-year fixed loans. These figures are commonly used by financial institutions, journalists, and housing analysts to track mortgage rate trends over time. (Freddie Mac)

- Mortgage marketplaces and real-time lending platforms such as Zillow, Bankrate, and Mortgage News Daily continuously monitor rate quotes, borrower demand, and lender activity throughout the day. These platforms aggregate national lending data to estimate mortgage rates today for conventional, FHA, VA, refinance, and jumbo loan products. (Yahoo Finance)

- Financial media outlets and housing analysts including Realtor.com, AP News, Yahoo Finance, and MarketWatch regularly combine mortgage rate data with broader economic trends such as inflation, Federal Reserve policy, Treasury yields, housing inventory, and affordability conditions. This helps consumers better understand why mortgage rates move throughout Q1 2026 and how economic conditions may affect borrowing costs moving forward. (Realtor.com)

These national mortgage rate averages are extremely useful as market benchmarks, but borrowers should understand that they are not personalized loan offers.

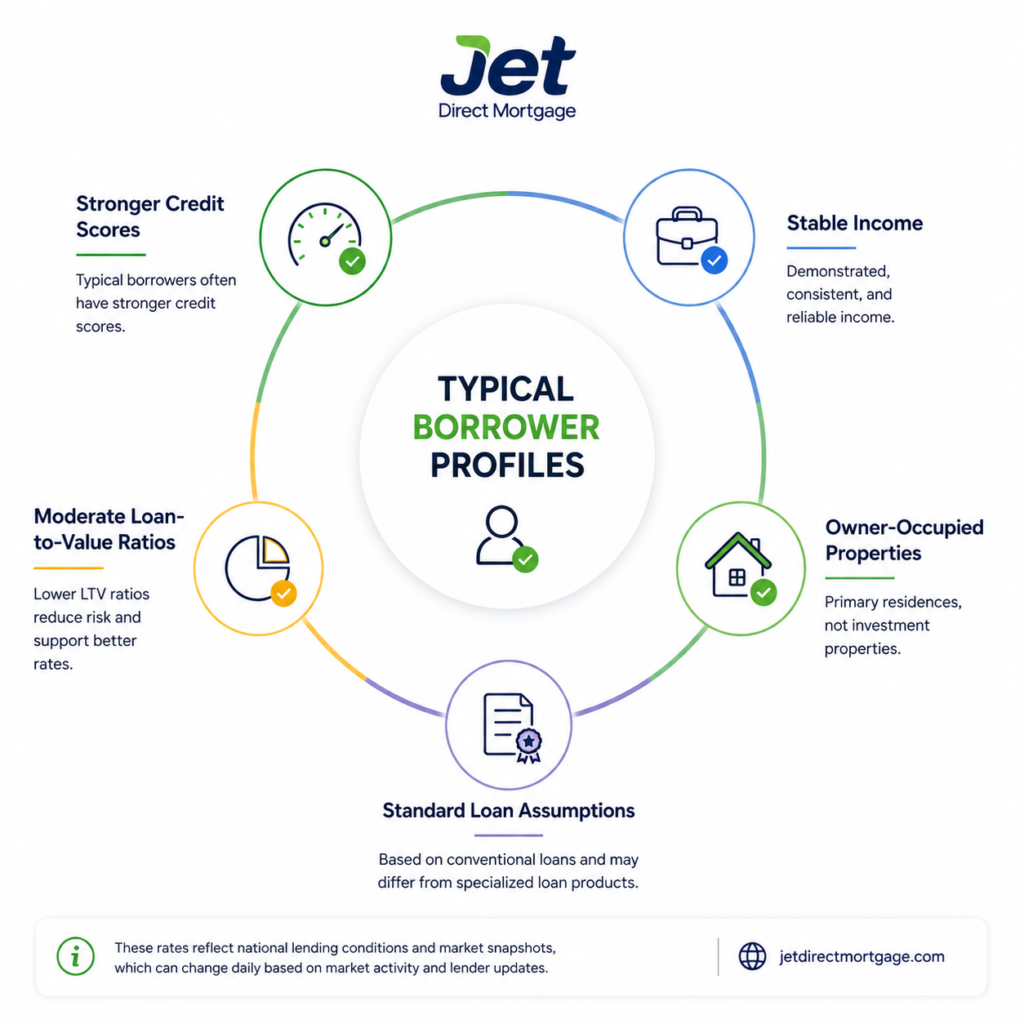

What Mortgage Rate Averages Typically Reflect

- Typical borrower profiles, often including stronger credit scores, stable income, moderate loan-to-value ratios, and owner-occupied properties.

- National lending conditions, rather than localized markets or state-specific pricing differences.

- Daily or weekly market snapshots, meaning mortgage rates today can still fluctuate intraday based on bond market activity and lender pricing updates.

- Standard loan assumptions, which may differ from specialized financing products such as jumbo loans, VA loans, FHA loans, adjustable-rate mortgages, or investment property financing.

That’s why comparing mortgage rates today should always go beyond national averages alone.

In Q1 2026, factors like credit score, down payment amount, debt-to-income ratio, loan type, property occupancy, and overall financial profile continue playing a major role in determining the actual mortgage rate a borrower may qualify for.

At Jet Direct Mortgage, national mortgage rate data is used to help educate borrowers and provide market transparency, while still emphasizing the importance of obtaining a personalized mortgage quote tailored to your specific financial situation and financing goals.

What Mortgage Rates Today Mean in Real Dollars in Q1 2026

To better understand how mortgage rates today affect affordability in Q1 2026, let’s look at a simple example using a standard 30-year fixed mortgage.

Even relatively small rate changes can have a major impact on monthly payments, long-term interest costs, and overall buying power.

Example Scenario (For Illustration Only — Not a Loan Quote)

- Loan Amount: $400,000

- 30-Year Fixed Mortgage at 6.34% → estimated monthly principal & interest: ≈ $2,488

- 30-Year Fixed Mortgage at 7.00% → estimated monthly principal & interest: ≈ $2,661

That represents a difference of roughly $173 per month, or more than $2,000 per year in additional cash flow, before factoring in property taxes, homeowners insurance, HOA fees, or mortgage insurance.

This example highlights why mortgage rates today continue to play such a critical role for homebuyers and homeowners throughout Q1 2026. Even modest fluctuations in current mortgage rates can significantly affect:

- Your maximum home affordability while keeping the same monthly payment target.

- Your debt-to-income ratio (DTI) and overall mortgage qualification profile.

- Long-term interest costs over the life of a 30-year fixed mortgage.

- Refinancing opportunities if mortgage rates decline later in 2026.

- Whether shorter-term options, such as 15-year fixed mortgages, make sense for faster equity growth and reduced total interest paid.

For borrowers comparing mortgage rates today, understanding the real-world payment impact is often more important than focusing only on headline percentages.

In Q1 2026, many buyers are adjusting purchase budgets, down payments, and financing strategies based on changes in current mortgage rates and overall housing affordability conditions.

Because every borrower’s situation is different, actual monthly payments and mortgage pricing can vary depending on factors such as:

- Credit score

- Down payment amount

- Loan type

- Occupancy status

- Property taxes

- Insurance costs

- Discount points and lender fees

That’s why national mortgage averages should be viewed as market benchmarks rather than personalized loan offers.

Why Are Mortgage Rates Today Still Challenging for New York Homebuyers in Q1 2026?

National averages only tell part of the story. In high-cost housing markets like New York, mortgage rates today continue creating unique affordability challenges for both first-time buyers and existing homeowners throughout Q1 2026.

- Home prices across many parts of New York remain elevated, meaning even modest changes in current mortgage rates can significantly affect monthly housing costs, debt-to-income ratios, and overall buying power. Higher borrowing costs continue impacting affordability across both suburban and urban markets. (AP News)

- Many homeowners still hold “legacy” mortgage rates below 4%, making them hesitant to sell their homes and take on a significantly higher mortgage payment in today’s market. This phenomenon, often called the “lock-in effect”, continues limiting housing inventory in Q1 2026. (Realtor.com)

- Mortgage rates today are creating additional pressure on first-time homebuyers, especially in competitive New York markets where elevated home values, property taxes, and limited inventory already make affordability challenging. (Bankrate)

That combination continues shaping the broader New York housing market in several important ways:

- Housing inventory remains relatively tight, since many homeowners with historically low mortgage rates are choosing to stay in place longer rather than refinance or relocate.

- Monthly affordability remains highly sensitive to mortgage rate fluctuations, meaning even a 0.25% rate increase can materially change monthly payments and qualification thresholds.

- Refinancing strategies have become more nuanced in Q1 2026, with borrowers carefully evaluating cash-out refinances, HELOCs, adjustable-rate products, and long-term rate forecasts before making financing decisions.

- Current mortgage rates today continue influencing buyer behavior, with some borrowers adjusting home price targets, increasing down payments, or exploring alternative loan programs to improve affordability.

For borrowers navigating mortgage rates today in New York, personalized financing strategies have become more important than ever.

Loan structure, credit profile, occupancy type, and down payment size can all substantially impact the mortgage rate and monthly payment a borrower ultimately receives.

Jet Direct Mortgage continues helping borrowers across New York compare mortgage options and navigate changing market conditions in Q1 2026, including:

- Conventional mortgage loans for home purchases and refinances.

- FHA and VA loan programs offering more flexible qualification options for eligible borrowers.

- Jumbo mortgage products designed for higher-priced New York real estate markets.

- Refinance solutions and HELOC options for homeowners evaluating equity access and long-term payment strategies.

Is Now a Good Time to Buy a Home in Q1 2026?

There is no universal answer, but mortgage rates today and broader housing market conditions in Q1 2026 continue creating opportunities for some buyers while presenting affordability challenges for others.

You May Consider Buying Now If:

- Your income and employment are stable, allowing you to comfortably manage current mortgage payments and future housing expenses.

- You have sufficient savings for a responsible down payment, closing costs, and emergency reserves.

- Current mortgage rates today fit within your long-term monthly budget, even if rates remain above pandemic-era lows.

- You plan to stay in the home long enough to build equity, offset transaction costs, and potentially refinance later if rates decline further in 2026.

Potential Advantages for Homebuyers in Q1 2026

- Current mortgage rates remain below some 2024–2025 peak levels, improving affordability compared to previous highs. (Freddie Mac)

- Housing competition has cooled in certain markets, giving buyers more negotiating leverage on pricing, seller concessions, and closing costs.

- Many lenders continue offering flexible mortgage products, including FHA loans, VA loans, adjustable-rate mortgages, and down-payment assistance programs.

- Refinancing opportunities may remain available later, meaning some borrowers are choosing to buy now and potentially refinance if mortgage rates today decline further in future quarters.

You May Want to Pause or Prepare More If:

- Your debt-to-income ratio is already stretched, making higher monthly payments difficult to sustain.

- You have limited savings after closing, reducing financial flexibility for unexpected expenses or market changes.

- Your employment or income outlook is uncertain over the next 12–24 months.

- You are relying on future rate cuts alone to make the payment affordable, rather than purchasing within a realistic budget today.

Mortgage rates today in Q1 2026 remain higher than historic lows but lower than recent peaks, creating both challenges and opportunities for homebuyers.

Whether now is a good time to buy depends on your income stability, savings, long-term plans, and monthly affordability. Many buyers are still purchasing homes while monitoring future refinance opportunities if rates decline later in 2026.

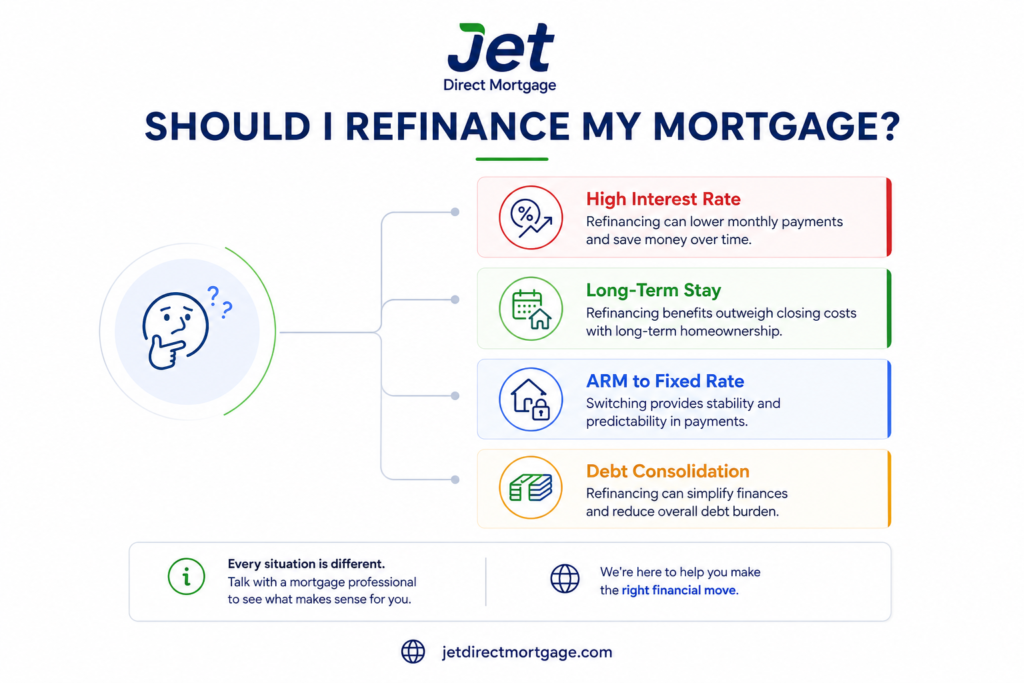

Is Now a Good Time to Refinance in Q1 2026?

Refinancing decisions remain highly personalized in Q1 2026, especially as mortgage rates today continue fluctuating between the low-6% and mid-6% range.

Current refinance mortgage rates today are still significantly lower than some 2024 and 2025 peaks, but whether refinancing makes sense depends on your existing loan, long-term plans, equity position, and overall financial goals.

Refinancing May Make Sense If:

- Your current mortgage rate is meaningfully higher than today’s refinance rates, particularly if your existing rate is in the upper-6% or 7%+ range.

- You plan to remain in the home long enough to recover refinancing costs through monthly payment savings or long-term interest reduction.

- You want to switch from an adjustable-rate mortgage (ARM) to a fixed-rate mortgage for more predictable monthly payments and long-term stability.

- You are consolidating higher-interest debt, such as credit cards or personal loans, into a mortgage refinance strategy that still improves your overall financial position.

- You want to reduce monthly payments or extend loan terms to improve cash flow during a period of elevated living costs and economic uncertainty.

Current Refinance Trends in Q1 2026

- Freddie Mac reported that the average 30-year fixed mortgage rate recently moved between approximately 6.09% and 6.51% during Q1 and early Q2 2026, depending on broader market volatility and Treasury yields.

- Refinance activity has increased noticeably in 2026 as rates moved below some prior highs, with Freddie Mac reporting that refinances accounted for roughly 42% of single-family acquisition volume in Q1 2026.

- Many homeowners continue exploring:

- Rate-and-term refinances

- Cash-out refinancing

- HELOC alternatives

- Shorter-term mortgage products

depending on equity levels and long-term financial planning goals.

You May Want to Wait or Reevaluate If:

- Your current mortgage already carries a low fixed rate, especially below 4–5%.

- Closing costs outweigh projected monthly savings within your expected time horizon in the property.

- Your credit profile or debt-to-income ratio has weakened, reducing eligibility for competitive refinance mortgage rates today.

- You expect to sell or relocate within the next few years, limiting the long-term benefit of refinancing.

Refinancing in Q1 2026 may make sense if current mortgage rates today are significantly lower than your existing loan rate, or if refinancing improves your monthly cash flow, loan stability, or debt structure.

Homeowners with higher-rate mortgages, adjustable-rate loans, or long-term plans to stay in their homes may benefit the most from exploring refinance opportunities.

Next Steps for New York Borrowers in Q1 2026

If you’re currently:

- Buying a home in New York

- Comparing mortgage rates today

- Refinancing an existing mortgage

- Or exploring financing options such as FHA loans, VA loans, jumbo mortgages, HELOCs, or adjustable-rate mortgages

These are some of the smartest next steps to consider in Q1 2026.

1. Get a Personalized Mortgage Rate Quote

Mortgage rates today can vary significantly based on:

- Credit score

- Down payment amount

- Loan type

- Property occupancy

- Debt-to-income ratio

- Loan size and location

A personalized mortgage quote helps you understand your estimated monthly payment, closing costs, and realistic financing options based on current market conditions rather than national averages alone.

2. Request a Mortgage Pre-Approval

In many New York housing markets, pre-approval remains one of the strongest tools buyers can have in Q1 2026.

Benefits of pre-approval include:

- Understanding your realistic home price range

- Strengthening offers in competitive markets

- Identifying potential credit or income issues early

- Improving confidence while shopping for homes

With mortgage rates today still fluctuating, pre-approval can also help borrowers lock financing strategies sooner rather than later.

3. Compare Loan Programs Carefully

Different mortgage products can create very different long-term outcomes depending on your financial goals and time horizon.

Borrowers in Q1 2026 continue comparing:

- Conventional mortgage loans

- FHA and VA loans

- Jumbo mortgage programs

- Fixed-rate vs adjustable-rate mortgages (ARMs)

- 15-year vs 30-year mortgage terms

- Cash-out refinance and HELOC options

Choosing the right structure can impact monthly affordability, total interest paid, refinancing flexibility, and long-term equity growth.

4. Build a Long-Term Mortgage Strategy

For many borrowers, the best decision is not simply chasing the absolute lowest mortgage rate today, but creating a financing strategy that fits long-term goals and financial stability.

Important questions to consider include:

- Could refinancing make sense later if rates decline further in 2026?

- How much equity could you build over 5–10 years?

- Would additional down payment improve affordability significantly?

- Does a fixed-rate mortgage provide more stability than an ARM in the current environment?

- How would future life changes affect affordability?

As mortgage rates today continue evolving throughout Q1 2026, successful borrowers are focusing on sustainable monthly payments, long-term flexibility, and personalized financing solutions rather than trying to perfectly time the market.

Ready to become a homeowner? Let’s get you started.

FAQ

What are mortgage rates today in Q1 2026?

Mortgage rates today in Q1 2026 generally remain in the low-6% to mid-6% range for many conventional 30-year fixed mortgages, although actual rates vary by lender, credit score, loan type, and down payment.

Mortgage rates continue fluctuating based on inflation data, Treasury yields, Federal Reserve expectations, and overall housing market conditions.

Will mortgage rates go down in 2026?

Many economists expect mortgage rates to gradually ease throughout 2026, but significant declines are not guaranteed. Mortgage rates today remain heavily influenced by inflation, bond markets, and Federal Reserve policy expectations.

While some forecasts suggest moderate improvement later in 2026, rates are still expected to remain above the historic lows seen during the pandemic era.

Is now a good time to buy a home with current mortgage rates?

For many borrowers, buying a home in Q1 2026 can still make sense if monthly payments comfortably fit their budget and long-term financial goals.

Mortgage rates today are higher than historic lows but lower than some recent peaks. Buyers with stable income, solid savings, and long-term homeownership plans may still find good opportunities in the current market.

Should I refinance my mortgage in Q1 2026?

Refinancing may make sense if your current mortgage rate is significantly higher than today’s refinance rates or if refinancing improves your monthly cash flow, loan stability, or debt structure.

Many homeowners in Q1 2026 are exploring rate-and-term refinances, cash-out refinancing, and fixed-rate options depending on their long-term financial goals and home equity position.

What factors affect mortgage rates today?

Mortgage rates today are influenced by several economic factors, including inflation, Treasury yields, Federal Reserve policy expectations, mortgage-backed securities markets, employment data, and overall investor sentiment.

Lenders also price mortgages based on borrower-specific factors such as credit score, debt-to-income ratio, loan amount, occupancy type, and down payment size.

How can I get the best mortgage rate in Q1 2026?

To secure a competitive mortgage rate in Q1 2026, borrowers typically benefit from improving credit scores, reducing debt, increasing down payments, comparing multiple lenders, and choosing the right loan structure.

Shopping lenders carefully and obtaining a personalized mortgage quote can often make a significant difference in both monthly payments and long-term borrowing costs.

Experienced Chief Operating Officer with a 26 + year demonstrated history of working in the banking industry. Skilled in all aspects of the residential mortgage market . Strong business development professional with a Bachelor of Science (BS) focused in Business Administration and Management, from St. Joseph College. A direct endorsement underwriter and a licensed Mortgage Loan Originator.